Don’t Call It Stagflation, But China Assets Flash Economic Worry

China slowdown bites harder for investors on inflation jump.

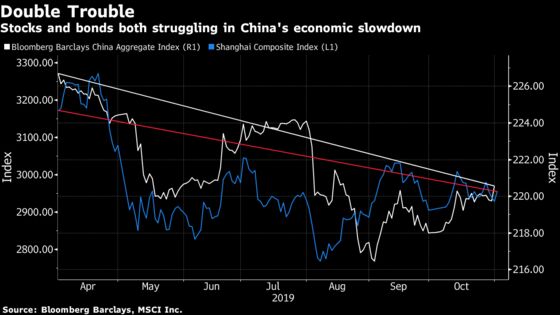

(Bloomberg) -- A rare, simultaneous bout of weakness is hitting Chinese bonds and stocks, exposing growing unease about the dual brunt of slowing output growth and rising prices in the world’s second-largest economy.

Up until recently, stock investors could take a measure of solace from weakening economic growth, confident that policy makers would respond with expanded stimulus measures -- even if they weren’t the same scale as in years past. But now, a jump in inflation is cementing the view that the People’s Bank of China isn’t likely to roll out large-scale stimulus soon.

It’s not the same magnitude of stagflation that walloped stocks and bonds alike in the U.S. in the 1970s and early 1980s. But the nervous undercurrents in Chinese markets are drawing attention to Beijing’s policy dilemma, one that is complicated by the trade tensions and elevated debt levels.

“A weak economy is well expected, but the problem is that inflation has reduced space for the central bank to ease policy,” said Amy Lin, a Shanghai-based analyst at Capital Securities.

There were some signs of a respite on Friday, with the Shanghai Composite Index up 0.9% as of 2:06 p.m. local time, following an unexpected gain in a manufacturing gauge that cut against the run of recent data. Yet it’s still down about 4% since the end of April, while the MSCI World Index of developed stocks is up 2.6% in that time. And it’s 10% off of its high for the year.

On the bond side, Chinese government securities have under-performed their peers this year, more than doubling the 10-year yield premium over Treasuries to about 157 basis points.

Ten-year bonds are heading for fourth straight week of declines. The latest disappointment: the People’s Bank of China’s decision to drain a net 590 billion yuan ($84 billion) from the financial system this week by allowing money market loans previously issued to financial institutions to mature.

The PBOC has also held off on using a one-year targeted lending tool, which was widely expected among central bank watchers since last week. Even before recent price rises, the central bank was wary of cutting actual lending rates out of concern for high debt levels and the stability of the financial system. Higher inflation now on balance makes it even less likely that dramatic easing is on the cards.

Consumer prices rose 3% in September from a year earlier, propelled by a 69% surge in pork prices thanks to the outbreak of swine fever that’s ravaged hog production in the world’s biggest consumer of the meat. Deutsche Bank AG doesn’t rule out a further climb to 4% inflation.

“Pork is not a small deal -- there are already signs of some fine-tuning of monetary policy,” said Qu Qing, Beijing-based chief economist at Jianghai Securities, who thinks inflation could even surpass 4.5% in January. It’s a new element for policy makers up to now focused on holding down real-estate prices, according to Qu.

And what’s next for markets?

“It all depends on what the central bank does next,” Qu said.

©2019 Bloomberg L.P.