A Divided Fed May Be Reluctant to Forecast More Cuts

A small cut won’t be applauded by Trump, who last week said the Fed’s “boneheads’’ should reduce rates to zero or lower.

(Bloomberg) --

Under pressure from Wall Street and President Donald Trump, the Federal Reserve is widely expected to reduce interest rates on Wednesday for a second straight meeting, but its sharply divided policy panel may be reluctant to forecast further cuts.

The Federal Open Market Committee is likely to lower rates a quarter percentage point to insure against risks from a global slowdown and uncertainty over Trump’s trade policies, while forecasting no more reductions this year, according to economists surveyed by Bloomberg.

The meeting comes as the Fed’s New York branch injected billions of dollars in cash into money markets this week, to quell a surge in short-term rates that was pushing up its benchmark rate. The spike pushed the rate above their preferred range.

The policy statement and updated quarterly forecasts will be released at 2 p.m. in Washington and Chairman Jerome Powell will brief the press 30 minutes later.

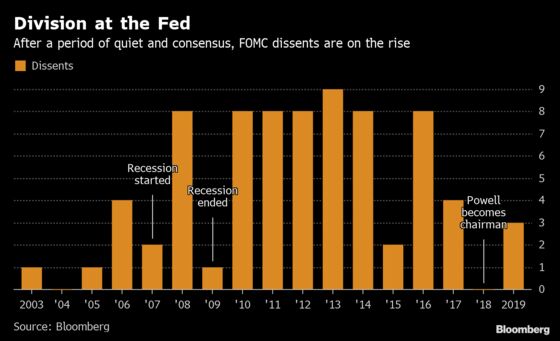

“It is a very divided group,’’ said Carl Tannenbaum, chief economist with Northern Trust Corp. in Chicago. “If participants are not seeing a deterioration in growth, how far are they willing to push? It is not a sure thing they will do more.’’

The median interest-rate projections in the “dot plot’’ -- which displays the forecasts of the 17 Fed policy makers -- is likely to be unchanged for December after Wednesday’s expected cut, according to the Bloomberg survey. By contrast, investors are projecting another quarter point reduction by the end of this year.

Kansas City Fed President Esther George and Boston’s Eric Rosengren are likely to dissent, as they did against the rate cut in July, favoring no move. Another possible dissenter is St. Louis Fed President James Bullard, who may favor a half-point cut in the face of rising uncertainties.

What Bloomberg Economists Say

“Bloomberg Economics expects policy makers to cut rates in steady 25 basis-point increments until the yield curve is no longer inverted. We believe this means rate cuts in September, October and December -- although officials may hesitate to fully telegraph such intentions.”

-- Carl Riccadonna, Yelena Shulyatyeva, Andrew Husby and Eliza Winger

Click here for more.

That said, most economists surveyed by Bloomberg expect the FOMC statement to stick with language that signals a bias to continued easing, probably via references to uncertainty over the outlook and a commitment to “act as appropriate” to sustain the expansion.

“There are two fundamentally different views of the economy,’’ said Lindsey Piegza, chief economist at Stifel Nicolaus & Co. Inc. in Chicago. That will be reflected by a “growing in the dispersion of the dots and increasingly muddying the policy message for investors.’’

A small cut won’t be applauded by Trump, who last week said the Fed’s “boneheads’’ should reduce rates to zero or lower.

Read more: Key Trump Quotes on Powell as Fed Remains in the Firing Line

Volatility in oil prices after attacks on key Saudi Arabian facilities over the weekend reinforces the growing risks in the global economy, though the FOMC may be reluctant to adjust views to fast-changing events.

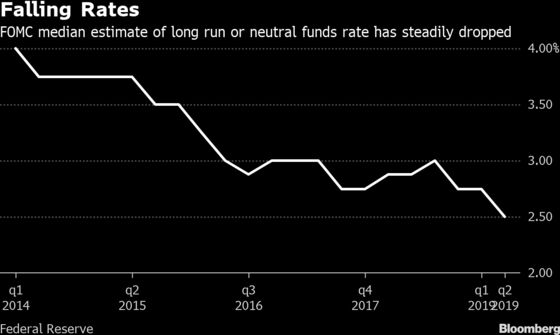

The committee could ratify the view that rates will be lower for longer by edging its estimate of the so-called neutral rate which neither spurs nor brakes the economy. It has fallen to 2.5% from 4% in early 2014 amid a global decline in borrowing costs that’s seen them slip into negative territory in Europe and Japan.

Statement Language

FOMC divisions make drafting the statement a challenge. Recent data have supported its forecasts for more than 2% economic growth this year, and some reports have surprised to the upside. Yet U.S. payroll growth has slowed and manufactured contracted in August for the first time in three years.

“They have been using boilerplate language ‘solid’ in describing the labor market, but that’s becoming harder to support and could be downgraded,” said Neil Dutta, head of U.S. economics at Renaissance Macro Research. Market measures of inflation expectations could also be downgraded, he said.

Powell, who in July referred to the rate cut as a “mid-cycle adjustment’’ rather than a long string of cuts, is likely to be asked about Trump’s call for zero rates and ex-New York Fed President Bill Dudley’s recent controversial column suggesting his former colleagues don’t cut rates to avoid enabling the trade war.

IOER, Balance-Sheet Tweaks

The Fed may announce a couple of technical adjustments to its balance sheet and the interest it pays banks on reserves after a sharp rise in money-market rates led the New York Fed to take action on Tuesday via its first overnight injection of cash in a decade.

It could make another adjustment to the interest rate it pays on excess reserves by reducing it by more than amount it cuts the fund rate. IOER is currently at 2.1% and the Fed may lower that by a bit more than the amount it cuts the target range for its benchmark federal funds rate -- currently 2% to 2.25% -- to better anchor money market rates.

Separately, following the Fed’s decision in July to call an early halt to the gradual shrinking of its balance sheet, it may also say it is going to start allowing it to grow again to keep pace with growth in the economy, said Jonathan Wright, a professor at Johns Hopkins University and former Fed economist. The Fed has previously discussed this in terms of a process that could begin further down the road.

A third option to reduce pressure in money markets could be a new tool called a standing overnight repo facility. Such an instrument has been previously discussed and the FOMC was briefed on it in June, though minutes of the meeting showed that policy makers wanted more work done to figure out what it would do and how it would work.

--With assistance from Matthew Boesler.

To contact the reporter on this story: Steve Matthews in Atlanta at smatthews@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Alister Bull

©2019 Bloomberg L.P.