Treasuries May Be Open to Tactical Plays as Rally Loses Momentum

Treasuries May Be Open to Tactical Plays as Rally Loses Momentum

(Bloomberg) -- Price action and momentum drive flows in bonds, but from a tactical perspective it’s no longer compelling to chase the rally in 10-year Treasuries. The aggressive fall in yields should stabilize with confirmation needed from fundamentals, helped potentially by less convexity hedging flow.

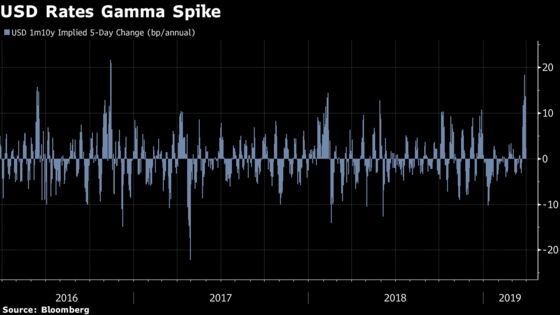

Harvesting value from short rates volatility on the 1m10y point has been an attractive yield enhancement strategy in recent years, with the lack of realized volatility of rates earlier this year having boosted short gamma positions. Ten-year yields declined as much as 26bps since before the March FOMC meeting, with receiving flows related to delta hedging short-gamma positions having helped compound the decline in rates (in addition to other negatively convex players, such as MBS investors).

Any further fall in yields may not lead to an increased need to hedge these positions given it would reduce the negative gamma profile as the market moves further from the strike, reducing the appeal of chasing duration.

- The 1m10y implied vol at the start of March was implying a terminal move of ~10bps, with the ~40bps rally in 10y yields triggering large hedging flows

- The spike in gamma will likely be temporary as yields stabilize and remain range-bound, with tactical systematic short-volatility strategies taking advantage of the moves; China PMI, South Korea exports, U.S. ISM, NFP and German factory order data will set the tone for 2Q and whether a growth bounce is underway

- Any moderate sell-off within a new lower range caused by green shoots in the global economy may bode well for payer ladders structures; YTD highs are unlikely to be taken out any time soon given the global low rates environment

- Curve vol straddles may be preferable over outright long vol exposure for those inclined to protect against recession risks

- The increase in delivered curve vol comes from the rates curve moving from bull flattening on risk-off to bull steepening on Fed cuts

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Scott Hamilton

©2019 Bloomberg L.P.