Evans Says Fed May Have to Ease If Downside Risks Take Hold

Evans Says Fed May Have to Ease If Downside Risks Become Reality

(Bloomberg) -- The Federal Reserve may have to put interest-rate increases on hold or even ease monetary policy if economic forecasts for 2019 disappoint, Chicago Fed President Charles Evans said.

“At the moment, the risks from the downside scenarios loom larger than those from the upside ones,” Evans said in remarks prepared for a speech Monday in Hong Kong. “If activity softens more than expected or if inflation and inflation expectations run too low, then policy may have to be left on hold -- or perhaps even loosened -- to provide the appropriate accommodation to obtain our objectives.”

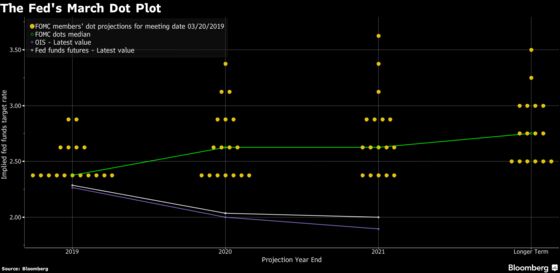

The U.S. central bank’s rate-setting Federal Open Market Committee surprised investors on March 20 by bringing down its projections for further tightening. Eleven of the 17 FOMC officials expected it would be appropriate to leave rates unchanged for all of 2019. The pivot followed a three-year campaign in which policy makers raised their benchmark overnight policy rate from near zero to just under 2.5 percent.

Fed Chairman Jerome Powell cited downgraded estimates for economic growth during his post-FOMC meeting press conference, in part due to a slowdown overseas. Evans echoed that outlook, saying he expects U.S. growth to slow to a 1.75 percent to 2 percent pace in 2019 following a 3.1 percent expansion in 2018.

“The lower end of this range is actually in line with my view of the economy’s long-run growth potential. So we’re not looking at a bad number,” Evans said. “Still, the economy won’t feel like it is doing very well compared with last year’s very strong performance.”

In an interview with Bloomberg TV in Hong Kong, Evans said he’s forecasting policy will be on hold until the fall of 2020.

Inflation close to 2 percent is “good but I’m worried that it still takes accommodation to keep inflation at that level, and so I actually marked down my path for policy rate increases,” he said.

In his speech on Monday, the Chicago Fed chief said if economic growth meets expectations, further tightening would depend on faster inflation. A closely-watched gauge of U.S. price pressures rose above the Fed’s 2 percent target last summer for the first time since 2012, but has since moderated to levels just below 2 percent.

“If growth runs close to its potential and inflation builds momentum, then some further rate increases may be appropriate over time to ensure that the economy settles in on its long-run sustainable growth path and that inflation runs symmetrically about our 2 percent target” Evans said. “In this scenario, the path for rates will depend crucially on any signals of an acceleration in core inflation.”

Yield Curve

In a question-and-answer session after his speech, Evans said there are a lot of “miscues” about modest yield curve developments. While the flatter yield curve is something to be mindful of, U.S. economic fundamentals remain strong and the risk of a negative shock hitting the economy is not “unusually higher or lower at the moment,” he said.

At an earlier panel discussion on Monday, Evans said the Federal Funds rate was close to neutral and it was a good time to be “cautious” given global risks and U.S. fiscal stimulus waning.

“I am not worried about inflationary pressures increasing,” he said. “If anything I am worried they are not going to increase more.”

--With assistance from Michelle Jamrisko and Catherine Bosley.

To contact the reporters on this story: Matthew Boesler in New York at mboesler1@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, ;Nasreen Seria at nseria@bloomberg.net, Alister Bull, Ros Krasny

©2019 Bloomberg L.P.