For Currency Traders, August Was No Day at the Beach

Emerging markets have been getting hammered this month. A less predictable Chinese yuan is only going to make things worse.

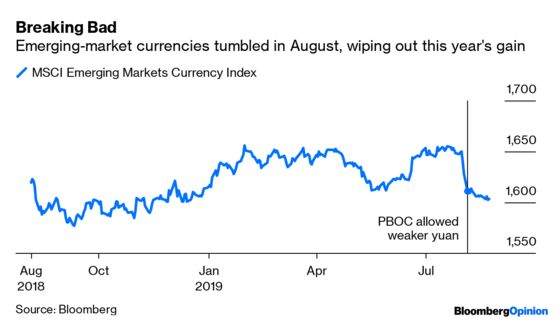

(Bloomberg Opinion) -- Emerging-market currencies are having their worst month since May 2016.

To confound matters, some of the usual rules of investing have broken down. When the global economic outlook is dimming, traders often sell currencies of small, open, trade-reliant economies – say, South Korea’s won – and cling to higher-yielding assets, such as the Turkish lira. This is driven by the so-called carry trade, when investors borrow money cheaply in low-rate markets to buy riskier assets.

That split isn’t happening right now: Emerging-market currencies are getting sold across the board.

But before you jump to blame the trade war, consider the elephant in the room: China, and its plans for the direction of the yuan.

For months, the yuan had been relatively steady, which helped anchor the currencies of China’s smaller trading partners. Then on Aug. 5, the People’s Bank of China surprised markets by allowing the yuan to weaken, prompting the U.S. Treasury to designate China a currency manipulator. The yuan has continued its slide, hitting an 11-year low Monday.

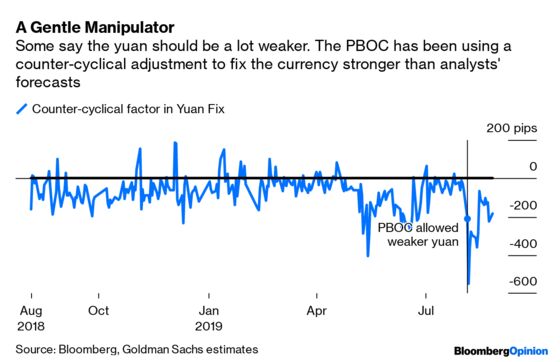

Things would be a lot easier if the PBOC let markets decide how the currency trades, yet the yuan remains heavily managed. Wary of capital flight – and perhaps still hopeful for a trade deal with the U.S. - Beijing hasn’t been very aggressive in its weakening path.

A case in point: One of the elements that determines the yuan’s daily fix is what’s known as the counter-cyclical adjustment. Even after this month’s abrupt weakening, China’s central bank has been using this factor to set its official exchange rate stronger than traders’ forecasts. Without it, the yuan fix would have been at 7.25 per dollar by now, estimates HSBC Holdings Plc, compared with 7.0570 earlier Monday.

So far, the yuan has been an effective weapon in this trade war, one that Beijing is using carefully. At a fixing of 7.25, a weaker currency could offset the current 25% tariff imposed by the U.S., HSBC says; and it would need to weaken to as much as 7.70 to counterbalance a 10% tariff on the remainder of China’s exports that currently bear no levy. So you could argue that after President Donald Trump’s weekend Twitter tirade, the fix should have been 8.0. Conversely, if things go swimmingly between Washington and Beijing – Trump on Monday said that China asked to restart talks – don’t be surprised if the yuan falls sharply below 7.0 again.

Meanwhile, the carry trade is no longer in fashion. Just like their peers in developed nations, emerging-market central banks are racing to cut rates. After slashing its benchmark rate by 425 basis points in late July, Turkey’s real rate, which accounts for inflation, hovers at just over 4%. The real rate in Indonesia has fallen, too – to 2.2% after two consecutive rate cuts. Are these paltry, single-digit yields worth the trouble? Just look at all the political upheaval in Argentina, which triggered the peso’s 31% slide this month.

August has always been a weak month for emerging-market currencies, as traders go on their summer vacations and illiquid markets become vulnerable to price swings. Maybe going to the beach is the only rational coping strategy after a testing summer of trade-war drama and China’s unpredictable currency moves.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.