Delinquencies Jump After Bangladesh Central-Bank Move Backfires

The initiative, which is available to borrowers until Sept. 7, created a “perverse incentive” to default.

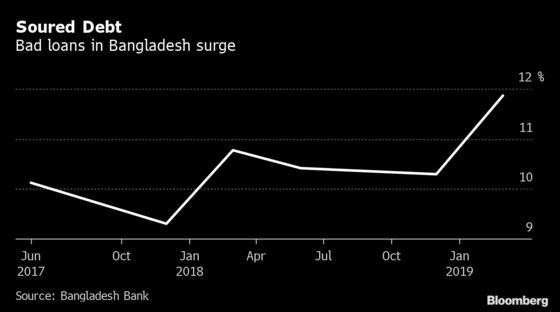

(Bloomberg) -- Bangladeshi banks are facing another jump in already-crippling levels of bad debt as a move by the central bank to ease the situation backfires.

In an effort to revive credit growth, Bangladesh Bank in May introduced an amnesty program that allowed delinquent borrowers to clean up their books by making a small upfront payment and then clearing the rest of their debt over 10 years at favorable interest rates. But it also triggered a rush by healthy companies to reschedule debt on the same terms, which now threatens to overwhelm the banks.

“I’m traumatized by non-performing loans,” said Anis A. Khan, managing director of Dhaka-based Mutual Trust Bank Ltd. Borrowers have been using every excuse they can find -- from a death in the family to political uncertainty -- to try to get onto the central bank program, Khan added in a recent interview.

The initiative, which is available to borrowers until Sept. 7, created a “perverse incentive” to default, according to researcher Fitch Solutions Inc. Non-performing loans may rise “significantly” from 11.9% in March as a result of the program, according to Yawer Sayeed, managing director of AIMS of Bangladesh Ltd., which manages 5 billion taka ($59 million) of assets.

The upfront payment under the Bangladesh Bank program was lowered to 2% from 10% for first-time defaulters. The maximum interest payment over the following 10 years was set at 9%, even if the borrowers were paying as high as 15% previously.

Read: Willful Defaults Are Bangladesh’s ‘Biggest’ Problem: StanChart

The initiative has created a sense among Bangladeshi companies that “one can get away by not paying back loans,” said Zahid Hussain, a former World Bank economist in Dhaka. That poses a threat to the wider economy and to a banking system “whose shock absorbing capacity is already sapped by willful defaults,” he said.

The central bank says the policy will help revive lending growth in an economy that’s dependent on attracting investment to sustain growth. Asian Development Bank forecasts the economy will expand 8%, the fastest pace in the region, over the next two years.

“It was necessary to take some remedial measures to bail out the defaulters,” said Shitangshu Kumar Sur Chowdhury, banking reforms adviser at Bangladesh Bank. “It’s not flawless, just like any other policy, but it has more merits than demerits.”

Chowdhury, a former deputy central bank governor, acknowledged that the new policy creates moral hazard for borrowers. “That’s why we kept it open only for a short period to minimize it,” he said.

At Mutual Trust Bank, gross bad loans climbed to more than 6% in June from 4.3% two years ago and may rise further. Managing Director Khan recalls getting a visit from a businessman from Chittagong asking for a reduction in interest rate to 5% citing losses in his steel businesses.

Read how a Sri Lankan bank is betting on Bangladesh to expand

The customer, who Khan declined to identify, paid 25% of his 2 billion taka loan. Mutual Trust is yet to rule on his request to pay 5% interest on the balance amount.

“One of our concerns in Bangladesh over the last five years has been poor transparency in the banking sector,” said Mattias Martinsson, chief investment officer at Stockholm-based Tundra Fonder AB. “The changes will obviously not stimulate further investments.”

Tundra owns shares of BRAC Bank Ltd., Bangladesh’s biggest lender by market value. The company’s bad loan ratio increased to 3.7% in June from 3.3% a year earlier.

To contact the reporter on this story: Arun Devnath in Dhaka at adevnath@bloomberg.net

To contact the editors responsible for this story: Arijit Ghosh at aghosh@bloomberg.net, Marcus Wright

©2019 Bloomberg L.P.