(Bloomberg Opinion) -- Under the watchful eye of Beijing’s energy hawks, China’s oil and gas majors have splurged for more than a decade, first on deals abroad and then drilling at home. Yet with crude prices at less than half where they were at the start of the year and demand battered by a coronavirus epidemic, they’re preparing to cut back.

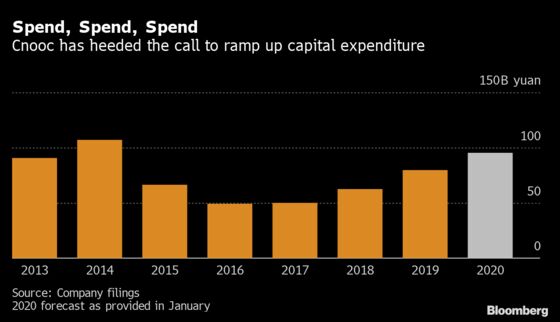

Cnooc Ltd. signaled Wednesday it might reduce its 2020 capital expenditure budget, which was set at as much as $13 billion, the highest since 2014. PetroChina Ltd., the country’s largest oil producer with a market value of $117 billion, suggested Thursday that it would do the same. Given the delicate politics involved, it’s a welcome hint of rational frugality.

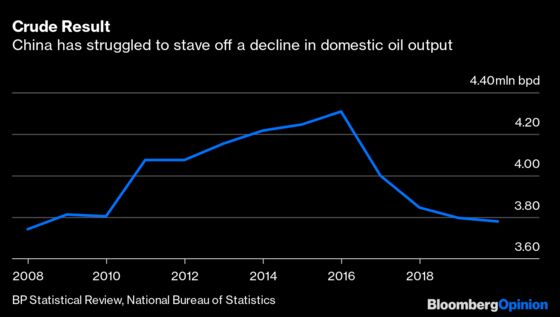

Energy security has always been a top concern for China’s leadership. Overseas deals peaked at $28 billion in 2012, the year Cnooc bid for Canada’s Nexen. Local production growth has been less exuberant, and China has been importing ever more. As trade tensions with Washington rose in 2018, President Xi Jinping urged the country’s state-owned titans to drill. That set off a frenzy from deepwater fields in the South China Sea to shale gas in Sichuan, where China Petroleum & Chemical Corp., known as Sinopec, has led.

Performing national service is fine when oil is at $60 a barrel, even if the improvements are unimpressive compared to the capital spent. It’s a different matter when West Texas Intermediate is just coming off an 18-year low of less than $20. That’s a price at which no one can make money — not even Cnooc, with an all-in production cost of less than $30 per barrel of oil equivalent. Cnooc’s adventures in U.S. onshore and Canadian oil sands look terrible; its buccaneering domestic ventures are little better.

Overseas, oil majors from Chevron Corp. to Saudi Aramco are cutting spending to preserve capital. Dividends are precarious. Logic dictates that China’s producers, even with healthier balance sheets, will follow the same pattern. The question is whether they can put financial logic ahead of political necessity.

So far, the message is cautious: Cnooc executives pointed out that 2020 spending targets were drawn up when oil was at $65, so adjustments would be made. It gave no specifics. PetroChina, meanwhile, didn’t disclose precise targets for the year. That’s no accident, given a volatile market. After a string of personnel changes, there are new bosses across the industry. Political priorities haven’t been set in stone, given the delay in the annual National People’s Congress meeting. Still, the official message has been clear: Life is returning to normal after a devastating shutdown. Announcing a drastic spending cut, or anything that might hint at job losses or a weak economy, simply isn’t on the cards. PetroChina employed 476,000 at the end of 2018.

That doesn’t mean that there won’t be mild cuts followed by steeper ones later in the year, a pattern seen before.

How steep? Unlike during the last price crunch, in 2014 and 2015, the forward curve suggests prices will remain low, with little prospect for a quick solution to the Russia-Saudi spat that has worsened a global supply glut. Demand, meanwhile, is in the doldrums. China’s economy, and therefore its own appetite for oil and gas, is recovering only slowly, and the rest of the world is ailing as more lockdowns, factory closures and travel restrictions are imposed to limit the spread of the coronavirus.

Analysts at UBS Group AG forecast Cnooc’s capex could come down 25% over the next two years, a cut that could be far deeper if oil averages closer to $30 this year. Overall, they project Chinese state-owned oil producers could cut spending by over a third, dragging production down 8% to 9%.

Exploration budgets may be trimmed, though domestic production — where job preservation remains key — will mostly be spared. That leaves refining and other downstream activities, plus projects abroad, to bear the brunt.

Low energy prices aren’t all bad for China, which imports more than 70% of the crude it consumes. Even liberalization of the domestic gas market becomes easier when prices are low enough for consumers to cope with change, Michal Meidan of the Oxford Institute for Energy Studies points out. Cheaper oil could eventually stimulate demand. For now, a little less drilling all round.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Clara Ferreira Marques is a Bloomberg Opinion columnist covering commodities and environmental, social and governance issues. Previously, she was an associate editor for Reuters Breakingviews, and editor and correspondent for Reuters in Singapore, India, the U.K., Italy and Russia.

©2020 Bloomberg L.P.