Europe’s Weapon for Next Crisis Is Fiscal Policy, Blanchard Says

Europe’s Weapon for Next Crisis Is Fiscal Policy, Blanchard Says

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

Government spending must play a greater role in bolstering the euro-area economy in coming years, even if that means bigger budget deficits, according to Olivier Blanchard, the former International Monetary Fund chief economist.

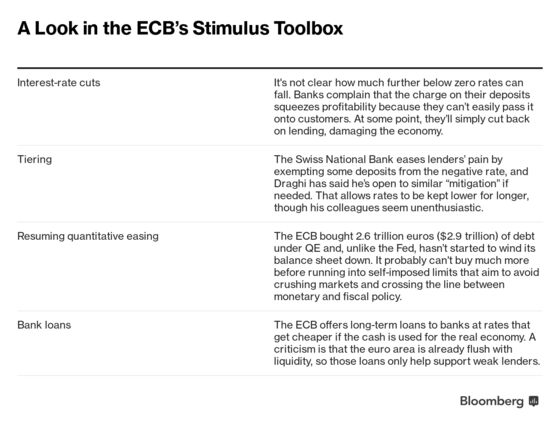

Speaking at the European Central Bank’s policy forum in Sintra, Portugal, Blanchard praised President Mario Draghi’s resolve in deploying negative interest rates, large-scale asset purchases and long-term bank loans to help the 19-nation region recover from the global financial crisis. But he also argued that those efforts have left policy makers with little room to handle future economic shocks.

“Surely there is not enough room to respond to even a run-of-the-mill recession,” Blanchard, who is now at the Peterson Institute for International Economics, told an audience of central bankers and economists. “Fiscal policy has a much more active role to play, and it is not yet equipped to do so.”

The question of how to cope with the next downturn has become more pressing as global growth cools under the pressure of trade tensions. The ECB says it’ll act if needed but, unlike the U.S. Federal Reserve, it has yet to move away from record-low interest rates and a QE-bloated balance sheet. Meanwhile, the European Union has maintained its pressure on nations to cut their deficits.

Instead, the EU should revisit its rules on debt targets, Blanchard said. If budget deficits are needed to sustain demand, they should be used for public investment or to finance structural reforms. Moreover, a case could be made to appoint “some form of minister of finance” to better coordinate monetary and fiscal policy.

Blanchard said that to ensure fiscal policy is sufficiently expansionary, governments could agree on a coordinated approach with each country issuing debt, similar to the global response to the 2009 financial crisis. Alternatively, member states could settle on a common budget financed by euro bonds, he said, acknowledging the “political difficulties” of that step.

EU finance ministers struck a deal this month on the design of a common budget for the euro area but ducked a key decision that will determine how much firepower it will have.

He also revived his call for the ECB to adopt a higher inflation target, saying he is “disappointed” the central bank hasn’t done so, especially given how it was able to change so much and keep its credibility in the past. The ECB has consistently fallen short of its goal of just under 2%.

“I realize that what I have offered is blue sky thinking, ignoring the complex euro geopolitics which will determine the outcome in the end. But it is the right place to start,” Blanchard said. “Monetary policy has transformed itself. Now is the time to do the same for the rest of the macro policy architecture.”

To contact the reporters on this story: Jana Randow in Frankfurt at jrandow@bloomberg.net;Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Paul Gordon, Brian Swint

©2019 Bloomberg L.P.