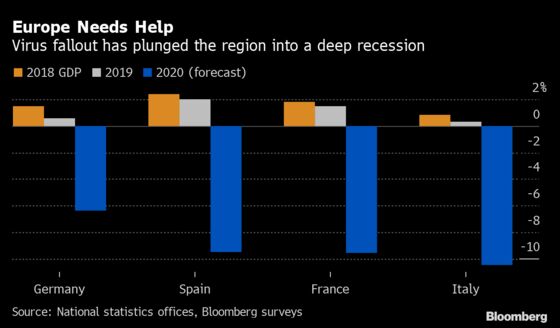

Europe Awaits German Fiscal Cascade That Could Be Just a Trickle

Europe Awaits German Fiscal Cascade That Could Be Just a Trickle

(Bloomberg) -- Germany’s stimulus is offering policy makers a real-time experiment on how much such national aid helps other countries too, just as the coronavirus forces the region to confront its lack of fiscal integration.

European Union leaders are working on their first-ever plan for joint borrowing to help the bloc’s more vulnerable countries. But until that’s agreed, the boost due to permeate through its biggest economy will remain the biggest single effort available for anyone else to benefit from in the current crisis.

With talks between governments on that common fiscal push set to intensify, gauging whether German stimulus is seeping into the rest of the euro area -- a so-called “spillover” -- could underscore how urgent an EU accord might be. It’s also a material question for the European Central Bank as it battles an unprecedented shock that has crippled growth and choked cross-border trade.

“There will be some knock-on effects,” said Christian Odendahl, chief economist at the Centre for European Reform in Berlin. “There’s an argument to be made that spillovers might be lower than they’d otherwise be because the trade links, particularly the service trade links, are limited.”

As the region’s economic motor and its most fiscally powerful member, Germany has the greatest capacity to deliver budget stimulus to its economy. That push is now taking the form of tax giveaways, spending on 5G data networks and railways, and incentives to build electric vehicles.

That stimulus is finally delivering what economists at the International Monetary Fund, the European Commission and the ECB long craved. Since September, ECB officials regularly urged countries “with the fiscal space” -- a label most aptly applied to Germany, which previously pursued balanced budgets -- to spend more.

However, evidence on whether such stimulus would help the rest of the region much was always mixed, and the current crisis may prove to be a new testing ground for debate on the matter.

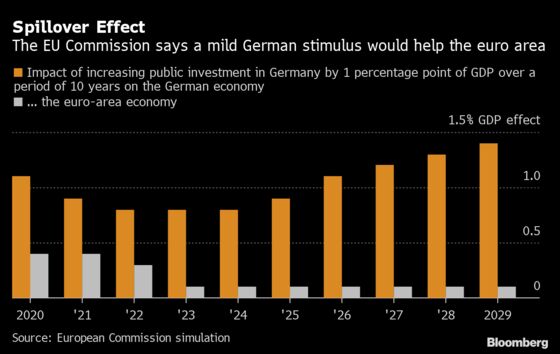

According to the work of Yuriy Gorodnichenko, an economics professor at the University of California, Berkeley who specializes in fiscal shocks, knock-on effects can be substantial. Moreover, the current downturn is propitious because such spillovers tend to be larger during recessions.

Meanwhile Odendahl, who says such effects are normally “quite sizeable,” is less sure this time because of the scale of the shutdown.

Virus Recovery |

|---|

Highlights of German Stimulus Plan (June)

|

Rescue Package (agreed in March)

|

By contrast, researchers at the IMF and the ECB have tended to conclude that such effects are more generally limited. A study by the Washington-based fund in 2017 calculated that on average, fiscal stimulus equivalent to 1% of a large economy’s output bumps up that of another country up by just 0.08% in the first year.

A report by the central bank in Frankfurt last year came to a similar view, acknowledging that the cross-border effects were “small.”

Germany’s Bundesbank is also skeptical of the big effects of spillovers and estimates that any effects from stimulus there would largely follow industrial trade routes: Hungary, the Netherlands and Poland would get more of a boost in percentage terms than France, Spain and Italy.

A more specific issue with the current fiscal easing is that some measures are particularly consumer-focused and domestic in scope, such as payments to families of 300 euros per child, and a sales tax-cut for the next six months, costing the government 20 billion euros.

The plan is also due to accelerate 10 billion euros in investment in digital, security and defense projects.

But soome long-term projects “are still a bit vague,” said Angel Talavera, an economist at Oxford Economics. “While some of them might in the end be quite beneficial, some of them might be a bit of a waste.”

As sizeable as the stimulus is compared to those offered by other countries, it’s also not as large as some economists might envisage. Last year, one German research institute called for spending of 450 billion euros on education, transport, infrastructure and climate over a decade to future-proof the economy.

The current plan is “not in itself big enough to result in significant higher growth in countries that will export to Germany,” said Aline Schuiling, an economist at ABN Amro Bank NV. “European initiatives are much more important.”

That’s where talks in Brussels later this month over a proposed 750 billion-euro plan to jointly finance an economic recovery may prove much more crucial for the continent’s growth prospects. With a bloc including the Netherlands frowning at the prospect that a portion of that sum will be given out in grants, officials are seeking a compromise.

Whatever happens in those talks, Odendahl says such an agreement is needed to help balance national economic policies with the common good for the region.

“We have quite sizable spillovers most of the time,” he said. “So this pan-European recovery boost is exactly what Europe needs -- because usually national policy makers don’t take these spillovers into account.”

©2020 Bloomberg L.P.