Dollar Is Trading at a Discount for First Time Since March Chaos

Dollar Is Trading at a Discount for First Time Since March Chaos

(Bloomberg) -- The dollar is looking unloved with the curtain having come down on one of the most intense episodes of currency-market stress. But don’t bank on a major slump.

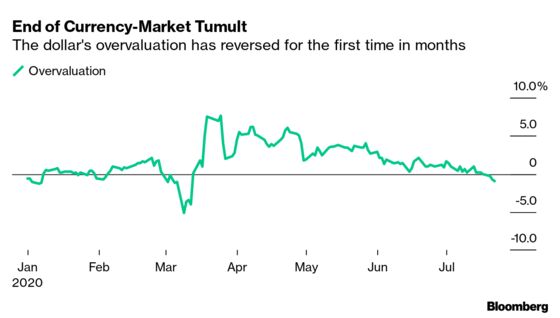

The dollar is now trading at a discount to fair value for the first time since the tumult that gripped the G-10 complex back in March. The U.S. Dollar Index (DXY), which traded at a hefty premium of as much as 8% at one point, has an offered tone now. Indeed, at 94.986, the index is trading at a discount of 1.4% against the fitted curve in a multivariate setting.

Back in the first quarter as the markets went into meltdown, risk-on currencies slumped, some by more than 10%. The tumult caused the Ted and FRA/OIS spreads, measures of stress in money and credit markets, to blow out and led to a widening of cross-currency basis swaps as investors sought refuge in the dollar. The Fed then unveiled a volley of measures that have largely healed ructions in the market.

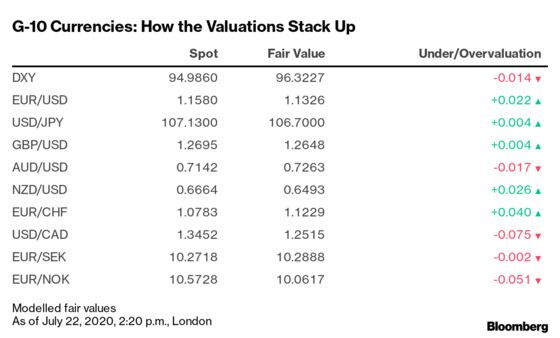

The current unwinding of the premium for the dollar is working as a salve for the familiar risk currencies such as the euro and the Australian and New Zealand dollars. The table below shows the current fair values:

The model forecasts a currency’s value based on multiple factors including interest-rate differentials, leading economic indicators such as PMIs, flow indicators and exogenous variables such as crude prices and China’s exchange rate.

Does all the above mean that the dollar will continue weakening? Any discussion of the dollar can’t ignore the euro given the high weighting of the latter in the DXY. As the table above shows, the euro is trading at a premium of 2.2% over fair value, stemming from the currency’s reversed correlation with bunds, yields on which have fallen. Given all the weakness in the euro-area economy, it’s unlikely that the European Central Bank will want higher yields or undue euro strength for fear of choking off any signs of inflation, which was already feeble before the pandemic struck.

It is also inconceivable that the Bank of Japan would want the yen -- which is almost fully valued -- to shoot any higher. And with the explicit target of the 10-year point of the JGB curve, Governor Haruhiko Kuroda has greater currency control than perhaps many of his peers.

While periods of under- and overvaluations are common, all the above rein in prospects for a huge correction in the dollar. In addition, the assumption that the U.S. economy isn’t yet out of the woods is borne out in the rates complex, thanks to the market’s self-imposed curve control.

As long as that skepticism prevails and fundamental factors don’t augur in favor of risk currencies, demand for the dollar can’t simply disappear into thin air.

NOTE: Ven Ram is a currency and rates strategist for Bloomberg’s Markets Live. The observations are his own and not intended as investment advice

©2020 Bloomberg L.P.