Draghi’s Final Stimulus Push Keeps Bond Investors in Suspense

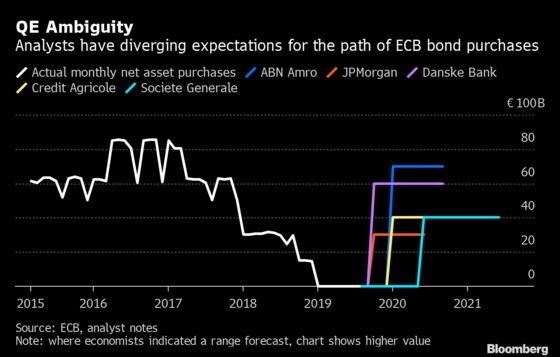

Expectations for quantitative easing in the euro area, however, diverge wildly.

(Bloomberg) --

Mario Draghi’s plans for a parting stimulus shot before he retires as European Central Bank president are laced with even more suspense than usual.

While the ECB is widely expected to cut interest rates next month, the prospect of a renewed round of asset purchases is shrouded in uncertainty. Investors must judge how much quantitative easing the euro-zone economy needs, how much buying space the central bank has before it hits self-imposed limits -- and whether policy makers will dare test Draghi’s claim that he can bust through those restrictions if needed.

That ambiguity means markets are in the dark about one of the key monetary tools available to support the 19-nation economy as it battles a slowdown wrought largely by external factors such as trade tensions and Brexit. Much depends on whether Draghi wants to go out with a bang before Christine Lagarde takes over on Nov. 1.

Most analysts predict the ECB will lower its deposit rate by 10 basis points to minus 0.5% at its Sept. 12 meeting, joining the current wave of global easing. In the past several weeks alone, the U.S. Federal Reserve and its peers in major economies including Russia, Australia, South Korea, Brazil, India, Indonesia and South Africa have cut rates.

Wide Range

Expectations for QE in the euro area, however, diverge wildly. The market is currently pricing in around 100 billion euros ($112 billion) to 200 billion euros of fresh stimulus, according to Alessandro Tentori, chief investment officer at Axa Investment Managers.

ABN Amro expects purchases of 70 billion euros a month over nine months. Morgan Stanley predicts QE at either 45 billion euros or 60 billion euros a month for at least a year. Goldman Sachs estimates that the ECB will spend a total of as much as 300 billion euros.

Some analysts see bond-buying announced alongside a rate cut, while others believe there will be a delay. UBS says it doesn’t consider fresh purchases a done deal.

What Bloomberg’s Economists Say

“We expect the ECB to cut the deposit rate by 10 basis points and relaunch its asset purchase program in September.

--Maeva Cousin. Read the complete ECB INSIGHT

One factor is the ECB’s attempt to keep on the right side of European Union law that forbids it from directly financing governments. By restricting itself to holding no more than 33% of any nation’s sovereign bonds, the institution aims to avoid becoming a dominant creditor.

The problem is that it’s already at or close to that limit in some countries -- including Germany, the bloc’s biggest economy. In June, Draghi said there’s still “considerable headroom” and that a weaker economy could warrant breaching the limits, though he’s done little to clarify that view since.

Legal Jeopardy

BayernLB reckons a pending ruling by Germany’s constitutional court on a challenge to the legality of the program could delay action.

“I don’t believe that a new QE program is just around the corner,” said Stefan Kipar, the bank’s euro-area economist. “You have to imagine the communications disaster if they say they are doing a new round of QE, and two weeks later the Federal Constitutional Court says the Bundesbank can’t participate.”

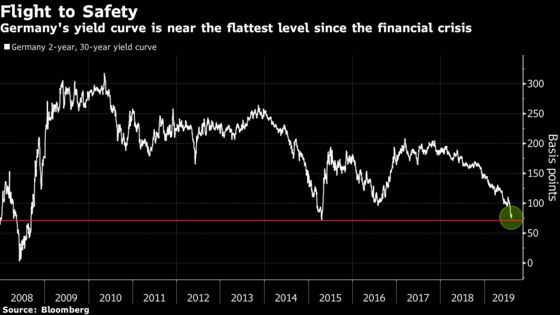

QE might not even be the most useful tool for the current environment. The chief benefit of buying bonds is that it can depress longer-term borrowing costs, but investor demand for safer assets is already pushing down yields. The gap between rates on Germany’s two-year and 30-year bonds is near the narrowest since the financial crisis.

“They’ll change the rules if they need to,” said Oliver Rakau, an economist at Oxford Economics, who predicts monthly purchases of 20 billion euros to be announced in September. “The question is how big of a package do you even need, and do you really need to have 60 billion that we had at times when we were still worrying about deflation? From that perspective, I think QE will be smaller, and that should also give the ECB more time to reach the boundaries.”

For Axa’s Tentori, a small program would only be equivalent to a “negligible” cut in the deposit rate. Still, that doesn’t mean the ECB won’t act. For all the uncertainty surrounding Draghi’s intentions, investors are primed for at least some kind of action.

“The markets now expect something, independent of the economic purpose,” Tentori said.

To contact the reporters on this story: Carolynn Look in Frankfurt at clook4@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Jana Randow

©2019 Bloomberg L.P.