ECB's Knot Says Economy Doesn't Yet Warrant Resumption of QE

Draghi primed investors after July’s meeting to expect some form of stimulus, saying the outlook is “getting worse and worse”.

(Bloomberg) --

European Central Bank policy maker Klaas Knot said the euro-area economy isn’t weak enough to warrant the resumption of bond purchases and such a step shouldn’t be taken unless the slowdown worsens.

While the Dutch central-bank governor said he’s open to an interest-rate cut, his remarks echo those by his German colleague Jens Weidmann and suggest President Mario Draghi will have a fight on his hands if he’s planning a strong package of monetary stimulus at the ECB’s Sept. 12 meeting. Investors have stepped up predictions that he’ll deliver lower rates and resume quantitative easing.

“If deflation risks come back on the agenda then I think the asset-purchase program is the appropriate instrument to be activated, but there is no need for it in my reading of the inflation outlook right now,” Knot said in an interview in Amsterdam on Thursday. “Not reactivating the asset-purchase program also means you keep some powder dry for when actually future contingencies happen.”

European bond yields jumped on the comments. The euro erased its earlier decline to trade at $1.1076 at 4:44 p.m. Frankfurt time.

Draghi primed investors after July’s meeting to expect some form of stimulus, describing the economic outlook as “getting worse and worse” and ordering ECB staff to examine all policy options. He’ll be acutely aware that failure to deliver a large stimulus package risks tightening financial markets -- potentially driving the euro and bond yields higher -- and worsening the already-protracted slowdown.

His successor from Nov. 1, Christine Lagarde, weighed in with written answers to a European Parliament questionnaire published Thursday. She said the ECB hasn’t hit the lower bound on rates, and has a “broad toolkit” which it can and should use to tackle a downturn.

While another rate cut is widely predicted, banks including Goldman Sachs, Nomura, and ABN Amro have also predicted a new round of QE. Societe Generale said this week that it now sees the ECB cutting the deposit rate by 20 basis points to minus 0.6% and announcing that it’ll start buying 40 billion euros ($44 billion) a month of debt.

Finnish Governor Olli Rehn fueled the increasingly heated debate when he called for an “impactful” package that overshoots expectations.

What Bloomberg’s Economists Say

“Persistent weakness in the CPI data, a decline in inflation expectations and a lower path for global oil prices, as implied by futures markets, will likely prompt the ECB to revise down its inflation forecast, and announce a large stimulus package in September.”

--Maeva Cousin

Read her EURO-AREA PREVIEW

The region has shown little sign of escaping the downturn. Germany, the largest economy, reported rising unemployment and weaker inflation on Thursday as it teeters on the edge of recession. U.S. President Donald Trump has persisted with protectionism and railed against the weakness of the euro, and the U.K. is headed for a potentially disorderly Brexit on Oct. 31 that would hit continental businesses.

Euro-zone consumer-price data due Friday is expected to show inflation at 1%, far below the ECB’s goal of just under 2%.

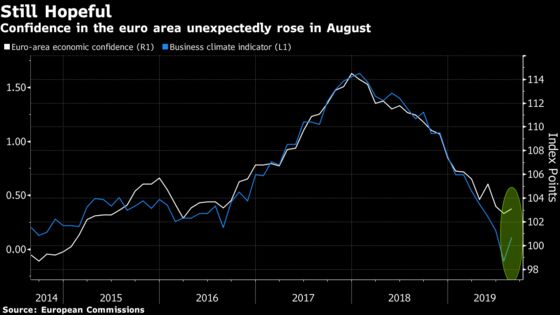

Yet there are occasional bright spots. Euro-zone economic confidence unexpectedly improved in August and the French economy grew faster than initially estimated in the second quarter.

QE was capped at the end of last year after 2.6 trillion euros of purchases, with the ECB shifting its focus to simply reinvesting the proceeds of bonds as they mature. Knot said there was no “valued added” in launching a package of measures.

“The market expectations are overdone,” he said. “If stimulus is warranted to protect the resilience of domestic demand then I think conventional policy easing would be the appropriate instrument to contemplate -- so a rate cut.”

SocGen also predicts a measure to soften the impact of negative rates on banks. Draghi has said the ECB will consider steps such as exempting some bank reserves from the charge, which compresses banks’ profitability and threatens to hinder their lending to companies and households. Knot said he’d be “reluctant” to support such a move unless there is a strong monetary-policy rationale.

Bundesbank President Weidmann said in a newspaper interview published last weekend that would be “wrong for us to act for action’s sake” and that speculation over large stimulus “doesn’t do justice” to the latest data.

Credibility Risk

Such resistance from the German central banker has been a regular feature over the years and is unlikely to be enough in itself to thwart any plans by Draghi. Still, if that view is also held by Knot as well as traditional policy hawks such as Executive Board members Sabine Lautenschlaeger and Yves Mersch, the next meeting could turn contentious.

Slovak Governor Peter Kazimir, a former politician who joined the ECB this year, highlighted the threat any significant dissent poses, when he said officials will need to muster “broad unity” in favor of more monetary stimulus if they are to make it credible. Knot signaled he’s not there yet.

“We don’t have deflation risks and we don’t even have recession, but we still have Brexit uncertainty looming and that is not going to be resolved by Sept. 12,” he said. “If we stay in this somewhat-below-potential growth world, the next shock might actually take us into recession, and what do we do then?”

--With assistance from Kristie Pladson.

To contact the reporters on this story: Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net;Ruben Munsterman in Amsterdam at rmunsterman1@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Zoe Schneeweiss

©2019 Bloomberg L.P.