Fed May Boost Balance Sheet But Evercore Warns It’s Not QE Redux

Fed May Boost Balance Sheet But Evercore Warns It’s Not QE Redux

(Bloomberg) --

This week’s volatile moves in U.S. money markets raise the odds that the Federal Reserve will start expanding its balance sheet, just weeks after it stopped running down its portfolio of bond holdings.

That’s the take of some Fed watchers ahead of the central bank’s policy announcement on Wednesday, when the Fed’s Open Market Committee is forecast to lower its benchmark interest rate. Any move to resume balance-sheet expansion, however, would probably be entirely separate from a policy-based move to lower borrowing costs.

Instead, it has everything to do with the mechanics of the financial system. The surge in money-market rates Monday and Tuesday could be a symptom that banks lack sufficient reserves -- in other words, there’s just not enough cash in the system to prevent spikes in short-term rates caused by a confluence of certain transactions.

“There is a good chance that the Committee will shorten or scrap outright the period in which the balance sheet is kept on hold,” Evercore ISI analysts Krishna Guha and Ernie Tedeschi wrote in a note Monday. On Tuesday, they specified their base case is for buying up to $14 billion a month in Treasuries, starting in October.

Fed policy makers have repeatedly underscored that they will seek an ample supply of bank reserves, ensuring that they can effectively implement monetary policy -- without the danger that short-term rates exceed levels targeted by the central bank. But that’s come into question during this week’s ructions.

Back in March, the Fed indicated in a statement that once reserves had shrunk to a level no greater than necessary for efficient policy implementation, it would begin letting its balance sheet expand again. (The Fed can boost banks’ reserves by buying assets such as Treasuries.)

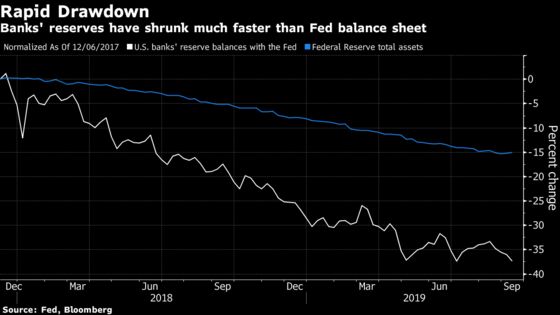

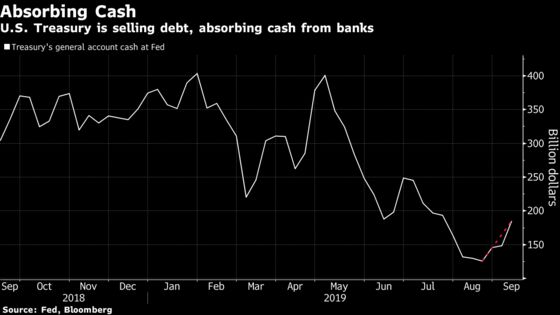

Banks’ reserves now stand at just under $1.5 trillion, down from $2.8 trillion at the peak in 2014 and around a seven-year low. The latest surge in issuance of U.S. Treasuries by the federal government to fund the budget deficit, after a deal between Congress and President Donald Trump to boost the U.S. debt ceiling, has contributed to the recent shrinkage. Targeting the appropriate level of reserves can be challenging for officials given all of the various influences of the economy.

“Is it an imminent disaster?” Jeffrey Gundlach, chief investment officer of DoubleLine Capital, asked of the spike in repurchase agreements earlier this week. “No. The Fed is going to use this warning sign to go back to some balance sheet expansion,” he said in a webcast Tuesday.

Allowing for bigger bank reserves could help relieve pressures without the Fed having to mount continuous operations such as Tuesday’s $53.2 billion injection of liquidity via an overnight repo operation. That first-in-a-decade move will be followed up Wednesday, when the Fed’s New York district bank is prepared for an operation of as much as $75 billion.

But resuming bond purchases to let banks’ reserves start expanding again isn’t a policy move, analysts flagged.

“This would not be a resumption of QE or even so-called QE-lite,” Guha and Tedeschi wrote, referring to the quantitative easing the Fed conducted starting in the crisis, the last wave of which ended in 2014. “It would simply be a return to pre-2007 dynamics. But it would mechanically boost bid for Treasuries and may therefore still have some market impact.”

Rabobank also saw the potential for traders to see the move as relevant. “We wonder whether the market would judge such a step” to be mechanically similar to an asset-purchase program, the bank’s strategists including Richard McGuire wrote Wednesday.

Also to watch for on Wednesday is the potential for a standing repo facility, which would allow eligible banks to convert Treasuries into reserves on demand at an administered rate. Fed staff briefed officials on the idea back in June.

Finally, the Fed could also cut the rate it pays on banks’ excess reserves by more than the benchmark federal funds rate target.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger

©2019 Bloomberg L.P.