ECB Has Messaging Problem as Lagarde-Lane Signals Muddy View

The European Central Bank is struggling to make its intentions clear to investors in its response to the virus recession.

(Bloomberg) -- The European Central Bank is struggling to make its intentions clear to investors at a critical juncture in its response to the coronavirus recession.

Economists and investors see mixed messages from the ECB’s top policy makers. Most important is a perceived disconnect between President Christine Lagarde’s press conferences after policy decisions, and blog posts by Chief Economist Philip Lane the following day.

National central bank officials have taken note, expressing concern privately that such a dynamic risks undermining Lagarde’s credibility just as the ECB gears up for talks on whether to increase monetary stimulus. The officials asked not to be identified because internal deliberations are confidential.

The Frankfurt-based institution has even considered whether to change the practice of publishing a blog by Lane after the policy decision, according to euro-area officials.

An ECB spokesman declined to comment.

The ECB’s communication challenge is all the more important right now as the euro area faces extraordinary uncertainty. Rising coronavirus infections are forcing new restrictions, while consumer prices are falling and under further downward pressure from a jump in the euro.

Any verbal confusion can tighten financial conditions and make the economic recovery from the pandemic even harder to sustain.

“The impression is that the chief economist and president don’t send the same message on policy and that is creating some mismatch,” said Piet Christiansen, chief strategist at Danske Bank A/S. “It’s difficult to gauge if the president and chief economist are perfectly aligned.”

Lane’s blogs started in March to provide the economic rationale for decisions, and he has published them after all but one of the president’s press conferences since then.

The officials said there are no fundamental differences in policy approach between the two, adding that any perceived ambiguity by Lagarde may reflect her desire to convey the sometimes-conflicting views of Governing Council members.

Consequently, the president can appear relatively sanguine in her press conferences about the policy challenges, while Lane’s blogs have been more pointed.

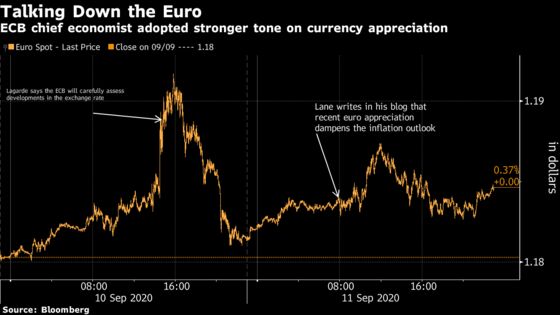

For example, the euro rose on Sept. 10 when the president signaled no pressing need for a monetary response to the strengthening currency. Lane, who had earlier said the exchange rate “does matter,” wrote the next day that it has “significantly muted” inflation.

“Certainly the market was surprised by the differing statements on euro appreciation,” said Neil Jones, head of foreign-exchange sales to financial institutions at Mizuho Bank. “The price action said it all.”

That was reminiscent of an incident early in the crisis when Lagarde stunned markets by saying the central bank wasn’t there to shield the debt of the most-vulnerable nations.

Italian borrowing costs immediately jumped, Lagarde tried to walk back the remarks the same day, and Lane wrote the following day that the ECB would “not tolerate” such risks. Other policy makers followed suit.

A surprise appointment to the presidency, given that she has never worked at a central bank, Lagarde joined last November promising to build consensus after divisive spats among policy makers under her predecessor, Mario Draghi.

Since her gaffe in March on bond yields, she has taken to reading carefully from written statements in her briefings, openly admitting in June that she does so to be “very, very specific.”

That strategy has also raised concern among some officials, who are concerned that repeatedly reading from notes doesn’t deliver the policy message as convincingly as needed.

With 25 policy makers, the ECB is prone to cacophony. More signals are due this week with speeches by officials including Lane and Lagarde, and the account of last month’s policy meeting.

Recent comments include Vice President Luis De Guindos saying there is no imminent need to bolster stimulus, Executive Board member Yves Mersch seeing no sign of economic deterioration, and their colleague Fabio Panetta signaling support for preemptive stimulus. Bank of Spain Governor Pablo Hernandez De Cos said there is “no room for complacency.”

A report on Monday showed Germany, Europe’s largest economy, faring better than most of its neighbors. Yet Bundesbank President Jens Weidmann, typically seen as wary of extensive stimulus, said “ample” liquidity is still needed so that knock-on effects from the crisis “cannot intensify and entrench economic problems.”

“The markets like the Lane blog, Panetta speech and De Cos soundbite because they confirm what the market believes must happen,” said Richard Barwell, an economist at BNP Paribas Asset Management. “The market has concluded that it knows what the ECB will do, and can cherry pick.”

Central Banker JeopardyLagarde is far from being the only top central banker to struggle with communications. |

|

©2020 Bloomberg L.P.