Fed Wipes Out Dollar Premium in One Fell Swoop: Liquidity Watch

Fed Wipes Out Dollar Premium in One Fell Swoop: Liquidity Watch

(Bloomberg) -- It’s never been cheaper to access dollars outside of the U.S., thanks to the Federal Reserve’s beefed-up swap lines.

Three-month dollar-yen cross-currency basis, a key indicator of funding stress for global investors, turned positive on Tuesday and rose to an all-time high on Wednesday. That means yen funding is at its most expensive versus the U.S. variety, similar to those in Europe and the U.K. It was at a record discount just two weeks ago.

It’s all down to the Fed. With a net $360 billion of outstanding swap lines extended to central banks in Japan, Europe and the U.K. as of Tuesday, foreign lenders are awash with dollars even as more are becoming available. Case in point: A seven-day Bank of Japan allotment on Wednesday saw a take-up of just $950 million compared with almost $5 billion maturing.

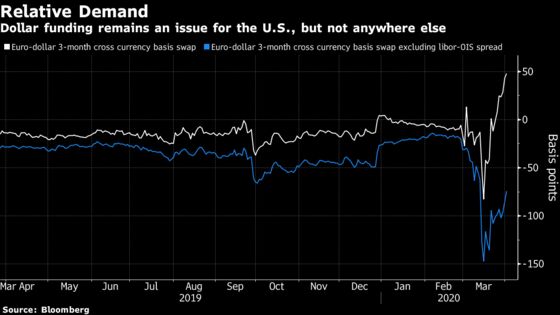

While the dollar is getting cheaper globally, costs are still high at home. U.S. money-market spreads are languishing near post-crisis wides, a reason why investors may be turning to cross-currency basis swaps. The spread between the London interbank offered rate and overnight index swaps -- a proxy for the risk-free rate -- is near its widest level since the 2008-2009 financial crisis.

“The elevated level of Libor (v OIS), compared to other funding rates which are showing signs of easing, may be incentivizing investors to lend dollars through cross-currency to take advantage of elevated yields,” wrote Morgan Stanley strategist Zuri Zhao in a note. “This leads to a further narrowing in the cross-currency - particularly now that quarter-end settlement has passed.”

| Read More: |

|---|

|

Here’s a look at some key funding metrics:

Cross-Currency Basis

Three-month cross-currency basis for yen saw a dramatic tightening on Tuesday and soared above 10 basis points the following day. The euro variety was about 50.

The recent turbulence in U.S. dollar funding markets was in part the result of a decrease in bank hedging services because of rising volatility, according to a paper by the Bank for International Settlements published Wednesday.

The resulting pullback in the supply of dollars from banks and money markets during a period of high demand resulted in dramatic increases in funding costs.

Libor and Commercial Paper Spreads

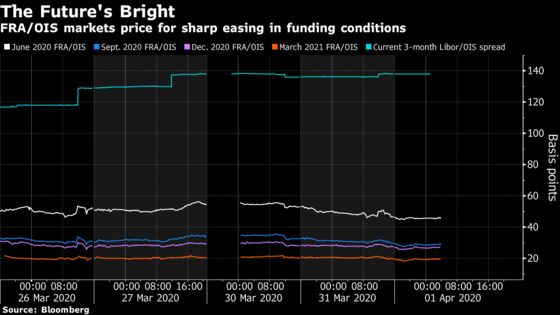

Three-month dollar Libor fell 1.4 basis points on Wednesday, staying within this week’s tight range. The yield on short-term commercial paper issued by top-tier non-financial companies fell to 1.51% as of March 31, according to Fed data published Wednesday.

Yet any commercial paper that issuers are selling are still concentrated among the shorter tenors, an indication the market is still relatively frozen. This is why the debut of the central bank’s Commercial Paper Funding Facility -- due to start in the first half of April -- will be important to watch.

“The rollout of the CPFF facility will be a crucial reality check for the market,” Credit Suisse strategist Jonathan Cohn wrote in a note to clients. “If it does serve to cap 3m CP-OIS rates around 110bp, then the rapid normalization – much of which is priced in the market – should be realized assuming a reasonable beta between Libor and CP.”

Futures markets are already pricing in such a move. FRA/OIS contracts -- the spread between Eurodollar futures that are priced off Libor and overnight swap rates -- show a steady tightening through year-end.

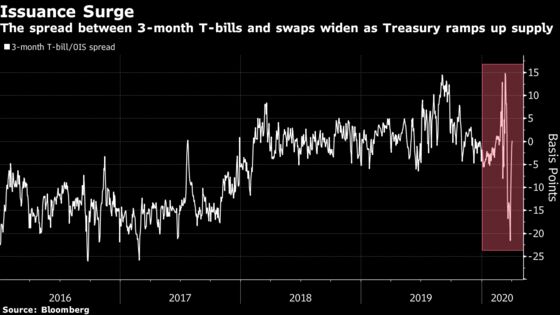

T-Bill/OIS spreads

A closely watched gauge of short-term lending has been widening and is expected to continue as the U.S. continues to flood the market with Treasury bills. The Treasury is currently set to increase the total amount of short-term securities on issue by around $288 billion by April 7, data from the department show.

The spread between yields on three-month Treasury bills and overnight index swaps, which measures the health of a key part of the U.S. government debt market, has returned to near zero. It touched minus 22 basis points on March 26, which was the most inverted since February 2017.

While appetite for T-bills has been robust as cash has flooded into government money-market funds, that demand should moderate as flight-to-quality pressures fade.

“The panicked dash for cash which characterized March at moments will likely moderate,” BMO Capital Markets strategist Jon Hill wrote in a note to clients. “If this occurs, it would translate into not only a slowing/reversal of the AUM increase in government funds, but also an extension” of their weighted average maturities.

©2020 Bloomberg L.P.