Draghi’s Legacy in Credit Is a Bigger, Cheaper, Quirkier Market

Europe’s corporate bond market has been transformed since departing ECB President Mario Draghi took office at the end of 2011.

(Bloomberg) -- Europe’s corporate bond market has been transformed since departing European Central Bank President Mario Draghi took office at the end of 2011. Here are four charts showing how 178 billion euros ($199 billion) of corporate QE and numerous attempts of easing euro-area financing conditions has reshaped the behavior of both corporate borrowers and bond investors.

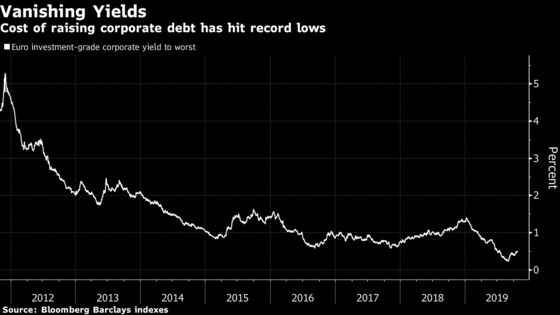

The size of the euro investment-grade corporate bond market has ballooned to a record 2.4 trillion euros ($2.7 trillion) since Draghi took the helm at the ECB. This growth, turbo-charged by cheap QE era funding costs, is triggering a fundamental change in how companies in Europe borrow money: Corporate bond issuance “reflects, at least initially, a shift by some firms from loans to market-based debt funding,” the ECB said in its 2018 annual report.

All this has been made possible by record-low borrowing costs spurred by the ECB’s negative interest rate policy and bond purchases. Firms rated triple-B, one to three steps above junk, have turned to Europe’s bond market for funding in their droves and this rating group now accounts for half of the entire euro high grade market.

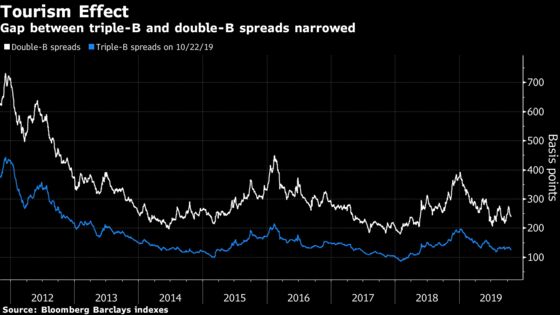

Depressed high grade yields -- another consequence of ECB monetary policy -- has led to so-called credit market tourism: portfolio managers buying bonds that are usually beyond their remit in a bid to boost returns. The stronger names in the junk bond market have been prime targets and as investors flocked to them, their spread pick-up over their high-grade peers declined.

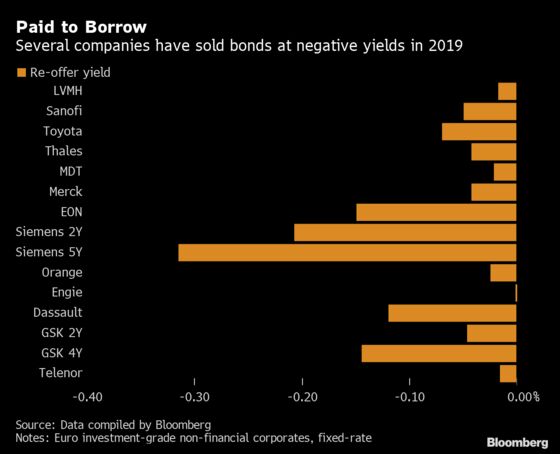

The ECB’s easing policy has also led to distortions, the most recognizable of which is the phenomenon of companies effectively getting paid to borrow money in the bond market. What started with a couple of short-dated issues by Henkel AG & Co KGaA and Sanofi SA a few months after the start of corporate bond purchases had spread to numerous bond offerings by 2019.

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editor responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net

©2019 Bloomberg L.P.