Fed Mulls Explicit Forward Guidance, Stays Wary of Yield Targets

Federal Reserve officials showed no readiness at their June meeting to commit to yield-curve control.

(Bloomberg) -- Federal Reserve officials showed no readiness at their June meeting to commit to yield-curve control, but did reveal an eagerness to provide more guidance in coming months on the future path of interest rates and asset purchases.

“Many participants remarked that, as long as the committee’s forward guidance remained credible on its own, it was not clear that there would be a need for the committee to reinforce its forward guidance with the adoption of a YCT policy,” minutes published Wednesday of the June 9-10 Federal Open Market Committee meeting showed.

YCT refers to yield caps or targets, a strategy of limiting the yields on government bonds at specific maturities. It’s a tool some central bankers believe can help reinforce an existing commitment to hold policy rates low for an extended period, as the Fed is already doing.

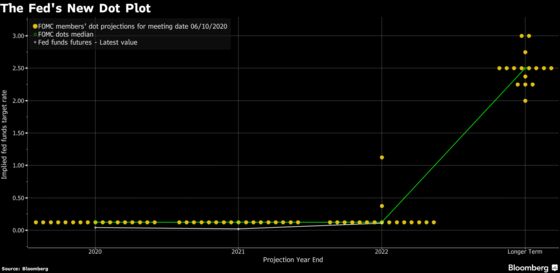

U.S. central bankers left interest rates near zero at the session, which was conducted via video conference. They also agreed to keep purchasing Treasury and mortgage-backed bonds at a pace of about $120 billion a month.

In a press conference that followed, Fed Chair Jerome Powell said officials were “not even thinking about thinking about raising rates.”

Forward Guidance

The minutes showed that various participants viewed the economy needing support “for some time” and that the central bank should strive to communicate clearly on the outlook for policy at upcoming meetings.

“Most participants commented that the committee should communicate a more explicit form of forward guidance for the path of the federal funds rate and provide more clarity regarding” asset purchases, according to the record of the meeting.

Powell on Tuesday told lawmakers the U.S. economy had begun to rebound from the coronavirus pandemic sooner than expected, but that the outlook was “extraordinarily uncertain and will depend in large part on our success in containing the virus.”

“While this bounceback in economic activity is welcome, it also presents new challenges -- notably, the need to keep the virus in check,” he said in testimony before the House Financial Services Committee.

FOMC members showed differing views on what precisely should inform their future policy moves, though they “generally indicated support for outcome-based forward guidance.”

Inflation Overshoot

A “number” of officials favored tying future policy moves to inflation. That could involve waiting for “a modest temporary overshooting of the committee’s longer-run inflation goal” of 2%.

“A couple” of other FOMC members signaled a preference for linking future moves instead to the unemployment level, while “a few others” favored calendar-based forward guidance.

In their discussion of the economy, policy makers said they expected consumer spending to rebound strongly in the second half of 2020. They added, however, “the recovery in consumer spending was not expected to be particularly rapid beyond this year.”

Officials also highlighted “significant uncertainty and downside risks associated with the pandemic.” They also appeared willing to nudge lawmakers toward passing additional stimulus.

Fiscal Support

“Among the other sources of risk noted by participants were that fiscal support for households, businesses and state and local governments might prove to be insufficient,” the minutes said. “Participants stressed that measures taken in the areas of health-care policy and fiscal policy, together with actions by households and businesses, would shape the prospects for a prompt and timely return of the U.S. economy to more normal conditions.”

Fed officials heard a staff presentation on yield curve control and forward guidance. On the latter, the staff ran model simulations that suggested the committee would have to maintain “highly accommodative financial conditions for many years” to significantly boost the recovery.

On yield curve control, the staff outlined its various past uses, including experiences in the U.S. during World War II and by Australia and Japan in recent years.

The three experiences “suggested that credible YCT policies can control government bond yields, pass through to private rates and, in the absence of exit considerations, may not require large central bank purchases of government debt,” the minutes said. “But the staff also highlighted the potential for YCT policies to require the central bank to purchase very sizable amounts of government debt under certain circumstances.”

Just over half of economists surveyed by Bloomberg May 29-June 3 said they expected the Fed to eventually adopt yield-curve control, but probably not before September.

©2020 Bloomberg L.P.