ECB Out-Doving Fed Boosts Euro’s Allure as Carry Trade Funder

Traders are betting the Fed will hike interest rates 25 basis points by the beginning of 2023

(Bloomberg) -- Jackson Hole sharpened the contrast between a Federal Reserve telegraphing an end to stimulus and a dovish European Central Bank. For the euro, that means its status as a preferred funding currency just got a boost.

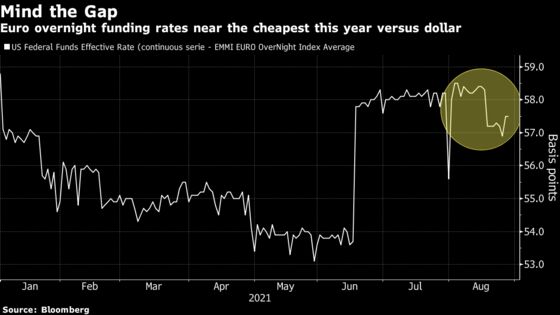

The discount on the overnight rate to borrow the common currency instead of dollars rose earlier this month to the most since 2020. That juiced up returns on carry trades funded by the euro, which have been some of the best performers this year.

That trend got extra legs on Friday after Federal Reserve Chairman Jerome Powell said it could be appropriate to start scaling back its $120-billion-a-month bond-buying program this year, though the central bank won’t be in a hurry to begin raising rates thereafter. That approach is miles ahead of the ECB, which said large-scale bond buying will continue next year, even after emergency asset purchases end.

“If the ECB was to persist in dovishness versus other central banks over the next few years, this would increase the attractiveness of the euro as a funder,” said George Saravelos, global head of FX research at Deutsche Bank in London.

Euro Funding

Against this backdrop, Brandywine Global Investment Management says it’s using the common currency instead of the dollar to finance purchases of emerging-market currencies. Nordea Investment Management sees it as a trend that’s bound to gain traction.

Traders are able to finance positions in higher-yielding assets using the euro at a rate of minus 0.48% overnight versus 0.09% for equivalent dollar funding, often seen as the default option for investors in the developing world.

What’s more, they can rest easy that their investments are less likely to get derailed by a sudden shift in outlook. ECB officials are still erring on the side of more stimulus even as they signaled this week that their latest shift in forward guidance doesn’t necessarily mean a longer period of low interest rates.

“We’re not using the dollar as a funding currency –- it’s really the euro and the yen,” said Jack McIntyre, a Philadelphia-based money manager at Brandywine Global Investment Management, who has an underweight position in the common currency to finance purchases of emerging-market crosses.

Already this year, volatility-adjusted carry trades funded with euros delivered positive returns for 17 out of 23 emerging markets tracked by Bloomberg. The same measure for those funded by the greenback have delivered losses for 15 of them.

While a bulk of that performance can simply be explained by the euro’s weakness -- it has dropped about 5% against the dollar since the beginning of the year -- it also underscores the impact of the widening policy divergence across the world’s biggest central banks.

It’s a rift that’s poised to remain wide -- according to market pricing -- as Powell cited the U.S. economy’s progress toward the Fed’s inflation objective, even as he indicated a careful assessment of incoming risks related to the Covid-19 delta variant.

Indeed, the discourse in financial markets is already beginning to shift away from when the Fed will start tapering its asset purchases, to how quickly they’ll wrap up the operation.

‘Relative Margin’

“Since the Fed is sounding relatively more hawkish, it brings the relative margin of policy to the forefront,” Brandywine’s McIntyre said. He is betting that the global economy gets past the delta variant relatively unscathed, that the U.S. continues to experience robust growth into 2022 and that China adds stimulus to its economy.

That backdrop would lead to a payoff for riskier currencies such as the Chilean peso, the Mexican peso, the Brazilian real, the Malaysian ringgit and the ruble, he said.

Traders are betting the Fed will hike interest rates 25 basis points by the beginning of 2023, while the ECB isn’t expected to increase the deposit rate until 2024.

“Short-term, this Fed-ECB divergence is quite disruptive as it contributes to tightening global monetary conditions via a stronger dollar,” said Witold Bahrke, a senior macro strategist at Nordea Investment Management.

But over the medium term, the euro should continue to “gain attraction” as a funding currency, since the ECB will stick with its ultra-easy policy, he said.

Next Week

- Inflation prints for the euro zone and Germany will be in focus. U.S. non-farm payrolls are due Friday, which could provide further clues on the shape of the recovery and central bank policy responses.

- Sovereign issuance from the Netherlands, Italy, Germany, France, and Spain should amount to an above-average total volume of about 30 billion euros ($35 billion), according to Commerzbank strategists. Still, net supply should turn into negative territory, with 48.3 billion euros of backflows due from Germany and Italy, they said.

©2021 Bloomberg L.P.