Fed Drags Feet as Digital Money Challenges Central Banks

Fed Drags Feet as Digital Money Revolution Tests Central Banks

(Bloomberg) -- When finance ministers and central bankers come to Washington this week, the International Monetary Fund has a message for them: Digital currencies are on your doorstep. Get involved.

“In the U.S., and other countries around the world, it is just a matter of time before we see massive disruption,’’ Tobias Adrian, the director of the IMF’s monetary and capital markets department said in an interview. “There is at least the potential that new technology might lead to a new global payment system fairly rapidly.”

The G-7 on Thursday will release broad guidelines for regulating digital money. They will also discuss whether central banks should issue their own. Adrian’s team is contributing to the report.

Central banks from Sweden to Canada and China are studying whether their money should have a digital counterpart. Sweden began an e-krona project in 2017 and has issued two reports on the topic. The Bank of Canada has launched a formal research project that has partnered with other monetary authorities. The U.S. central bank, by comparison, is focused on updating the domestic payment system to real-time settlements so money moves almost instantly.

The forces of change are coming from two, longer-run developments that regulation may slow but not stop.

Online Purchases

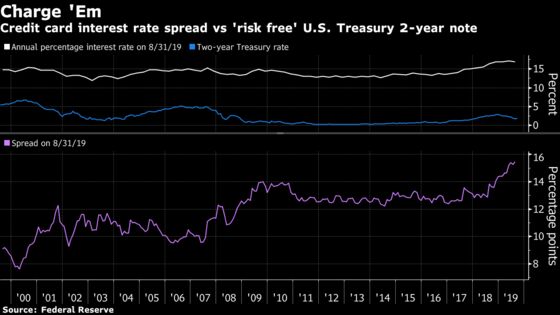

The first: Transactions are increasingly conducted online, and consumers and merchants want cheaper and faster payment systems. In the U.S. today, payments travel through banks and credit card companies, and along the way there are fees and delays. Those costs cut particularly hard against gig workers, immigrants, and low-income people.

“The American payment system is a giant reverse Robinhood, sucking billions of dollars out of people who live paycheck to paycheck and depositing money in the form of credit card rewards to the already rich,’’ said Aaron Klein, a fellow at the Brookings Institution in Washington, who is critical of the roughly five-to-six years the Fed says it will take to launch its own real-time payment system.

The second trend is a potent threat. Social media and online platforms like Facebook could create “stablecoin’’ currencies to facilitate transactions on their platforms. A stablecoin’s value is linked to some reserve asset and is designed to have less price variation than cryptocurrency.

Libra

A financial system that is moving away from a bank-centric model of payments to one that is based on payment platforms, leaves central bankers with a choice: Do they want on their country’s money or somebody else’s to facilitate those transactions?

A system of competing currencies “is what the U.S. banking system used to look like in the 1800s, and we had repeated financial crises,’’ said Julia Coronado, the founder of MacroPolicy Perspectives in New York and a former Fed board economist.

But today the public is demanding simpler payment forms and the central bank should find ways to embrace that while protecting the safety and soundness of money, she said.

“The monetary authority must recognize the current system doesn’t fully serve the public’s needs anymore and some degree of disruption is inevitable,” said Coronado.

Fed Links

That’s a tall order for the Fed to accomplish without congressional backing or support of the banking system, with which it has deep historical linkages. And so far, the U.S. central bank hasn’t looked to be a first mover in the space.

The Fed has no formal digital currency research effort, though its economists are keeping abreast of the topic. It is occupied with the build out of its real-time payment system FedNow.

FedNow will compete with a private payment system run by banks that is already delivering real-time payments -- for a fee. It will also continue to work through a bank-centered model rather than a payment-centered model. In fact, FedNow intentionally strengthens the current banking model rather than disrupting it.

A digital currency “is really about the industrial organization of the payment system,’’ said former Richmond Fed President Jeffrey Lacker. “The Fed has always aligned itself with the banking system, and FedNow is about preserving the privileged place banks have in that system.’’

Fed Governor Lael Brainard spoke about the costs and benefits of stablecoins and central bank digital currencies on Wednesday in Washington.

“Global stablecoin networks also may pose challenges to bank business models,” she cautioned. “In the extreme, widespread migration to one or more global stablecoin networks could disintermediate the role of banks in payments.”

Economists predict the Fed can’t wait much longer to confront the question of digital currency. That’s also the view of the leaders of the Bank for International Settlements and the IMF -- Depression-era institutions that were founded to help stabilize the global monetary system.

“It might be sooner than we think that there is a market and we need to be able to provide central bank digital currencies,’’ BIS chief Agustin Carstens told The Financial Times in June.

Privacy, Outages

There are plenty of things to worry about, economists caution. Big tech monetizes user data and it would certainly continue to do so if they got involved in payments, raising privacy concerns. Platform payment systems could easily develop into monopolies and help spread dollarization to other nations as merchants and consumers abandoned local currencies. Anything digital is subject to hacking, power outages and is naturally limited by access to technology.

Adrian, the IMF director, says central bankers often argue from the status quo when it comes to digital currency, asking, “What problem are you trying to fix?”

Mainly, it’s that payment needs are changing and legacy services are expensive and slow, Adrian said. As economists, “we like innovation and we like competition,” he said.

“That is the thing about innovation -- you don’t quite know what it is going to be used for,’’ Adrian said. “Did we know we would come to rely so much on our smartphones when they were introduced?”

--With assistance from Alex Tanzi.

To contact the reporter on this story: Craig Torres in Washington at ctorres3@bloomberg.net

To contact the editors responsible for this story: Alister Bull at abull7@bloomberg.net, Margaret Collins, Vince Golle

©2019 Bloomberg L.P.