ECB Dream of German Fiscal Firepower Effect Isn't Too Proven

ECB Dream of German Fiscal Firepower Effect Isn’t Really Proven

(Bloomberg) --

If Germany does open its fiscal taps to unleash a major stimulus, it’s not clear how far that will benefit any economy other than its own.

Seeking a German budget boost has become a priority for European Central Bank policy makers wanting to add thrust to their own monetary easing, and outgoing President Mario Draghi is likely to plea for help again from governments at his final decision this week. But the evidence that it would trickle beyond the country’s borders is mixed.

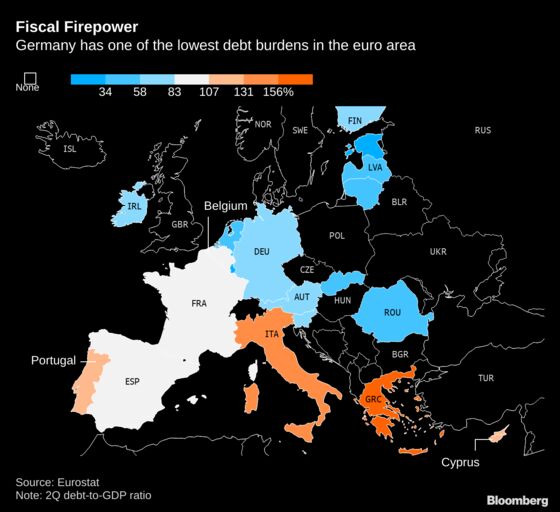

It’s no surprise that Draghi and his successor, Christine Lagarde, look at the fiscal firepower of Europe’s largest economy with such yearning, since Germany has one of the region’s lowest debt burdens, while the institution’s own toolkit is depleted. ECB officials would dearly love that budget muscle to be flexed for everyone’s benefit.

Yuriy Gorodnichenko, an economics professor at the University of California, Berkeley who has researched fiscal impacts, reckons a rising stimulus tide in Germany would indeed lift all boats with a noticeable result.

“My sense is it’s a big number,” he says. “Others will disagree.”

Such divergence in the field was acknowledged in a 2017 paper by three ECB officials. They said so-called fiscal spillovers are “largely debatable” -- in terms resembling former Federal Reserve chief Ben Bernanke’s description of quantitative easing as working in practice, but not in theory.

“The evidence derived from macroeconomic models suggests that the spillovers are small,” the ECB paper said. “Empirical studies, in contrast, tend to be more robust and support the existence of significant spillover effects.”

A 2016 European Commission analysis reckoned an increase in German and Dutch public investment of 1% of GDP would generate output spillovers to the euro area of as much as 0.5%. A paper the previous year by former IMF Chief Economist Olivier Blanchard and colleagues found “a large and positive impact” in the region’s periphery of fiscal expansion at its core.

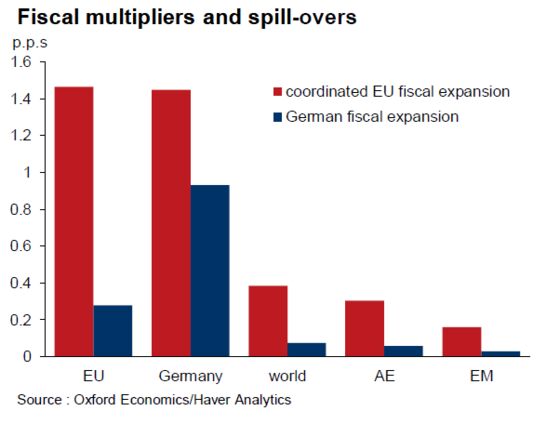

According to Oxford Economics, the interconnectedness of EU economies means the spillover effect is quite large, while the domestic benefit is lower than elsewhere. A coordinated approach would be best -- “it almost doesn’t pay to engage in a fiscal expansion within the EU without cooperation,” economist Tamara Basic Vasiljev said in a report this month.

German officials are less convinced. Bundesbank chief Jens Weidmann argued last year that because public expenditure wouldn’t affect imports much, spillovers “are likely to be small.”

That chimes with an economy ministry analysis from 2015, which found that Berlin increasing public investment would boost euro-area output only “slightly” and without any lasting effect on growth.

One issue likely to affect the outcome of any study is whether there could be counter-effects to a fiscal boost, such as a strengthening of the euro or higher interest rates.

German stimulus might also help countries which don’t really need it. Ansgar Belke, professor at the University of Duisburg-Essen, reckons more affluent Finland, Ireland and the Netherlands could be beneficiaries, while effects on Greece, Spain and Portugal might be “rather low.”

Belke adds that at the current juncture, the trade war poses a challenge to the transmission of a stimulus. His research shows that “fiscal policies are not as effective in uncertain times as in tranquil times.” Others have also noted that government spending shocks had larger impact in booms than in recessions.

On that last point, IMF officials seem to disagree. The wider impact of fiscal stimulus “intensifies when a source or recipient country is in recession and/or benefiting from accommodative monetary policy,” according to its 2017 World Economic Outlook.

Crucial to any analysis is what form German stimulus would take. With a railway network plagued by delays and patchy wireless connectivity, projects focused on transport and 5G networks could generate “quite advantageous” multipliers elsewhere, according to Marc Bruetsch, chief economist at Swiss Life.

What Bloomberg’s Economists Say

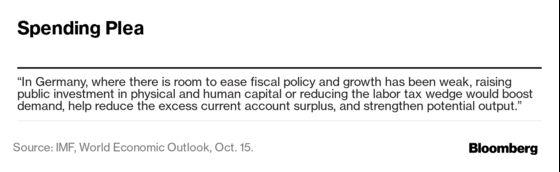

Berlin could probably justify easing fiscal policy by as much as 2.2% of GDP in 2020. That would free up space for spending or tax cuts of as much as 80 billion euros -- a bigger dose of stimulus than unleashed during the financial crisis. But it won’t happen.

-- Jamie Rush, chief European economist

See BECO for more from Bloomberg Economics

Whatever its wider effects, a fiscal stimulus for Germany is clearly a relatively inefficient way of aiding the euro region as a whole. But while French President Emmanuel Macron has pushed a euro-zone budget to make countries pool resources, there remains strong opposition in richer members towards sharing their tax money.

“Germany saying they would ease fiscal policy because they’re in a deep recession is not the same as Germany saying we should ease fiscal policy because we’re benefiting from being in the euro and we should help everyone else,” Trevor Greetham, head of multi asset management at Royal London Asset Management, told Bloomberg Television. “But Macron has got a euro-zone budget started, and that’s something to keep watching.”

In the meantime, all Draghi and Lagarde can do is keep calling on governments to step up, which is probably what will happen on Thursday.

“We would expect him to lean into the fiscal policy rhetoric,” Andrew Wilson, co-head of global fixed income at Goldman Sachs Asset Management, said on Bloomberg TV. “We all know that monetary policy is really reaching the end of its limits.”

--With assistance from Birgit Jennen and Zoe Schneeweiss.

To contact the reporters on this story: Catherine Bosley in Zurich at cbosley1@bloomberg.net;Yuko Takeo in Tokyo at ytakeo2@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, ;Paul Gordon at pgordon6@bloomberg.net, Craig Stirling

©2019 Bloomberg L.P.