ECB’s Kazaks Sees Prospect of Faster Inflation Than Forecast

ECB’s Kazaks Sees Prospect of Faster Inflation Than Forecast

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

The euro area’s inflation outlook may turn out higher than currently anticipated if the coronavirus doesn’t inflict any further shocks, according to European Central Bank Governing Council member Martins Kazaks.

The region’s stabilizing economic recovery, persistent supply bottlenecks and rising expectations all point to possible faster-than-forecast price gains, he said in an interview on Thursday. Just last week the ECB revised up its inflation projections through 2023, citing improvements in the outlook as one reason to pare pandemic bond buying.

“If Covid does not surprise on the negative side, there is some upside for the inflation outlook over the medium term,” said Kazaks, the governor of Latvia’s central bank in Riga. He cautioned that “I am talking about decimals here,” and he doesn’t yet see inflation at or above the ECB’s 2% goal over the medium term.

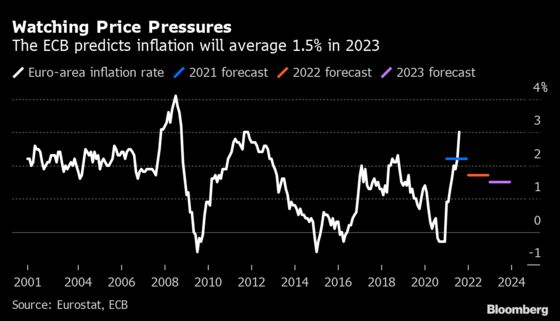

The euro region is now enduring the fastest price increases in a decade, with a rate of 3%. Officials view that spike as largely transitory, expecting inflation to average 2.2% this year and slow to 1.5% by 2023.

“There is perhaps some upside for those numbers to be revised up in the following forecasting rounds,” Kazaks said. “I agree with the current outlook, but I would say that the balance of risks for inflation are somewhat on the upside.”

After he spoke on Thursday, the ECB dismissed a Financial Times report that said Chief Economist Philip Lane told analysts privately officials expect to reach the target by 2025.

Gabriel Makhlouf, another Governing Council member, said Friday that “fears of excessive euro-area inflation are overstated.” Policy makers, however, need to remain vigilant “so that we can react as necessary if conditions change,” he said.

European bonds remained under pressure after Kazaks’s comments, with 10-year German yields rising two basis points to -0.28%. The euro rose 0.1% to $1.1781.

Wage Pressure

“We hear some anecdotal evidence that there could be some wage pressures down the road, but we have not seen that yet in the data,” he said. “There is no reason to expect that inflation would be permanently very hot. If at some point inflation will be significantly higher than our strategy and monetary-policy mandate, then of course we will know how to react.”

For now, ECB President Christine Lagarde insists that the Governing Council’s decision to “moderately” slow stimulus at its Sept. 9 meeting “isn’t tapering,” an emphasis that sets the Frankfurt-based institution apart from the Federal Reserve and the Bank of England, which are both closer to winding down stimulus.

Policy makers are in no rush to start such a debate, Kazaks said, with their 1.85 trillion-euro ($2.2 trillion) pandemic purchase program currently set to run until at least March 2022.

Officials will try to inform financial markets on the future of the measure “as soon as it is reasonably feasible,” he said, adding that “uncertainty is still high and it is reasonable to maintain flexibility.”

“At the current moment, monetary support is still necessary, fiscal support is still necessary,” Kazaks said. “But as the economy improves, the support needs to be withdrawn so that when the next crisis comes, we have again room to intervene.”

The Governing Council has yet to discuss whether and how it will apply the greater flexibility of its pandemic program to an older asset-purchase tool in future, he said.

Kazaks also argued that it will eventually be important to revisit the institution’s guidance on how soon after ending bond buying it would be willing to raise interest rates. So far, the ECB has said asset purchases will end “shortly before” interest rates begin to rise.

Some policy makers are concerned that by having delayed expectations for an interest-rate hike at their July meeting, that could also signal a longer-term commitment to asset purchases.

“In the past, this link was used to strengthen forward guidance,” he said. “We now have a much stronger and clearer strategy and also a more forceful forward guidance, therefore this link is not that crucial anymore.” Still, “we shall discuss it and try to avoid the risk of the markets misunderstanding us.”

| Read more: |

|

©2021 Bloomberg L.P.