Emerging-Market Watchers' Obsession With Current Account Bites

Emerging-Market Watchers' Obsession With Current Account Bites

(Bloomberg) -- Emerging-market central bankers are taking stronger steps to rein in current-account deficits, even though they say the attention the market puts on this metric is all a bit unfair.

Two recent policy decisions in Asia illustrate the challenge. Indonesia and the Philippines raised interest rates last week to shore up their currencies and curb inflation risks. Both economies run current-account deficits of more than 3 percent of gross domestic product, making them reliant on foreign investment and therefore vulnerable to outflows when investor sentiment turns sour.

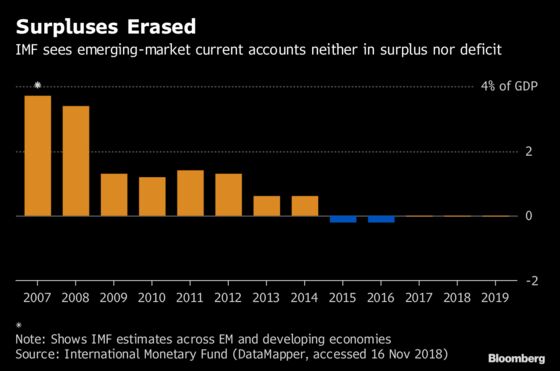

Market watchers are often fixated on whether the deficit, the broadest measure of trade in goods and services, widens or not to determine an economy’s vulnerability.

But much depends on the content of the deficit: whether the imports are used for sound investments on development projects like roads and rail, helping to improve the economy’s growth potential, as in the case of the Philippines and Indonesia. In the latter, consumer goods make up less than 10 percent of total imports.

Also, a narrowing in the deficit isn’t always a sign of good health. In the case of Argentina and Turkey, for example, recent improvements in trade balances are due to their crashing currencies -- down more than 48 and 29 percent this year, respectively -- and weak economies, which have put a brake on imports.

Funding the deficits have become more challenging this year because of Federal Reserve rate hikes, which have lured foreign investment away from emerging markets. While there was a brief lull after the U.S. policy makers held rates this month, more market volatility could be in store if the Fed proceeds with a December increase, the dollar continues to strengthen and U.S.-China trade tensions persist.

Here’s where eight emerging markets stand on their current accounts, and what related tensions are causing stress:

ASIA:

Indonesia

- The current-account gap widened to 3.4 percent of gross domestic product in the third quarter, and with another surprisingly strong trade deficit in October, the current account is set to remain elevated into the final three months of the year

- The government has raised taxes on some imports and delayed infrastructure projects -- many of which rely on equipment and materials from abroad -- in a bid to curb the deficit. Bank Indonesia has increased interest rates by 175 basis points in six moves since May, including an unexpected increase on Nov. 15, to help bring the shortfall down to below 3 percent this year

- “It’s not a sin to have a current-account deficit,” Indonesian Finance Minister Sri Mulyani Indrawati said Nov. 7 at the Bloomberg New Economy Forum in Singapore, adding that “the current-account deficit is not for consumption. It is a measure of infrastructure development” and investment that requires capital goods imports

- Reza Siregar, the head of Southeast Asia and India research at the Institute of International Finance, is among those seeing project delays as an unnecessary -- and harmful -- approach, since postponing much-needed infrastructure will reduce potential growth; better to change bloated fuel subsidies, he says

Philippines

- The current account swung from a surplus into a deficit in 2016 and has remained there on an annual basis since, reaching 3.6 percent of GDP in the second quarter, as President Rodrigo Duterte ramped up infrastructure spending in the Southeast Asian nation

- Government spending is outpacing fiscal plans due to infrastructure projects and will boost the economy, said Budget Secretary Benjamin Diokno, and underspending was previously a “weakness of the bureaucracy”

- That’s underpinned economic growth of more than 6 percent, but also fueled inflation, prompting the central bank to raise interest rates five times since May

- Deficit risks are more muted though because of strong foreign direct investment into the Philippines and the nation’s relatively small bond market that’s mostly held by domestic institutions, limiting outflow risk, according to Hoe Ee Khor, chief economist at Asean+3 Macroeconomic Research Office

