Fed Leans Toward Shortening Maturity of Its Treasury Holdings

Federal Reserve policy makers look to be leaning toward shortening the average maturity of their holdings of Treasury securities.

(Bloomberg) -- Federal Reserve policy makers look to be leaning toward shortening the average maturity of their holdings of Treasury securities once they complete normalization of the balance sheet later this year.

Fed Vice Chairman for Supervision Randal Quarles and Cleveland Federal Reserve Bank President Loretta Mester both said this week they would favor such a move, while also noting that no final decision has been made.

“My initial inclination is to think that we should go, all things considered, we should go back to a shorter duration,” Quarles said on Friday at a monetary policy forum in New York.

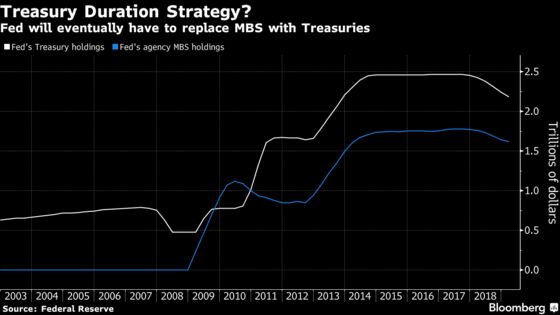

The Fed’s decision on what securities to hold on its balance sheet is of critical importance to investors. A shift in the central bank’s portfolio away from longer-dated Treasury bonds toward bills would tend to put downward pressure on short-term interest rates -- unless the Treasury Department elected to issue more bills in response.

A shorter-dated portfolio would give the Fed added firepower if a cut in interest rates to zero was not enough to counter a downturn in the economy. In that event, it could sell its short-term Treasuries or allow them to run off and use the proceeds to purchase longer-term debt, in an operation known as Operation Twist. That would put downward pressure on Treasury bond yields, providing support to the economy by lowering borrowing costs for home buyers and corporations issuing debt.

$3.98 Trillion

The duration of the Fed’s portfolio lengthened during the financial crisis as it added to its holdings of longer-term debt via quantitative easing. In a Jan. 18 note, Deutsche Bank analysts Steven Zeng and Matthew Luzzetti wrote that the Fed’s Treasury holdings “are estimated to have an average maturity of 7.7 years, or 1.9 years longer than the outstanding Treasury market and 2.3 years longer compared to private sector holdings.”

In an effort to normalize its balance sheet, the Fed is currently reducing its bond holdings by a maximum of $50 billion per month by opting not to reinvest some of the proceeds of securities as they mature. The balance sheet now stands at $3.98 trillion, down from a record high of $4.52 trillion in January 2015.

Minutes of the Fed’s January meeting released this week showed widespread agreement on ending that runoff this year. Left unanswered though is what investment strategy the central bank will adopt after that.

‘Ultimate Composition’

“The question of the ultimate composition of our balance sheet in the longer run is a very important one,” Fed Chairman Jerome Powell told reporters on Jan. 30. “It’s one that we see ourselves as coming to, you know, fairly soon, as in, in coming meetings.”

The Fed currently does not actively manage the duration of its reinvestments, simply allocating its bids proportionally to the amounts that the Treasury offers through its public debt auctions.

“I would skew it towards short-term Treasuries,” Mester said on Feb. 19 in an appearance in Newark, Delaware. “But there’s still an issue whether you want it to look like, even in the shorter terms, more like a market, or whether you want to go all to very short-term Treasuries. And I think that’s a decision we haven’t made yet.”

In his speech Friday to the policy forum sponsored by the University of Chicago’s Booth School of Business, Quarles sounded non-committal on what approach the Fed should take.

“In regard to duration, moving to shorten the duration of our holdings could increase the Fed’s ability to affect long-term interest rates if the need arose,’’ he said. “However, it might be preferable to have the composition of our Treasury holdings roughly match the maturity composition of outstanding Treasury securities, minimizing any market distortions that could arise.’’

It was only later, in response to an audience question, that Quarles made his preference known, while leaving open the possibility that he could be convinced otherwise during the Fed’s ongoing debate about the issue.

“We should focus our balance sheet” on short-term securities, he said, adding, “but I’m certainly open to persuasion.’’

--With assistance from Matthew Boesler and Christopher Condon.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Randall Woods

©2019 Bloomberg L.P.