Everything Is Up for Review at the Fed’s Big Policy Confab in Chicago

Chicago conference is billed as the main event in a yearlong review of how the Fed tackles the goals it’s been given by Congress.

(Bloomberg) -- Stable prices? Check. Low unemployment? Check. Judging by the main gauges of the U.S. economy, Federal Reserve officials might have good reason to pat themselves on the back when they gather in Chicago this week.

Instead, they’ll be taking a second look at everything they do.

For Americans, from wealthy investors to minimum wage-earners, the two-day conference starting Tuesday could be a big deal if it paves the way to a new strategy for managing inflation and fighting recessions.

In the immediate future, that would probably mean lower interest rates for longer, as central bankers step aside and let the job market keep heating up. President Donald Trump, chipping away at the barrier that’s supposed to separate central bankers from elected politicians, has been urging them to go even further.

The Chicago conference is billed as the main event in a yearlong review of how the Fed tackles the goals it’s been given by Congress: maximum employment and price stability.

Baked In?

Chairman Jerome Powell and his fellow policy makers will be joined by academics to debate new research on all kinds of complex topics. But the question that’s likely to dominate boils down to: Does the Fed need a new approach to inflation that’s persistently fallen short of forecasts?

“The Fed needs inflation up at a reasonable level to have room to deal with the next crisis,’’ Adam Posen, a former Bank of England policy maker who’ll take part in the conference, told Bloomberg TV on Friday.

“We all need inflation up, because that’s more conducive to wage growth and a good market,’’ said Posen, now president of the Peterson Institute for International Economics. “We’re in a low-rate, low-risk, low-inflation, secular stagnation environment.’’

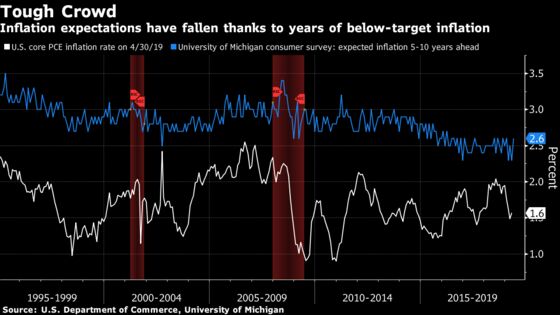

The central bank’s favored inflation measures have undershot the 2% target through most of the current recovery. That’s getting baked into the outlook of investors and households -– creating, Fed officials fear, a self-fulfilling expectation that prices will remain stagnant.

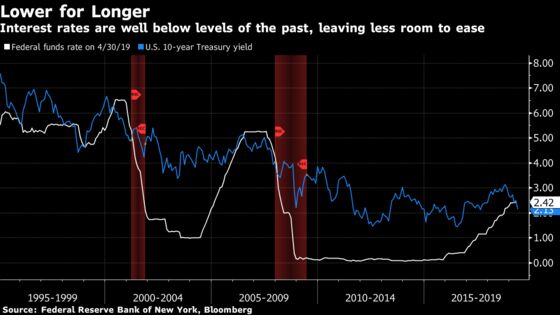

That would compound the bigger problem of low interest rates, which don’t leave much room for cuts in a recession. The Fed worries that powerful long-term forces, like slower population and productivity growth, have hobbled its ability to raise rates in expansions, which makes propping up inflation even more important.

‘Fed Listens’

One possible alternative to the Fed’s current strategy -- seen as a leading contender if the Fed were to decide on changing things up -- is known as average-inflation targeting. Outlined by New York Fed President John Williams in a paper last month, it envisages the central bank allowing prices to rise slightly faster than 2% during expansions, to “make up’’ for periods when they’ve lagged.

Like now. Inflation was close to 2% when the 2019 review, including a multi-city “Fed Listens’’ tour in which central bankers hear directly from business and community leaders, was announced in November. The outlook was strong enough that Fed officials expected to continue the rate-hiking campaign they began in 2015. They got heat from Trump, who has been lobbying for rate cuts, for even considering the idea.

Since then, weak inflation -- a favored gauge came in at 1.6% in April -- and concerns about the trade war’s impact on global growth have intensified the spotlight on Chicago this week.

The Fed stopped raising rates in December, after bringing its benchmark to just under 2.5%. Amid rising market volatility, Fed-watchers -- including former Governor Laurence Meyer, and analysts at JPMorgan Chase & Co. and Barclays Plc -- said last week they now expect cuts as soon as September.

Asked about the case for lower borrowing costs on Friday, Minneapolis Fed President Neel Kashkari, one of the central bank’s more dovish policy makers, said he’s “not quite there yet.’’

Still, Kashkari has been pushing for more attention to the employment side of the Fed’s mandate. He’s argued that America has missed out on jobs and higher wages, because policy makers raised rates in the mistaken belief that unemployment couldn’t fall much lower without stoking prices.

That perspective may get airtime in Chicago too. Two of the panel discussions will examine what full employment should mean for central bankers. They’ll likely reflect some of the “Fed Listens’’ events, when participants repeatedly raised concerns about inequality -- and skepticism about the need to take away the punchbowl just when wages, stagnant for years, are at last starting to accelerate.

Along with Trump’s interventions, those encounters with the public have served as reminders that central banking can’t stay entirely above politics, said J.W. Mason, an assistant professor of economics at City University of New York.

“To listen in a sense is a political act,’’ he said. “It says, we have a constituency we’re accountable to.’’

‘You Want the Opposite’

Not everyone headed to Chicago thinks the Fed needs a whole new strategy.

Kristin Forbes, a Massachusetts Institute of Technology economics professor, says central bankers have other options besides rate cuts to stimulate growth -- like the bond-buying programs they deployed after the financial crisis.

Forbes said she’s “less worried’’ than some about rates going back to zero. A new framework could be difficult to communicate, so “you need a pretty sound reason to change it, given that the system has worked fairly well,’’ she said.

But Brown University economics professor Gauti Eggertsson, whose research was cited in the Williams paper, thinks the status quo is too conservative.

Inflation expectations wouldn’t be bogged down now if the Fed had adopted the “make-up’’ strategy after 2008, Eggertsson said. The rate hikes that began in late 2015, when there was little evidence that inflation was headed north of 2%, wouldn’t have happened.

After the inflationary 1970s, “you wanted the conservative central banker,’’ he said. Nowadays, “you want the opposite.’’

To contact the reporter on this story: Matthew Boesler in New York at mboesler1@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Ben Holland, Alister Bull

©2019 Bloomberg L.P.