ECB Seen Boosting Bond Purchases to Avert Credit Market Meltdown

ECB Seen Boosting Bond Purchases to Avert Credit Market Meltdown

(Bloomberg) -- A savage sell off in corporate debt over the coronavirus epidemic this week is raising the prospect of the European Central Bank doubling down on the bond buying it uses to prop up the region’s economy.

The ECB needs to start expanding the purchases of corporate bonds it’s run since 2016 as soon as this week to restore calm to bond markets and head off any wider economic damage, according to George Saravelos, a strategist at Deutsche Bank AG.

The asset purchase program, also known as quantitative easing, is one of the most potent policy weapons left in the ECB arsenal as negative policy rates mean there’s limited capacity for further cuts.

Investors are increasingly working on the assumption that ECB President Christine Lagarde’s first big policy decision this week will see assertive measures to combat the coronavirus’s economic impact.

Priced In

Money markets are almost fully pricing in a 10-basis-point cut to the deposit rate, reversing earlier predictions of policy makers staying on hold for an extended period after the last announcement on Jan. 23. Most market participants expect the bank to go much further.

“The probability of the ECB announcing a package of policies has gone up, but the market will be underwhelmed by a package of several small measures,” Deutsche Bank economists Mark Wall and Marc de-Muizon wrote in a note. “The greatest market impact would come from fiscally-equivalent policy options, such as taking more risk by expanding private asset purchases or coordinating monetary and fiscal policy.”

The euro was down 0.5% at to $1.1395 on Tuesday, breaking a three-day rally. The shared currency reached $1.1495 on Monday, the strongest level in more than a year against the dollar. If the euro’s advance were to persist it could bother policy makers as it threatens to undermine growth in the export-heavy economy.

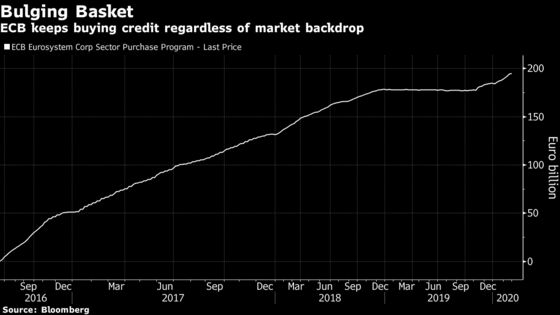

The ECB has amassed almost $223 billion of corporate debt in less than four years of QE, $20 billion of which has been added since it re-started net purchases in November.

“There is simply no capacity for the market to absorb a one-way exit from risky assets, especially credit,” Saravelos wrote in a note on Monday. “The ECB should ramp up its corporate bond QE program this week.”

The bank could increase the overall size of its QE or broaden its scope to include riskier categories of bank debt. Until now, it has only bought lenders’ relatively safe covered bonds and asset-backed securities.

“In times of stress, actions previously deemed impossible or unlikely can become part of a possible equation,” Jeroen van Den Broek, ING Groep NV’s head of credit research and strategy, wrote in a note Monday.

Making bank notes eligible for QE would massively swell the volume of debt the ECB could buy as they account for about 30% of European investment-grade corporate bonds, according to Wolfgang Bauer, a portfolio manager at M&G Ltd. He believes bank bond purchases would soften the blow of any further rate cuts, which have already been squeezing lenders’ profits for years.

The market for swaps insuring exposure to European banks isn’t yet pricing in that possibility, however. The cost of insuring senior bank debt has rocketed to the highest since 2016 in recent days, according to a Markit iTraxx index.

“Euro credit markets are currently caught in a tug-of-war between ‘pandemic recession’ fears and policy stimulus hopes,” said JPMorgan Chase & Co. analysts led by Matthew Bailey. They expect a temporary increase to 6-9 billion euros ($7-10 billion) of credit purchases for three months to support valuations of QE-eligible bonds.

--With assistance from Anooja Debnath.

To contact the reporters on this story: Tasos Vossos in London at tvossos@bloomberg.net;Alice Gledhill in London at agledhill@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Chris Vellacott, Hannah Benjamin

©2020 Bloomberg L.P.