The Solution to India's Liquidity Crunch Is Far From Home

Tapping the diaspora to prop up INR may be costly, but using $ to lubricate the local financial system is a worthwhile motivation.

(Bloomberg Opinion) -- Those who are awash in cash lack capital. Those who have adequate capital are thirsty for liquidity.

That, in a nutshell, is the story of India’s financial crunch, and the surest way to ease it will require tapping Indians living overseas.

In the past, New Delhi has resorted to such special hard-currency deposit programs to tide over balance-of-payment difficulties. A notable instance was in 1998, after India invited U.S. sanctions by testing a nuclear weapon.

Hooking nonresidents would be expensive now because dollar interest rates have risen significantly since the taper tantrum of 2013, the last time India nudged its banks to target the diaspora. The only way to justify such fund-raising would be if the program did more than just rescue the rupee: Easing a tight liquidity situation could be a worthwhile motivation.

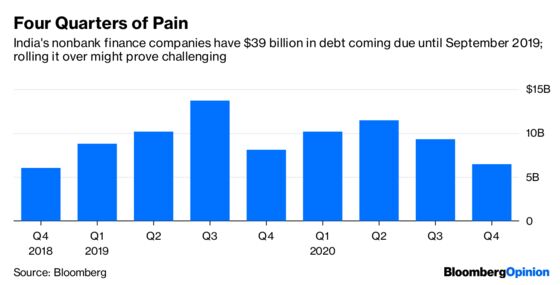

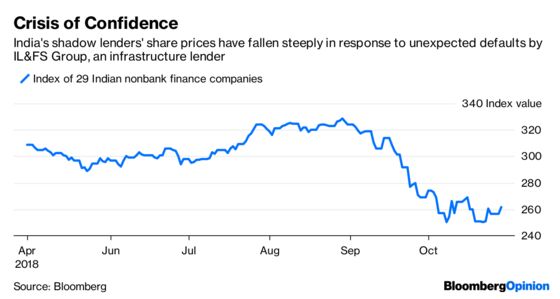

As much as $39 billion of publicly traded Indian shadow financiers’ rupee obligations, a fifth of the total, will mature between now and September, according to data compiled by Bloomberg. Rolling these over with new commercial paper, bonds and loans would be expensive; and in some cases, impossible: The nonbank lenders’ perceived credit quality has swooned over the past few months, ever since since one of them – the highly rated Infrastructure Leasing & Financial Services Ltd. group – began defaulting on debts.

If the liquidity taps don’t open soon for shadow lenders, property markets could be shaky. As Dhwani Pandya of Bloomberg News notes, citing data from JM Financial Ltd., nonbank lending to India’s real-estate firms expanded at a compound annual growth rate of 45 percent from fiscal 2014 through 2018, compared with less than 5 percent for bank advances. Should builders struggle to find a replacement for retreating shadow financiers, they may have to slash prices, and sell land holdings. If even then borrowers can’t service their debts, those defaults could further chill lending.

While loans to developers could be the first casualty, they may not be the only ones. Those against property, a popular source of funding for small businesses, could also pose a risk to finance companies if borrowers' prepayments dry up.

A typical loan against property in India has a tenure of 10 to 15 years, but gets prepaid in three to five, according to Moody’s Investors Service. That has allowed lenders to finance them by rolling over short-term borrowings without much of a glitch. Once small firms themselves start hoarding liquidity (because they can no longer get their properties refinanced cheaply), shadow lenders’ asset-liability gaps could balloon. Then their ultimate source of financing – money-market mutual funds – would evaporate.

The logical solution then is to unwind some of the market-share gains of shadow lenders in recent years. The way to do it would be to prod traditional deposit-taking banks to buy parcels of small-ticket customer loans from them outright.

State Bank of India, the country’s biggest lender, has tripled its annual target for buying loan portfolios of non-bank financial firms. SBI has a common equity Tier 1 ratio of 9.8 percent, adequate to provide for bad loans and aspire for some growth, according to India Ratings & Research Pvt., a unit of Fitch Ratings. Most of SBI’s other state-run peers have abundant deposits to deploy, but not many have the capital. A $200 billion tsunami of soured corporate loans has left them depleted.

One solution would be for the government to provide equity to any of the 21 state-controlled banks that wishes to buy shadow lenders’ loan portfolios but fears a thinning of its capital cushion. Where would New Delhi get the funds, given an already stretched budget deficit?

The money could come from nonresident Indians. There’s already talk of tapping the diaspora to prop up the rupee, Asia’s worst-performing currency this year. Typically, such dollars are raised by state-run banks as deposits. But they don’t need those now. Instead, if the foreign cash comes in as a bond investment, which qualifies as banks’ additional Tier 1 capital, and eventually gets deployed in a portfolio of shadow banks’ retail loans, it can effectively solve the twin deficiencies of liquidity and capital. And in the process, the rupee, too, gets a new leg to stand on.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.