Ex-Prop Traders Who Won Big on Repo Are Ready for Next Big Spike

The central bank’s actions kept the benchmark within its target range, but the efforts may not be enough.

(Bloomberg) -- Exiles from Wall Street’s old proprietary trading desks were among those who cashed in on September’s spiking repo rates, and now they’re lining up for the next big move.

Tucked away at funds from Sydney to Boston, traders who make their livelihood arbitraging dislocated market rates are eyeing another windfall like the repo madness that caught the Federal Reserve on the back foot and left the likes of Jamie Dimon largely on the sidelines.

They include Ardea Investment Management in Sydney, whose team expects more ructions as soon as the end of the year after winning with eurodollar options last month. James Madison at Manulife Investment Management in Boston calls repo glitches opportunities “we simply cannot miss.”

“We took advantage of elevated rates in the commercial paper market where yields on short paper moved higher to compete with overnight repo,” said Madison, a bond trader at Manulife. At the height of the run-up, he was scooping up securities yielding about 5.5%, double their usual rate.

Day-to-day trading of repurchase agreements -- transactions that amount to collateralized short-term loans -- rarely gets much attention, but they influence rates on money-market securities, overnight borrowing and most importantly the Fed’s policy benchmark rate.

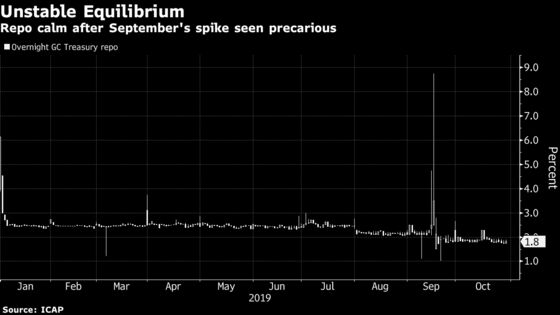

September’s episode, when a funding squeeze sent the repo rate soaring to about 10% and forced the Fed to step in to add temporary liquidity for the first time in a decade, has prompted growing scrutiny, including from U.S. Treasury Secretary Steven Mnuchin and Elizabeth Warren.

The Fed was ultimately drawn in last month because repo’s rise had pushed its own benchmark, the effective fed funds rate, too high. The central bank’s actions kept the benchmark within its target range, but the efforts may not be enough. Wider forces including bigger Treasury borrowing needs and regulations that hobble Wall Street dealers may yet frustrate policy makers.

Gopi Karunakaran, a former trader for Deutsche Bank AG in London who’s now at Ardea in Sydney, expects repeat episodes, possibly as soon as the end of the year when funding traditionally becomes scarce.

“Even given the Fed’s recent actions, I expect volatility in repo to keep reappearing periodically,” he said. “Constrained bank balance sheets mean more pricing anomalies and dislocations.”

Karunakaran and his colleagues at Ardea should know. The Volcker Rule, the part of 2010’s Dodd-Frank financial reform law designed to rein in risky trading by big banks, shut down the prop trading desks where many had made their living.

In September the tables turned. Unburdened by the type of regulations that hamstring the big banks, Ardea’s traders pounced, snapping up Eurodollar options whose value rose as money-market volatility increased. The move helped earn the Ardea Real Outcome Fund a total return of 0.3% in September as Treasuries due in one-to-three years lost 0.12% and bills maturing within three months gained just 0.18%.

It’s an uneven playing field that aggrieves Dimon, the chief executive of JPMorgan Chase & Co. Capital needs meant money had to sit in the bank’s coffers in September, when repos were paying roughly four times what the bank earns at the Fed.

“We could not redeploy it into the repo market,” Dimon told analysts following JPMorgan’s third-quarter earnings release in October. “We’d have been happy to do it.”

| Read More: |

|---|

While the Fed has gone on to add balance sheet expansion -- which permanently lifts banks’ reserves -- to its ad hoc liquidity injections, many firms warn that it may not be enough to thwart future repo spikes.

“We expect funding market pressures to reemerge as we approach important bank reporting dates, including year-end,” Pimco head of short-term bond portfolios Jerome Schneider and his colleagues wrote in a recent note.

That all sets up year-end and the historical cash crunch as the next big pressure point.

“December may put the efficacy of the Fed’s repo stress toolkit to the test,” said Blake Gwinn, head of front-end rates at NatWest Markets.

Money Markets Yearn for More Fed Guidance on Plans for Repo

Regulatory changes to free up banks cash is seen by many, not just Dimon, as part of the ultimate fix.

Mnuchin said in an interview Tuesday that he had spoken to Dimon and other banks about the repo imbroglio and would be prepared to revisit post-financial crisis regulations to help lubricate a clogged financial system. That prompted a warning from Presidential hopeful Warren, who has said in the past repo volatility is no reason to dial back restrictions.

And funding deficits may linger because Fed cash only goes to primary dealers, with no certainty it will trickle down to other market participants.

The Fed’s “cash infusions have succeeded in calming short-term funding markets,” according to Pimco’s Schneider. “However, there is no guarantee the extra liquidity will always be efficiently allocated around the banking system.”

To contact the reporters on this story: Liz Capo McCormick in london at emccormick7@bloomberg.net;Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Cecile Gutscher, Samuel Potter

©2019 Bloomberg L.P.