ECB Seen Readying the Pumps for Return to Massive Bond Buying

ECB Seen Readying the Pumps for Return to Massive Bond Buying

(Bloomberg) -- Financial firms including Goldman Sachs Group Inc. and Morgan Stanley are predicting that the European Central Bank’s flagship crisis-fighting tool will soon make a comeback.

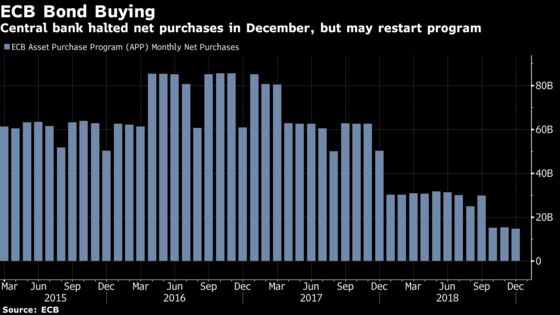

Policy makers could relaunch bond purchases as soon as September -- barely nine months after they capped the program at 2.6 trillion euros ($3 trillion), according to Evercore ISI’s Krishna Guha. Other institutions calling for the ECB to restart purchases by early next year include ABN Amro Bank NV, Danske Bank A/S, and BNP Paribas SA.

ECB President Mario Draghi said last month that officials will need to add monetary stimulus if the economic outlook doesn’t improve. The euro-zone economy has been stuck in a slump for more than a year, prompting some officials to say it’s no longer possible to consider the downturn a temporary blip.

While most investors and economists have penciled in a rate cut by September, their views on QE are more mixed. ECB Executive Board member Benoit Coeure, the head of market operations and a driving force behind QE when it was launched in 2015, said in remarks broadcast Monday that policy makers could “hypothetically” restart net asset purchases if circumstances make it necessary.

The latest boost to the likelihood of bond purchases, according to Guha, was last week’s nomination of International Monetary Fund chief Christine Lagarde to lead the ECB when Draghi steps down at the end of October. She has previously praised bond purchases as a policy tool.

That “certainly removes doubts in the eyes of the market as to whether the outgoing ECB president could muster support for one last big push before leaving office,” Guha said.

Here is a round-up of views on how the ECB might draw on QE to stimulate the euro-area economy:

Goldman Sachs

- “A return to large-scale QE is complicated by the ECB’s self-imposed limits on its asset purchases. But significant headroom remains to expand corporate sector purchases and we estimate that the ECB could buy up to 400 billion euros in sovereign debt under the current constraints”

- “A limited QE program -- for example, with monthly purchases of 30 billion euros for nine months -- seems feasible within the existing constraints”

Morgan Stanley

- “Sub-par growth and below-target inflation lead us to believe that the ECB now thinks that extra stimulus is warranted. This likely means reactivating its asset purchase program. When exactly and in what size is uncertain. While it could turn out to be different, our assumption is that the central bank could start buying something like 45 billion euros a month as early as the fourth quarter, with an announcement in September”

JPMorgan

- “At this stage, we do not expect more QE, but we emphasize that the visibility is extremely low in terms of the macro outlook and the ECB’s response to it”

ABN Amro

- “We expect the ECB to relaunch QE given the deterioration of the economic outlook and sliding inflation expectations. The second QE program could total 630 billion euros and run for nine months at 70 billion euros a month from January 2020 onward”

- “The new program could see relatively more purchases of national agency and regional bonds and corporate bonds. Within the public sector program, the issue(r) limit for sovereigns could be left unchanged, though it could rise for national agency and regional bonds”

BNP Paribas

- “We think the ECB will announce a 35-40 billion euros monthly pace of purchases in December for six to nine months, leaving the door open to a further extension, with risks of an earlier announcement”

- “The new QE program will concentrate on government bonds, in our view, complemented by purchases of private sector assets”

HSBC

- “The current growth and inflation outlook, alongside European Union politics, mean we don’t see an imminent restart of QE, although a shift in tone on technical constraints means a credible program is possible if downside risks crystallize”

Commerzbank

- “From the ECB’s standpoint, there are a number of reasons why net asset purchases should not be resumed. Even if the central bank were to raise the issuer limit from the current 33% to 50%, our calculations suggest that this higher limit would probably be achieved in roughly two years”

- “The ECB therefore has to use its ammunition very carefully, even though it officially stresses that this is not a problem”

Danske Bank

- “We now expect ECB to cut rates by 20 basis points, introduce a tiering system, extended forward guidance, and restart QE in a package which could come already in September”

- "Our baseline is that ECB will restart QE for the 12 months at a monthly pace of 45-60 billion euros a month"

To contact the reporters on this story: Carolynn Look in Frankfurt at clook4@bloomberg.net;Kristie Pladson in Frankfurt at kpladson@bloomberg.net

To contact the editor responsible for this story: Paul Gordon at pgordon6@bloomberg.net

©2019 Bloomberg L.P.