False Dawn in Treasury Yields Seen With Fed Posing Risk

False Dawn in Treasury Yields Seen With Fed Posing Risk

(Bloomberg) -- A familiar scenario may be about to play out in the world’s biggest debt market, with a major breakout in long-term Treasury yields at risk of faltering after a banner couple of days for bond bears.

Revived talk of potential economic stimulus, growing vaccine hopes and Federal Reserve Chair Jerome Powell’s signal of optimism for the year ahead sent 10-year Treasury yields to a roughly three-week high Wednesday, following one of the biggest daily yield spikes of 2020.

Yet rates are still only testing their post-U.S. election peak from several weeks ago, and there’s a host of obstacles to a sustained climb, beyond the fact that Congress has repeatedly failed to forge an agreement on additional relief spending.

For one thing, there’s the prospect that the Fed could swoop in as soon as this month to tamp down long-term borrowing costs to buoy the economy. Wednesday brought another measure showing U.S. labor conditions are already deteriorating, with millions of Americans still out of work. Add to that the fact that U.S. virus cases are surging and spurring fresh state restrictions, and the threat to the recovery is clear.

But economist Ed Yardeni says the key force keeping long-term yields from taking flight is that the Fed has convinced markets that it won’t allow it while the recovery remains tenuous. Some Wall Street analysts predict policy makers will adjust their bond-buying purchase program at this month’s meeting, scheduled for Dec. 15-16, by tilting Treasury purchases more toward longer maturities.

“If it was up to economic forces and trading in sort of a free-market fashion, we probably would see the bond yield moving even higher -- to above 1%,” said Yardeni, founder of Yardeni Research Inc. “But the Fed has put more weight on employing people as opposed to worrying about inflation.”

Looking into next year, most Wall Street strategists forecast higher yields, in large part with Fed policy staying ultra-loose. Both Goldman Sachs Group Inc. and JPMorgan Chase & Co. predict 10-year Treasury yields will reach 1.3% by the end of 2021. Analysts at Societe Generale SA see a jump to 1.5%.

In Asia trading Wednesday, after Tuesday’s big jump in yields, demand from investors to buy the dip wasn’t as robust as normal when yields have climbed toward the top of their range in recent months.

Major Milestone

For now, it’s clear that eclipsing the 1% level is the major test, with runs at that mark repeatedly failing, on occasions such as last month as well as in June. On Wednesday, yields temporarily retreated after a report showed that U.S. companies added fewer jobs in November than forecast. The 10-year yield traded at 0.93% as of 10:01 a.m. in London.

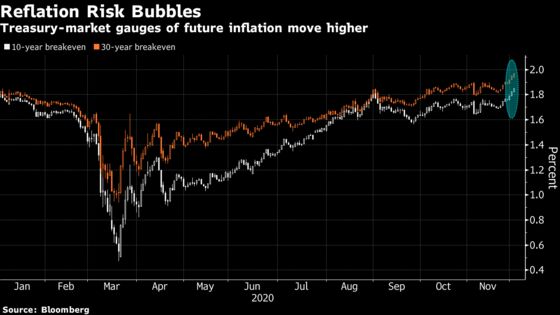

Part of the hesitancy seems to be that this time around bond-market measures of inflation expectations are climbing, potentially supporting the case for higher yields. The 10-year breakeven rate has risen to 1.87%, its highest since May 2019 and up from as low as 0.47% in March.

Powell told the House Financial Services Committee on Wednesday that he sees a “light at the end of the tunnel” around mid-2021, although the near-term looks challenging.

On the flip side, another anchor for yields is that the Fed has also made clear it will keep its target rate pinned near zero for years to come. Traders don’t see the first rate hike until late 2023, and they expect a very gradual pace of increases thereafter. A Morgan Stanley gauge of the expected pace of Fed tightening based on eurodollar futures shows that after the first increase, traders anticipate the central bank will only lift its target rate by about 25 basis points per year thereafter.

With the Fed signaling it will let the economy run hot and not rush to lift rates, a time-tested link between yields and the copper-gold ratio appears to have broken down. While the ratio has been surging, yields haven’t kept pace as the historical correlation suggests they should, in another example of how the central bank is shaping market expectations.

Read more about how a key correlation is breaking down.

Much of the recent rebound in yields may be about a pick-up in term premium, the added compensation investors demand for owning long-term debt, according to Roberto Perli, a partner at Cornerstone Macro LLC. That says to him that it’s more about risks, but not expectations, of better growth and inflation.

“In our view, these risks that the market is pricing might be exaggerated,” Perli, a former Fed economist, wrote in a note with colleague Benson Durham. The firm’s Treasury valuation models indicate that longer-dated yields are too high relative to the fundamentals.

©2020 Bloomberg L.P.