Emergency Fiscal Action Debated to Cushion World Virus Shock

Governments struggling to contain the global economic fallout from the coronavirus outbreak

(Bloomberg) -- Governments struggling to contain the global economic fallout from the coronavirus outbreak face mounting calls to unleash a major fiscal stimulus that could help cushion the blow.

While some investors are already betting that the epidemic will warrant the first joint emergency monetary easing since 2008, a gathering throng of analysts is asking if budget aid in countries from China to Germany wouldn’t be more effective.

Such a prospect would raise memories of action by the Group of 20 in 2009 as they raced to stem the financial crisis, with what they described at the time as an “unprecedented and concerted fiscal expansion” pledged to total $5 trillion. It’s not clear if there’ll be a similarly synchronized response to the virus, though pressure for some sort of global effort is starting to grow and individual governments are already taking action.

“Rate cuts and significant rate cuts are not necessarily the right policy response to what’s happening today,” Jim McCormick, global head of desk strategy at NatWest Markets, told Bloomberg TV. “What you really need is a fiscal response, and the good news is we’re seeing some of that in Asia, we’re seeing talk of it in Europe, but so far not so much of it in the U.S.”

Group of Seven finance ministers agreed on Tuesday to take actions “including fiscal measures where appropriate” to support their economies, and said they’re “ready to cooperate further,” according to a statement they released.

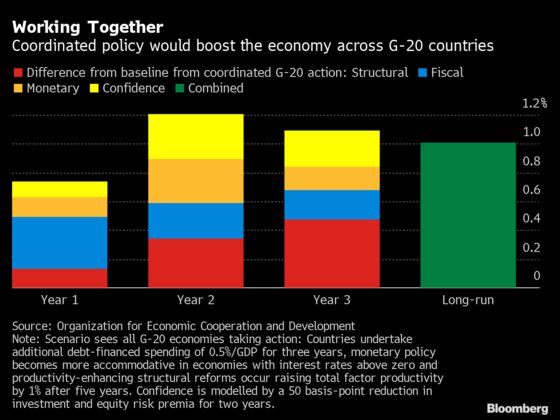

The Paris-based OECD described the scale of the challenge facing officials on Monday, warning that world economic growth is poised to slow to a pace not seen since 2009.

“Governments need to act immediately to contain the epidemic, support the healthcare system, protect people, shore up demand and provide a financial lifeline to households and businesses that are most affected,” OECD Chief Economist Laurence Boone said.

How aggressive governments are will depend on the ultimate fallout from the virus, said Chetan Ahya, chief economist at Morgan Stanley. But regardless of the size of shock, he predicts the fiscal deficit of the four major advanced economies plus China will rise to at least 4.7% of gross domestic product this year, the most since 2011 and up from 4.1% last year.

Among arguments for fiscal action are its ability to be help shore up demand more than monetary easing, and its more targeted nature, as opposed to the more general impact across the economy of central-bank stimulus.

One example of such measures is in Italy, by far the worst affected European country. The government is deploying tax credits, support for exporters and increased liquidity for businesses. That’s part of a stimulus that may cost at least 3.6 billion euros ($4 billion), adding to its already huge debt pile.

“There are instruments available, fiscal policy instruments or social policy instruments for such cases, like short term allowances, that we have used in the past and that have proved quite effective,” Bundesbank President Jens Weidmann told on Bloomberg TV on Friday. “This should be a debate addressed to fiscal policy makers.”

Another argument for budget stimulus is the severely depleted ammunition of monetary authorities -- most notably the Bank of Japan and the European Central Bank, whose interest rates are below zero.

Asia, where the crisis has been most devastating in its spread, has already seen a round of fiscal measures deployed, with the prospect of more to come. In China, the location of most virus cases, officials have pledged to cut taxes to help companies. That includes reducing or exempting value-added levies for firms providing essential goods or logistics, and more funds for provincial authorities.

“Probably the most important element for the markets going forward would be the fiscal component of what comes next, and in particular I think what comes next from China,” Yianos Kontopoulos, CQS Chief macro strategist, said on Bloomberg TV. “That’s where the epicenter still is.”

JPMorgan economists now forecast a fiscal boost worth 1% of GDP in China, with “material easing” also forthcoming in South Korea, Singapore and India.

Pressure is also building for budget action in Europe. ECB Vice President Luis de Guindos reiterated on Monday that such an effort -- rather than monetary policy -- should be the “main frontline of response.” European finance ministers are holding a conference call on Wednesday.

“A coordinated fiscal response needs to be very timely,” European Union economy chief Paolo Gentiloni told reporters in Brussels. “You can’t take it too early, you can’t take it too late.”

The virus crisis is heaping pressure on Germany, the euro region’s largest economy, to use its fiscal firepower built up from successive years of budget surpluses for the benefit of its neighbors. The finance ministry in Berlin said Monday that Germany has enough spending flexibility to react to economic crises without changing constitutional deficit limits.

In the U.S., the first line of defense currently appears to be interest rates rather than a budget push, which the economy has already experienced in a high dosage since President Donald Trump took office. Trump renewed his call for the Fed to lower rates in recent days and on Friday, Federal Reserve Chairman Jerome Powell opened the door to a cut with a rare statement vowing that the central bank would use its tools to support the economy. The virus and the upcoming presidential election may combine to provide the motivation for another tax cut.

Stimulus may also be imminent in Britain, which presents its budget on March 11. Fiscal loosening of around 1.5% of GDP was already planned before the current crisis, but Chancellor of the Exchequer Rishi Sunak said late on Monday that “we stand ready to announce further support where needed.”

For Carl Weinberg, chief economist at High Frequency Economics, monetary easing remains the preferable response -- and in any case, the push for galvanized action is doubtful.

“Increasing demand right now is not the right medicine,” he said on Bloomberg TV. “I don’t think that for the major economies anyhow that fiscal is going to be the game, and for any economy I think it’s a questionable way to go.”

--With assistance from Viktoria Dendrinou, Francine Lacqua, Matthew Miller, Tom Orlik (Economist), Catherine Bosley and Andrew Atkinson.

To contact the reporter on this story: Craig Stirling in Frankfurt at cstirling1@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Zoe Schneeweiss, Margaret Collins

©2020 Bloomberg L.P.