EM Rally Hinges on Draghi Being the Dove Traders Want Him to Be

Investors are looking for signs that the strongest rally in emerging markets in months is more than just a temporary reprieve

(Bloomberg) -- Investors looking for signs that the strongest rally in emerging markets in months is more than just a temporary reprieve will probably get it when the European Central Bank meets.

The monetary authority is set to unveil a fresh salvo of stimulus, which may further embolden traders to look for yield across emerging markets. More than 80% of economists surveyed by Bloomberg predict ECB President Mario Draghi will announce the central bank’s resuming bond buying, and forecasters see the deposit interest rate falling to a record minus 0.5%.

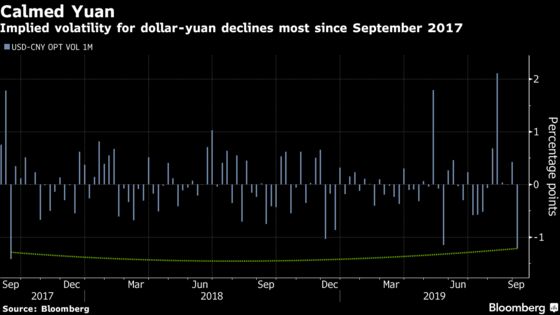

If those estimates are proven right, developing-nation stocks, bonds and currencies will probably extend a rally that was sparked earlier this month by the prospect of a meeting between U.S. and Chinese officials to discuss trade issues. The yuan’s one-month implied volatility fell last week the most in two years ahead of the 70th anniversary of the founding of the People’s Republic of China on Oct. 1.

“The ECB meeting on Thursday will be crucial for setting the tone of sentiment in emerging markets,” said Paul Greer, a London-based money manager at Fidelity International, whose emerging-market debt fund has outperformed 97% of peers this year.

The triggers of last week’s rally, “coupled with some cheap valuations in currencies after the August sell-off, make us tactically optimistic on the asset class for the next three weeks,” he said, adding that his fund is tactically overweight currencies and “more strategically overweight” credit and local duration in emerging markets.

Listen here for the emerging markets weekly podcast.

Turkey’s Big Cut

- Given the muted reaction from financial markets to the central bank’s 425-basis-point rate cut in July, slowing global growth, falling inflation and political pressure, the monetary authority will probably cut borrowing costs by 300-basis point this week, according to Bloomberg Economics

- “We are lowering and will lower interest rates to single digits in the shortest period,” President Recep Tayyip Erdogan said in a televised speech on Sunday. “After it falls to single digits, inflation will also slow to single digits”

- The lira has outperformed all of its peers this quarter

More Rates Decisions

- Economists see Bank Negara Malaysia maintaining its key rate at 3% on Thursday after the nation’s economy grew more-than-estimated in the second quarter

- ING Groep NV is among the minority, expecting a cut, arguing that Malaysia’s economy will find it challenging to outperform in an increasingly unfriendly external trade environment. The central bank last reduce interest rates in May. India, Thailand and Indonesia surprised markets last month with cuts

- The ringgit reached an almost two-year low last week

- Poland will probably keep interest rates on hold on Wednesday, while Serbia and Peru will decide on monetary policy a day later

Economic Data

- China will release a slew of key data in the coming week on credit growth, new yuan loans and money supply. Consumer and producer-price figures for August are due Tuesday. The latter fell below zero in July for the first time in nearly three years, sparking concerns over deflation

- Exports unexpectedly contracted in August, with sales to the U.S. tumbling amid the escalating trade war between the two nations. The offshore yuan weakened Monday after climbing four straight days through Friday, when the People’s Bank of China said it would cut the reserve ratio to the lowest since 2007

- “China would likely want to keep further yuan depreciation relatively modest ahead of U.S.-China trade talks,” said Patrick Wacker, a fund manager for emerging-market fixed income at UOB Asset Management Ltd. in Singapore. “As the Chinese measures announced on Friday indicate, they have a number of tools at their disposal short of yuan depreciation. While yuan depreciation is one of the more potent measures, it would likely antagonize the U.S. and lower the already slim odds of a breakthrough during scheduled trade talks”

- Taiwan said Monday that exports during August rose 2.6%, well above expectations and the fastest since October. The Philippines and India will report trade numbers later in the week

- India’s inflation, scheduled for Thursday, is estimated to have accelerated in August due to higher food and gold prices, according to Australia & New Zealand Banking Group Ltd. The central bank said last month the inflation outlook remains benign

- Attention will turn to Argentina’s national inflation reading for August on Thursday, which comes after an upset in the nation’s primary presidential vote and subsequent market sell-off. The peso is the biggest loser among emerging-market currencies this year

- Mexico’s inflation decelerated in August to the lowest level since 2016 and may push the central bank to cut its key rate again later this month. On Wednesday, industrial production data will likely point to a considerable level of slack in Latin America’s second biggest economy

- In Brazil, traders will watch July retail sales results for clues on the state of the nation’s economy. On Thursday, the central bank will post the result of its economic activity index, seen as a proxy for national GDP

--With assistance from Tomoko Yamazaki and Philip Sanders.

To contact the reporters on this story: Netty Ismail in Dubai at nismail3@bloomberg.net;Lilian Karunungan in Singapore at lkarunungan@bloomberg.net;Sydney Maki in New York at smaki8@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Shaji Mathew

©2019 Bloomberg L.P.