- Still, the peso has lost almost 5 percent against the dollar this year

India

- Elevated prices of crude oil, the country’s biggest import item, are at the heart of India’s current-account woes, further triggering concerns about higher inflation and a weaker currency; the shortfall widened to 2.4 percent of GDP in the second quarter from 1.9 percent

- Remittances from abroad act as an intrinsic balance against rupee weakness, in turn lending some healing to the current-account deficit

- To curb the deficit, the government has slapped higher tariffs on imports, such as jet fuel, jewelry and communications gear. The central bank has raised interest rates by 50 basis points so far this year

- Nomura Holdings Inc. analysts see an “ample” pool of reserves to continue to draw from, and judge currency intervention as a better tool for India than interest-rate hikes, given benign inflation, weakening growth and a fragile financial sector

EUROPE/MIDDLE EAST/AFRICA:

Turkey

- Turkey’s $46 billion current-account deficit has long made it the most vulnerable among emerging markets to the changes in global financial conditions

- After currency meltdown, which made imports prohibitively expensive, Turkey posted a $1.83 billion current-account surplus in September, following on an August surplus, in the first back-to-back monthly surfeit since September 2015

- Shortfall should shrink to 2 percent next year from 4 percent in 2018, helped by “massive real effective depreciation,” according to a Nov. 6 research note from analysts at Bank of America Merrill Lynch

- Shrinking deficit comes at cost of economic growth slowing to 3.5 percent this year and 0.8 percent next year from 7.4 percent in 2017, according to analyst estimates compiled by Bloomberg

Russia

- Surging oil prices and a ruble weakened by ever-present threat of sanctions combine to set Russia’s surplus on track to beat 2008’s record of $104 billion, according to VTB Capital

- Assuming no major shocks from tougher U.S. sanctions, the ruble could strengthen to as much as 60 per dollar in the fourth quarter, according to ING Groep NV

- While signaling the nation’s healthy finances, the large current-account surplus makes it less urgent for President Vladimir Putin to take steps aimed at curbing Russia’s reliance on energy exports and diversifying the economy

South Africa

- South Africa depends on foreign portfolio inflows to finance its current account as FDI flows remain modest

- Deficit is seen widening to 3.6 percent of GDP in 2018 from 2.4 percent in 2017, and remaining at that level next year

- With 38 percent of the 1.97 trillion rand ($140 billion) of government bonds in foreign hands, South Africa is vulnerable to capital flight sparked by local factors -- which could include a credit-rating downgrade to junk -- and global headwinds such as U.S. rate increases

- Budget deficit set to widen and gross government debt forecast to rise to almost 60 percent of GDP in 2024

LATIN AMERICA:

Argentina

- Deficit reached 5.3 percent of GDP in the second quarter, the highest since the first quarter of 1994, fueled by the mounting fiscal deficit

- Shortfall was one of those “idiosyncratic” factors that meant the peso has declined more than any other emerging market currency this year

- With the country falling into second recession in three years, deficit will inevitably narrow as domestic demand for imports weakens

- First signs of that decline are already apparent, with imports tumbling to 19-month low in September, prompting the first trade surplus since December 2016

- Deficit should narrow further as recession deepens and agricultural exports rebound; some help also gained from rising gas production in the giant Vaca Muerta shale deposit

Colombia

- Tight monetary policy, sluggish growth and increased exports of other products helped more than halve a yawning current-account deficit in the past three years as oil prices rebounded

- Shortfall was 3.2 percent of GDP as of second quarter from 7.1 percent in the third quarter of 2015

- Many analysts cited Colombia as potentially the next domino to fall in the emerging market contagion, but it never happened and the currency is only down 6.6 percent this year

--With assistance from Masaki Kondo.

To contact the reporters on this story: Michelle Jamrisko in Singapore at mjamrisko@bloomberg.net;Philip Sanders in Santiago at psanders@bloomberg.net;Selcuk Gokoluk in London at sgokoluk@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, ;Dana El Baltaji at delbaltaji@bloomberg.net, Tomoko Yamazaki

©2018 Bloomberg L.P.