Europe’s Capitals Mull Recovery Loans With Eye on Soaring Debt

Europe’s Capitals Mull Recovery Loans With Eye on Soaring Debt

(Bloomberg) -- As the European Union seeks to disburse funds from its 750 billion-euro ($888 billion) recovery program as soon as next year, some of the countries hardest hit by the pandemic are struggling to work out how to best keep their finances in check once they take on billions of euros of new loans.

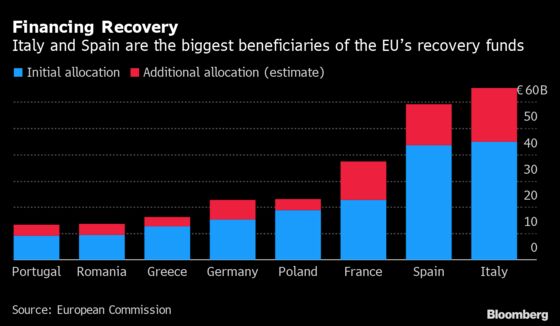

Spain, Greece and Portugal plan to focus on the grant portion first, which doesn’t need to be paid back, while they work out how to access the 360 billion euros of loans the EU will make available to member states as part of its stimulus package. Italy has indicated that it will request the full 128 billion euros of loans that it’s entitled to.

Economists and central bankers have encouraged the EU to ramp up spending in an effort to buoy the economy. The bloc even suspended its draconian fiscal targets until at least the end of 2021 due to the global crisis. But countries remain cautious because it’s unclear when they’ll have to bring their debt loads back into compliance.

“The grants need to be executed in the first three years so we will concentrate our efforts on investing these grants,” Spain’s Economy Minister Nadia Calvino said in Paris last week.

Hesitation over immediately tapping the loans comes as unprecedented spending has pushed borrowing levels above total output in southern European countries. Italy’s debt may jump to 158% of its gross domestic product this year, well above the 60% allowed under the EU’s rules. Spain’s is expected to reach 120% by year-end.

In an effort to keep the new borrowing from being reflected on its balance sheet, Greece -- whose debt may reach 197% of GDP by the end of the year -- is looking into using the EU funds to offer financial incentives to the private sector, such as through guarantees for cheap loans to companies, according to a government official, who asked not to be identified because the plans are private.

Portugal, whose debt is forecast to reach 135% of GDP next year, said it will minimize the use of loans that might lead to an increase in debt. The government is assessing using some of the loans for investments including capitalizing companies, according to a preliminary recovery plan.

There’s still a massive incentive for these countries to take loans from the EU, which can pass on its rock-bottom borrowing rates to member states. If Italy draws down all of the loans available to it, Rome would save about 1.4 billion euros in financing costs each year, according to Bloomberg calculations.

Grants First

While yields are low now, financing conditions could worsen in the future, accelerating the use of the EU-issued debt, says Raymond Torres, an economist with Spanish think tank Funcas.

“In the future, it’s possible that the gap widens between what countries can finance themselves at through the European loans and what they can get in the market,” Torres said. “It makes sense to start with the grants and then follow with the loans.”

Some countries, however, expressed hesitancy to use the EU’s loans due to the strings attached. Brussels insists that governments have to spend the loans and the grants on specific, EU-approved projects and they will be only disbursed once specific milestones are reached.

With the latest wave of restrictive measures casting fresh clouds over the economic outlook, prospects for a quick rebound next year are dimming, underscoring the importance of such funds in buttressing the region’s economies.

Yet EU governments are currently stuck in negotiations with the European Parliament over outstanding details of the plan, raising doubts about whether the first slice of funds can be distributed in the first half of 2021 as scheduled. An agreement between the two sides is needed to get the EU’s 1.8 trillion-euro budget and stimulus package over the line and operational by January.

©2020 Bloomberg L.P.