ECB Has Five Reasons to Delay Stimulus Decision to September

Markets see roughly 30% chance of a rate cut on Thursday.

(Bloomberg) -- European Central Bank policy makers have plenty of reasons to wait until September before committing to more stimulus.

In the run-up to their meeting on Wednesday, Governing Council members have said that additional support measures are available, if needed, to boost the euro zone’s ailing economy. That would be the latest in a number of policy shifts across the world toward more monetary easing.

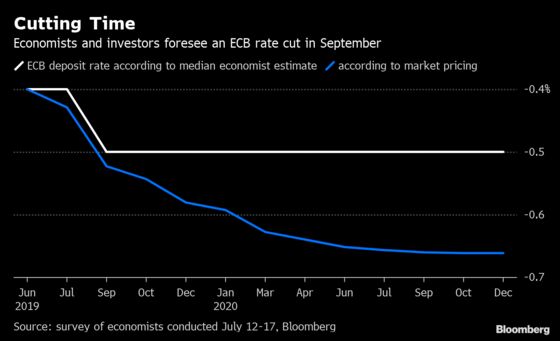

ECB President Mario Draghi might be tempted to appear proactive and present a package of changes already this Thursday. Traders in money markets are currently pricing roughly a 30% chance of a 10 basis-point cut in the deposit rate.

Most economists though expect officials to adapt their policy language first to hint at lower interest rates, before following through at the subsequent meeting in September with a reduction and a pledge to restart asset purchases. The following arguments favor waiting until after the summer break:

1. Awaiting the Federal Reserve

The ECB’s counterpart in the U.S. looks primed to lower interest rates by a quarter percentage point next week, in its first reduction in borrowing costs in more than a decade. Investors were previously pricing in a larger cut before some policy makers pushed back against such a step amid still-resilient economic data.

Should the Fed surprise with an aggressive move or signal the start of an easing cycle, the euro could appreciate. That would put downward pressure on euro-zone inflation and damp exports, enfeebling the economy even more. It may be worth waiting to see what U.S. officials do to formulate a response, particularly because the ECB has less room to lower interest rates.

“A rate cut in particular would be warranted if there is a unwarranted tightening in the euro-zone financial conditions -- that tightening could take the shape and form of stronger euro/dollar potentially on the back of a Fed rate cut,” said Valentin Marinov, Credit Agricole’s head of Group of 10 research and strategy. “We expect that the Fed will lead the way cutting rates with the ECB one step behind them.”

2. Economic Data

An economic report on Wednesday showed the slowdown worsening in July, with German factories in a particularly steep slump. That boosts any argument for a rapid response by the ECB.

Still, some key figures will only come after the July meeting, including second-quarter growth and fresh inflation readings. While policy makers typically have access to more granular statistics than financial-market participants, any extra information on how long the region’s manufacturing-led slowdown may last should be helpful in calibrating a response -- particularly with more recent data showing a mixed picture.

3. Fresh Forecasts

The ECB tends to announce major policy shifts when it unveils fresh economic forecasts, as the revised outlook supports the rationale for adding or cutting back on stimulus. The next update is due in September.

The previous round in June foresaw inflation averaging 1.3% this year and only 1.6% in 2021, yet that assumed slightly stronger price growth in the second quarter than what ultimately occurred. Revisions of the projections may therefore be underway.

4. Market Expectations

While policy makers say they don’t cater to market expectations, it’s hard for them to be entirely ignored.

Investors aren’t fully pricing in a 10-basis-point rate cut until September, and an early move could signal the economic situation is worse than currently perceived. Some ECB officials already classified market participants as too pessimistic at last month’s meeting, and may want to avoid painting an overly negative outlook.

5. Complexity of Package

Finally, the measures the ECB looks likely to announce will require careful consideration on how to implement them. Most analysts argue a lower deposit rate -- which is already at minus 0.4% -- will require a mechanism to exempt some bank deposits from the charge. There are a lot of different ways so-called “tiering” of reserves could be done. So far, policy makers haven’t expressed any preferences.

What Bloomberg’s Economists Say

“We expect the Governing Council to exempt 10% to 50% of excess reserves from the charge to cushion the impact.”

--David Powell. See his ECB INSIGHT

The ECB might also need to tweak its self-imposed rules to allow for further bond buying, and could take some time for ascertaining any legal ramifications.

--With assistance from John Ainger, Anooja Debnath and James Hirai.

To contact the reporter on this story: Carolynn Look in Frankfurt at clook4@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Jana Randow

©2019 Bloomberg L.P.