Not Even a Blockbuster Jobs Report Will Move the Needle for Treasury Bulls

Not Even a Blockbuster Jobs Report Will Move the Needle for Treasury Bulls

(Bloomberg) -- Somewhere on their list of things to be grateful for this Thanksgiving, investors might have put the tranquility in financial markets compared with late last year. But Treasury market participants are also probably wishing for a little more conviction in their next steps.

U.S. government debt has found its steadiest footing in months, with the 10-year yield trading in a narrow range and stabilizing around 1.78%. This owes a lot to the cheerful sentiment in U.S. equities -- which hit record highs in November despite persistent uncertainty over trade talks -- and signs of stabilization in economic data. Federal Reserve Chairman Jerome Powell recently detailed his view of U.S. growth as a glass more than half-full. But that doesn’t mean Treasury investors have abandoned their customary glass-half-empty perspective.

“We still feel that we’re on the right side of this, in the sense that we’re quite miserable with regard to the economic outlook,” said James Athey, a London-based portfolio manager at Aberdeen Asset Management. Even so, he’s sticking to the two-year sector and positioning for a steeper yield curve to keep “a foot in either camp” in case of positive surprises.

Another strong labor market report in this week’s crop of economic data could be one, though Athey thinks for the time being at least, yields are pretty contained. He says the Fed’s prerequisites for a rate hike -- material and persistent inflation pressure -- are unlikely to come about. And even a much stronger gain in jobs than the median forecast of 188,000 is unlikely to shake things up, according to the money manager.

“Payrolls could be 500,000 and it’s not going to move the needle for the Fed,” he said. “That feels like we’ve capped the upside in yields to some degree.”

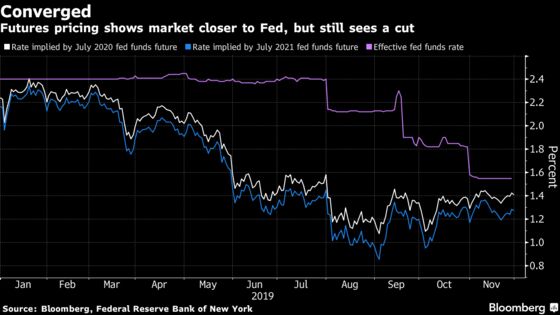

For their part, policy makers may well be thankful that, as the central bank enters its blackout period ahead of the Dec. 10-11 meeting, market expectations are aligned more closely to the Fed’s guidance than they have been all year. Fed funds futures are pricing in basically no change in interest rates over the coming months. But the next move is still expected to be down, with a quarter-point cut fully priced in by the end of 2020.

Ed Al-Hussainy at Columbia Threadneedle reckons aggressive easing is still in the cards for next year, so he’s also betting that yields will fall at the front end of the curve. The investment strategist expects the U.S. labor market trend will point to slower income growth in 2020, meaning that consumption, which remains a powerful support for this record U.S. expansion, “is going to be on thinner ice.”

In the meantime, the potential for progress in U.S.-China trade talks remains a risk to his bullish positioning, particularly as the mid-December deadline for another round of tariffs heaves into view.

He’s hedging against that improved growth scenario on two fronts. He’s buying inflation protection in the form of U.S. breakevens, as the market’s pricing for inflation seems “shockingly low.” And in case of a resurgence in optimism over a U.S.-China deal, he says the euro is a sound bet, as Europe has taken much of the brunt of the damage to global trade.

“I don’t have a lot of conviction that the growth story is getting better,” Al-Hussainy said. “But it may be, so it’s very cheap to get that protection.”

What to Watch

- Monthly jobs data and manufacturing gauges are among the highlights of the coming week

- Here’s the calendar for economic indicators:

- Dec. 2: Markit manufacturing PMI; ISM manufacturing gauge; construction spending

- Dec. 3: Vehicle sales

- Dec. 4: MBA mortgage applications; ADP employment change; Markit services PMI; ISM non-manufacturing gauge

- Dec. 5: Challenger job cuts; jobless claims; trade balance; Bloomberg consumer comfort; factory, durable goods and capital goods orders

- Dec. 6: Payrolls, unemployment and average hourly earnings; wholesale trade sales and inventories; University of Michigan sentiment; consumer credit

- No communications scheduled from Fed policy makers except for a Congressional appearance by Vice Chairman Randal Quarles, who is set to testify Dec. 4-5 on supervision and regulation

- Treasury bills are the focus for the auction calendar:

- Dec. 2: 13-week and 26-week bills

- Dec. 3: 52-week bills

- Dec. 5: 4-week and 8-week bills

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker

©2019 Bloomberg L.P.