ECB’s Next Step Hinges on Who to Believe on Future Inflation

The ECB’s next move to cope with the deepest downturn in decades could turn on whether it listens more to consumers or investors.

(Bloomberg) -- The European Central Bank’s next move to cope with the deepest downturn in decades could turn on whether it listens more to consumers or investors about the risk of deflation.

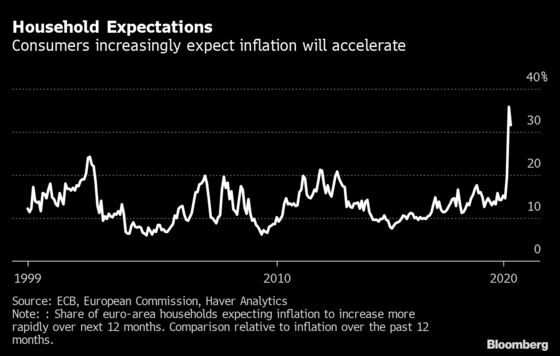

Executive Board member Isabel Schnabel highlighted the dilemma last week when she noted that financial markets have been pricing in “significant risks” of a downward spiral in prices because of the coronavirus, while households expect just the opposite.

The question of who’s right matters hugely for the ECB because policy makers have justified their unprecedented support by saying it’s geared toward their mandate of price stability, defined as inflation “below, but close to, 2%.”

Economists globally are debating whether this crisis will be inflationary or deflationary. Some say demand will be so slow to recover that prices will have to fall. Others predict they’ll be driven higher as the flood of money from fiscal and monetary stimulus meets reduced supply because of social restrictions and bankruptcies.

Multiple ECB officials have said their decision this month to extend and almost double their pandemic bond-buying program was motivated by fear that prices will start a broad-based decline.

That means they were more swayed by market indicators showing investors have ramped up bets that prices will fall over the next few years.

Those bets have retreated somewhat since the worst of the lockdowns, but they echo the pattern in late 2014 and early 2015 when the ECB’s then-president, Mario Draghi, made a dramatic push to stave off deflation with quantitative easing.

Yet some ECB policy makers dispute that deflation is likely, suggesting they think households are right. The central bank has even previously acknowledged that consumers are normally the better judge of inflation trends -- they dramatically overestimate the rate, but get the direction right.

That’s partly because they’re the ones buying the goods and services. If consumers fear their costs will rise, they’re likely to make purchases immediately rather than wait, which boosts demand and puts upward pressure on prices.

“Markets have moved more toward ‘believing it when we see it,’” says Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence. “For households, the key is energy and food that drives their expectations and can drive spending patterns.”

Read more on how on how markets are pricing deflation risks

What’s critical is whether this time is different. Even if they expect prices to rise, consumers are fearing for their jobs and their health because of the pandemic. The evidence so far is that they’re hoarding cash and showing little willingness to spend.

Investors have good reason to be wary. The ECB has fallen short of its inflation target for years, even in good times for the economy. Officials cite factors such as globalization, technological change, and an aging population that put downward pressure on prices.

Executive Board member Fabio Panetta said in an interview with Le Monde published Tuesday that “based on the inflation outlook, I expect a prolonged period of very accommodative monetary policy” -- but a clearer picture is needed before the ECB can decide whether to deploy more firepower.

Schnabel said households’ inflation expectations suggest they’re unlikely to retrench even further, meaning the risks of so-called second-round effects that cause lasting damage to the economy are “very limited.” But she also said the ECB’s action was appropriate.

Attention will now likely turn to whether fiscal stimulus programs by governments will help unlock savings as lockdowns are eased and shops reopen.

Sales-tax cuts, payouts for families with children and subsidies for purchases of cleaner cars are among the incentives politicians are banking on to encourage consumers to spend.

If that doesn’t work, the ECB may find it’s called back into action. Economists and investors are generally betting it will be, with another increase in bond purchases perhaps as soon as September.

“What happens to inflation ultimately comes down to consumer confidence and when will they spend on the back of the coronavirus,” said Piet Christiansen, chief strategist at Danske Bank. “We are in unprecedented territory, and as such we should take all indicators with a pinch of salt these days.”

©2020 Bloomberg L.P.