The End of Fed Debt Unwind Is Set. So Treasury's Looking at What's Next

The Fed is just weeks removed from announcing plans to halt its balance-sheet reduction.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- The Federal Reserve may be just weeks removed from announcing plans to halt its balance-sheet reduction, but the U.S. Treasury is already looking ahead to when the central bank might start growing its portfolio again.

In the usual drill before the Treasury’s announcement of borrowing plans for the next three months -- set for May 1 -- the department’s debt managers asked bond dealers for guidance on Friday. Among the insights sought was when -- down to the exact month and year -- the banks expect the Fed to resume growing its balance sheet after the roll-off ends in September. The request included the firms’ views on the long-run composition of the Fed’s balance sheet and the path officials will use to get there.

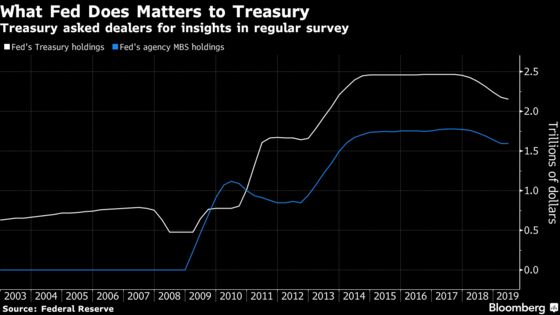

The Fed has made clear that it wants to ultimately return to its pre-crisis approach of holding only government debt, which will involve slowly replacing mortgage securities with Treasuries. What’s unclear is the maturity of Treasuries it will favor.

The twist is that strategists predict that sometime after October the central bank will reach a turning point, when it will need to start increasing its assets again. It would need to do that to prevent bank reserves from declining so far that funding markets become disrupted.

This all matters to the overseers of America’s debt because additional Treasury purchases by the Fed would reduce how much the government needs to tap from the the public to meet its funding needs. The Fed’s decision also factors into what maturities Treasury decides to issue. The central bank’s portfolio is about $4 trillion, including around $2.2 trillion of Treasuries and $1.6 trillion of agency mortgage debt.

“It’s obviously a critical question for the Treasury,” said Lou Crandall, chief economist at Wrightson ICAP. “The Treasury should have a sense of what one of the biggest players in the market is going to do.”

Crandall expects the Fed will eventually tilt its Treasury purchases toward bills, as it seeks to align the maturity of its debt holdings with the average maturity of the public debt. Currently, the weighted average maturity of the Fed’s Treasury investments is about 8 years. That compares with 5.8 years for the market.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Greg Chang

©2019 Bloomberg L.P.