Fed Backs Organic Balance Sheet Rise, Wall Street Wants Whopper

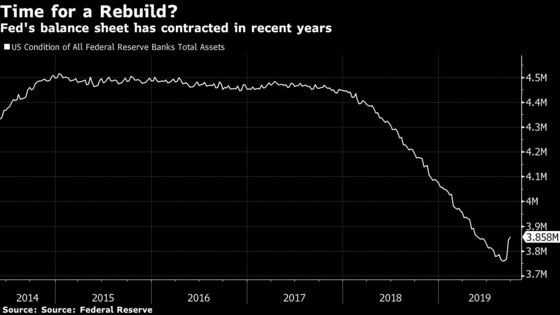

Such a massive operation would seemingly be far bigger than the “organic” balance sheet growth that policy makers are discussing.

(Bloomberg) -- Terms of Trade is a daily newsletter that untangles a world embroiled in trade wars. Sign up here.

They say it’s better to eat organic. But when it comes to the Federal Reserve’s balance sheet, Wall Street is hungering for a lot more.

Financial analysts argue that the Fed needs to buy anywhere from about $200 billion to a half a trillion dollars in Treasury securities to bulk up its balance sheet and reduce the risk of money-market turmoil.

Such a massive operation would seemingly be far bigger than the “organic” balance sheet growth that many Fed policy makers are currently talking about.

It would also be sure to draw comparisons to the quantitative easing programs that the central bank employed during the financial crisis and which President Donald Trump has spoken of approvingly.

Policy makers have sought to push back against any notion of a return of QE by portraying any restart of asset purchases as a natural response to the economy’s increasing demand for currency and liquidity.

“We’re going to be assessing, you know, the question of when it will be appropriate to resume the organic growth of our balance sheet,” Fed Chairman Jerome Powell told reporters on Sept. 18, adding policy makers would take up the matter at their next meeting.

The trouble is that implies Treasury purchases of about $100 billion to $200 billion over the next year, analysts said. That’s much smaller than the amounts many on Wall Street are looking for the Federal Open Market Committee to announce after its Oct. 29-30 gathering in Washington.

“If none of this had messaging or political implications, buying a big chunk of Treasuries up front would be an obvious choice,” Wrightson ICAP LLC chief economist Lou Crandall said in an email. “However, it’s not at all clear that the FOMC has the appetite for that.”

“This could make the October meeting treacherous for the market,” especially if the central bank also takes a pass on cutting interest rates, Crandall added.

JPMorgan Chase & Co. chief U.S. economist Michael Feroli agreed.

There’s a risk the Fed could end up disappointing investors “big time” if it embarks on a smaller balance sheet rise, he said.

Feroli though does expect the Fed to reduce rates for the third time this year in October. Investors are not so sure: They put the odds of a cut next month at about two-in-five, according to trading in the federal funds futures market.

Get Ready for Fed QE-Lite: What Quantitative Easing Is and Isn’t

Economists maintain that the Fed allowed its balance sheet to shrink too far, in the process reducing the supply of bank reserves in the system.

The result: Periodic scrambles for cash that can send short-term interest rates shooting higher, such as occurred earlier this month when repurchase market rates soared as high as 10%.

The repo market -- where financial institutions swap Treasury securities for cash -- “is critically important to the U.S. financial system and the economy,” former Fed officials Joseph Gagnon and Brian Sack wrote in a Sept. 26 blog post.

They said the Fed should consider increasing its balance sheet by $250 billion over the next two quarters through outright purchases of Treasuries to help diminish the risk of future money market turbulence.

After that, the central bank should continue to grow its balance sheet in line with the economy, said Gagnon, now a senior fellow at the Peterson Institute for International Economics, and Sack, currently director of global economics for the D.E. Shaw Group.

Mark Cabana, head of U.S. interest rates at Bank of America Corp., said the Fed may have reduced its assets by $100 billion too much, forcing it to temporarily inject reserves into the banking system recently through overnight and term repurchase pacts. On top of that, he said the Fed should build up a reserve buffer of around $150 billion.

Fed officials agree they may be reaching a point where they’ll need to resume buying assets.

‘Ridiculous’ Tightening

But they’ve been loath to acknowledge that they’ve reduced reserves too much, with some arguing that the money market’s recent problems stem not so much from the level of reserves but which banks are holding them.

Policy makers’ reticence to say they went too far is perhaps not too surprising given Trump’s repeated attacks on the Fed for its “ridiculous quantitative tightening.”

“It is very possible that reserves are near, or approaching, their appropriate level,” Philadelphia Fed President Patrick Harker said on Friday at an event in New York. “If that is the case, we may need to resume the organic growth of the balance sheet earlier than anticipated.”

He stressed though that wouldn’t mean the Fed was launching another round of quantitative easing. “This is not QE4. Let me make this clear. This is not a monetary policy tool,” he said.

--With assistance from Matthew Boesler and Vivien Lou Chen.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Alister Bull, Sarah McGregor

©2019 Bloomberg L.P.