Draghi’s Stimulus Shot Is No Cure for Europe’s Japanification

Draghi’s eight-year term has been defined by radical measures such as negative rates, long-term funding and quantitative easing.

(Bloomberg) -- The monetary stimulus that European Central Bank President Mario Draghi unleashed last week won’t be enough on its own to prevent an extended period of low economic growth and feeble inflation.

That’s the view of analysts in Japan, a nation with long experience of entrenched weakness where the central bank has also dived into a combination of negative interest rates and quantitative easing. They see parallels in the euro area as long as it’s blighted by fundamental challenges such as low productivity growth that lie outside the realm of monetary policy.

“It’s something Japan’s been struggling with over the past two, three decades,” said Harumi Taguchi, Tokyo-based principal economist at IHS Markit. “Europe also faces a range of structural problems. The ECB’s actions will be effective in the short term and it’s important to buy time, but what’s more important is how you deal with the underlying structural problems.”

Draghi’s eight-year term, which ends in October, has been defined by radical measures such as negative rates, long-term funding and quantitative easing. The Bank of Japan started QE in 2001 and has pushed the boundaries further since Haruhiko Kuroda became governor in 2013, buying exchange-traded funds and directly controlling the 10-year yield. Here’s a look at how they’ve both done.

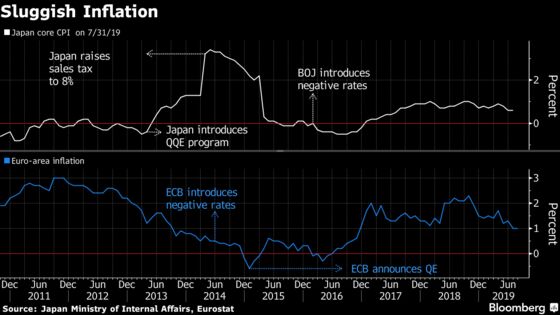

Lowflation

Draghi started negative rates in 2014 and QE in 2015, and the BOJ cut rates below zero in 2016. They both averted deflation -- a downward spiral of prices and wages that can lead to an economic depression -- but inflation has struggled to gain much momentum since, despite ever-loose policy.

Exchange Rate

One reason might be that persistent easing doesn’t necessarily mean a weaker currency -- an important conduit for reflating the economy. The euro dropped against the dollar after the deposit rate was cut below zero, and continued to fall as investors bet on a QE program, but it bottomed out as soon as bond purchases were announced in January 2015.

When Japanese rates turned negative, the yen fell only briefly before picking up again. One view is that subzero rates, by squeezing lenders’ profitability, caused a drop in bank stocks and a broader equity selloff. That pushed investors into buying the yen as a haven. Banks also brought overseas investments back home into yen-denominated assets.

Low Growth

The euro area exited a double-dip recession in 2013 and has grown ever since, something the ECB claims partial credit for, but even the bumper year of 2017 only saw GDP rise 2.5%. The central bank’s growth forecast for this year is just 1.2% and may be cut again on Thursday, and manufacturing is in recession.

Japanese growth has averaged only 1.2% since 2013, and that’s despite the nation’s ability to broadly coordinate fiscal and monetary policy -- a much harder task in Europe.

“Lowering rates further when it’s already near its limit doesn’t mean the economy will start revving up,” said Yuichi Kodama, chief economist at Meiji Yasuda Life Insurance Co. in Tokyo. “In that sense, the European situation is similar to Japan’s.”

A key concern is productivity, the economic value each person produces. Most developed nations have suffered weaker productivity growth for years though -- and that’s a trend economists have struggled to explain.

Getting On

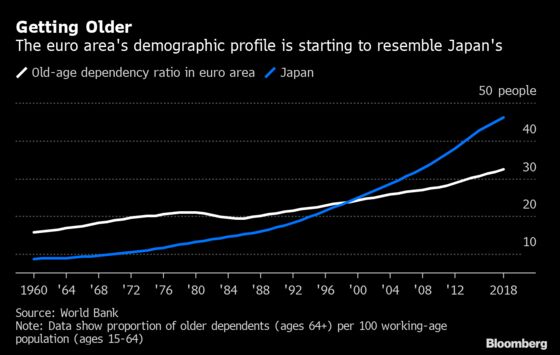

Europe and Japan share a demographic problem -- their populations are aging as birth rates plunge. That puts more of a burden on workers and can depress inflation as people save for retirement instead of spending. Ultra-low interest rates may exacerbate that as people fret over their retirement income.

Unlike Japan though, Europe has had an influx of migrants that helps to mitigate the problem. Bloomberg Economics’ Yuki Masujima says euro-zone diversity is higher than in Japan and that’s a reason to be wary of oversimplifying the comparison between the two economies.

“Still, they do face issues that are shared by advanced economies, including the aging population,” he said.

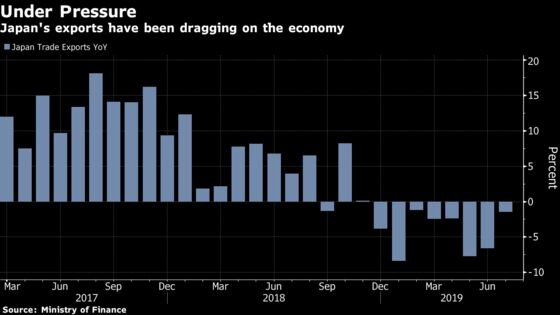

Export reliance

Where Japan and Europe are especially exposed is their relatively high reliance on exports. When global demand cools -- as currently because of U.S. President Donald Trump’s protectionism -- manufacturers suffer and the domestic economy is hit.

“There are a lot of fundamentals in Europe that are similar to Japan,” said Kenichiro Yoshida, senior economist at Mizuho Research Institute. “In countries like Germany but also in Europe in general there’s a tendency for growth rates to fall when trade volumes decline. In a word, they have a high rate of export dependency.”

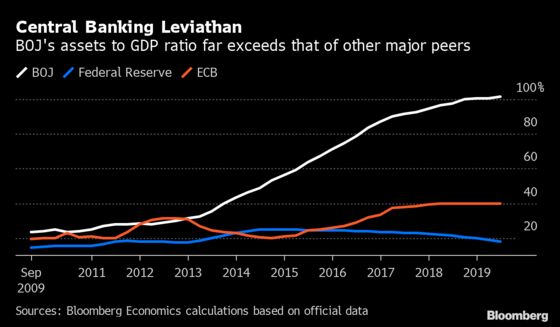

Piling Assets

As long as the ECB and BOJ plow on with monetary stimulus, their balance sheets will increase. The BOJ’s assets have ballooned to a value greater than the country’s GDP. While it’s debatable whether that should be a concern or not, what is apparent is that there’s no good correlation with inflation. The ECB could be headed the same way.

--With assistance from Yuki Masujima (Economist).

To contact the reporter on this story: Yuko Takeo in Tokyo at ytakeo2@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Jana Randow

©2019 Bloomberg L.P.