Fed Entering Brave New Policy World as Rates Near Normal Levels

Chairman Jerome Powell and his colleagues are expected to ignore Trump’s criticisms and raise interest rates this week.

(Bloomberg) -- As the Federal Reserve approaches the final stages of monetary policy normalization 10 years after it cut interest rates to zero, it faces the tough task of charting a less certain path while taking incoming fire from President Donald Trump.

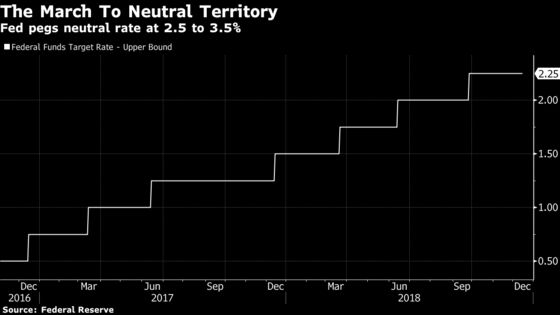

Chairman Jerome Powell and his colleagues are expected to ignore Trump’s criticisms and raise interest rates this week for the fourth time in 2018, to a setting of 2.25 percent to 2.5 percent. That will nudge rates to the bottom of what Powell has called the “broad range’’ of what’s neutral or normal for the economy -- neither restricting nor spurring growth.

“Policy making is easy when you are obviously far away from’’ neutral, said Vincent Reinhart, chief economist at Standish, part of BNY Mellon Investment Management. “It’s much harder when you get into a region where there is a range of disagreement over what neutral is.’’

The Fed is likely to slow its rate hiking campaign in response. Economists now expect it to boost rates twice next year, not the three times they saw previously.

There’s a lot at stake. The expansion is at a point where the Fed often makes a mistake, either raising rates too much, triggering a recession, or not enough, setting off a surge in inflation or asset prices. The Fed’s own credibility is also on the line given Trump’s attacks.

Powell gave a taste of what’s to come last month, declaring that “there is no preset policy path. We will be paying very close attention to what incoming economic and financial data are telling us.’’

While officials always say policy is data dependent, “they’re getting to the point where they actually mean it,’’ Reinhart said.

The result is likely to be more volatile financial markets because policy will be less predictable. But the strategy of not presaging rate hikes may also provide Trump with a smaller target to attack.

Besides raising rates on Wednesday, policy makers may take another step toward normalization by altering their policy statement to exclude its forecast of “further gradual increases’’ in rates. That would represent a break from the “forward guidance’’ strategy employed during the financial crisis and its aftermath to shape market expectations.

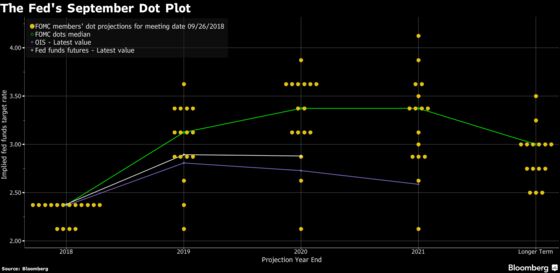

Investors though will continue to have the Fed’s “dot plot’’ for clues on where rates are headed. The graphic -- which lays out anonymously each policy makers’ rate projections -- showed 12 officials in September evenly split among two, three or four hikes for 2019.

What constitutes normal policy going forward is likely to look a lot different than in the past. The Fed’s policy rate will be much lower and its balance sheet much larger.

A Fed factoid illustrates the point: In April 2012, the lowest estimate of the neutral rate by a policy maker was 3.5 percent. In September that was the highest.

As Powell struggles with this brave new world, he will though face some problems familiar to his predecessors.

Risk Management

At the Fed’s annual gathering in Jackson Hole, Wyoming, in August, Powell spoke approvingly of the risk management approach to policy making pursued by former Chairman Alan Greenspan. That strategy says policy shouldn’t be set simply according to a baseline economic forecast, but also should take account of the risks surrounding the outlook.

Easier said than done, as the maestro himself found out: In the first half of the 2000s, Greenspan may have inadvertently sowed the seeds of the housing bubble by keeping rates low to counter a perceived risk of deflation.

Over the past two years, the Fed has marched rates higher even as it’s characterized the economic risks as “roughly balanced.’’ It’s been able to justify that because rates were below neutral. Soon that may no longer be the case.

What’s more, the minutes of the Federal Open Market Committee’s November meeting suggested that policy makers were becoming more worried about downside risks, even though they continued to call them balanced, Diane Swonk, chief economist at Grant Thornton LLP, said. She expects the Fed to carve out some flexibility so that it can pause hikes next year.

Small ‘p’ Pause

In April 2006, then-Chairman Ben Bernanke told lawmakers that the central bank might take a break at some point from raising rates at every meeting but if it did, that wouldn’t necessarily mean it was done tightening credit. Much to his surprise, investors reacted as if he had announced an immediate end to Fed rate increases, sending stock prices higher and bond yields lower. In the event, the Fed didn’t pause its hiking campaign and instead raised rates in May and June before stopping for good.

“There is a pause with a capital ‘P’ and a pause with a small ‘p’,’’ said Nathan Sheets, chief economist at PGIM Fixed Income. The former suggests the Fed is done while the latter indicates it may just be taking a short time-out to assess the outlook.

The trouble is that investors are predisposed to seeing any break in rate hikes as a Pause. And that could particularly be true next year: They are betting on just one quarter-point increase in 2019, according to pricing in interest rate futures.

Powell will have one big advantage in trying to explain what the Fed is up to: He’ll hold a press conference after every policy-making meeting, double the number this year. Back in 2006, the Fed didn’t hold any post-FOMC briefings with the media.

--With assistance from Christopher Condon.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull

©2018 Bloomberg L.P.