Draghi Stimulus Comes With More Punch as ECB Claims Room to Act

Draghi Stimulus Comes With More Punch as ECB Claims Room to Act

(Bloomberg) -- Mario Draghi is set on pushing the limits of the European Central Bank’s firepower right up until he leaves office.

With little more than four months to go in his job, the ECB president has all but pledged new stimulus for Europe’s flagging economy that may include both interest-rate cuts and asset purchases. Adding potency to that statement is his declaration that the institution shouldn’t be hemmed in by its rules restricting the room for maneuver.

In response, European bonds enjoyed one of their biggest rallies in recent memory as yields tumbled to record lows across the region. German 10-year rates are now hovering just above the ECB’s minus 0.4% deposit rate, while those on French securities dropped below zero for the first time. Traders in money markets are pricing a rate cut by September.

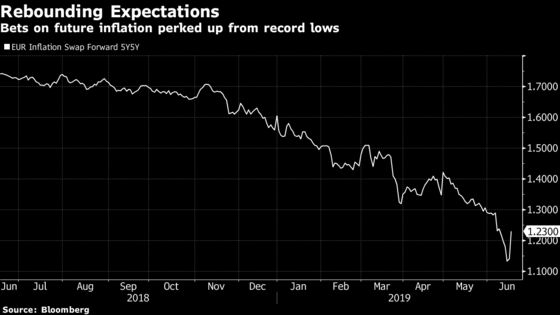

Tuesday’s threat of stimulus succeeded where the ECB failed earlier this month in placating investors. It prompted inflation expectations to rise and the euro to fall. According to the institution’s former chief economist, that’s because the extent of Draghi’s pledge opens the door to far more powerful policy action than officials had previously signaled was even possible.

“What is very important is the optionality -- to make the options more credible,” Peter Praet, who left the ECB at the start of this month, told Bloomberg Television. “I am not sure that markets say you need to act now, but the markets want to be reassured that if the environment doesn’t improve, do you have the necessary tools to do that.”

Summer Stimulus

Three central bank officials, speaking on condition of anonymity, told Bloomberg that an interest-rate cut is most likely the first response to any slowdown. Commerzbank AG economists see such a move as soon as the next meeting in July, while JPMorgan Chase & Co. anticipates a change in the policy language first, to set up a cut at the following gathering in September.

“The market was really being fairly lazy on pricing in ECB risks because of some sense they were hesitant to use their tools,” said Richard Kelly, head of global strategy at Toronto-Dominion Bank in London. “Draghi had to be even more blunt that they will act if they feel it is needed.”

That message led Austria and Sweden bonds to join Germany in the club of nations where investors have to pay to hold their sovereign debt. In Italy, investors brushed off comments from Deputy Prime Minister Matteo Salvini that the government would back so-called mini-bills, seen by many as a step toward a parallel currency to the euro, scooping up its bonds on the prospect of fresh quantitative easing. Yields fell the most in a year.

The ECB president’s remarks also incited a response from U.S. President Donald Trump, who said the drop in the euro prompted by Draghi’s remarks is unfair.

Draghi responded to that by telling the ECB’s annual retreat in Portugal that “we don’t target the exchange rate -- keep this in mind.”

His remarks bring the institution closer to the global easing shift that some economists and investors also expect the Federal Reserve to join this year. U.S. policy makers are seen unlikely to act as soon as their meeting this week.

The problem for Draghi is that he has already used up much of the institution’s ammunition. The deposit rate was cut to an unprecedented low of minus 0.4% in 2016. Its stimulus program hoovered so many government bonds that it was getting close to the buffers.

The Governing Council capped the amount of sovereign debt the ECB can acquire under QE to ensure it would avoid violating European Union laws prohibiting it from financing governments. It can’t hold more than 33% of a country’s total debt. There’s also a limit on individual issues of as much as 33% if certain conditions are met.

While Draghi claims the ECB has developed “headroom” to buy more, the cap still represents a straitjacket that risked undermining credibility. So on Tuesday, he sought to correct that impression by stating that those limits might not need to apply.

“The Treaty requires that our actions are both necessary and proportionate to fulfill our mandate and achieve our objective, which implies that the limits we establish on our tools are specific to the contingencies we face. If the crisis has shown anything, it is that we will use all the flexibility within our mandate to fulfill our mandate.”

That’s reminiscent of Draghi’s insistence in 2012 that the institution would do “whatever it takes” to save the euro, necessitating the creation of a crisis tool that pushed the boundaries of its competencies.

“If they take up QE again, they will have to change various characteristics,” said Nadia Gharbi, an economist at Pictet in Geneva. “What Draghi wants to show is that they are ready to do everything to boost inflation and that the constraints, including on the issuer limits, can be moved.”

What Bloomberg’s Economists Say

“Draghi also seemed to be emphasizing a need to take action soon...His term ends in October, but he still has a few months to preside over one last big change before he leaves.”

--David Powell and Maeva Cousin. See their ECB REACT

For now, the ECB president has succeeded in convincing investors that, even in the dying days of his time in office, nothing will stop his determination to leave a legacy of sustainable inflation. But he of all people knows that such a perception can quickly unravel.

“Draghi has managed to revive inflation expectations -- but only as long as he actually delivers,” said Arne Lohmann Rasmussen, head of fixed-income research at Danske Bank A/S in Copenhagen.

--With assistance from Catherine Bosley, Jana Randow and Piotr Skolimowski.

To contact the reporters on this story: Craig Stirling in Frankfurt at cstirling1@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Neil Chatterjee, Fergal O'Brien

©2019 Bloomberg L.P.