Debt Monetization Creeps Closer to Global Investors’ Wary Relief

From Jakarta to Wellington, policy makers are challenging taboos and creeping closer toward the monetization of government debt.

(Bloomberg) -- A massive shift that’s starting to play out in Asia’s bond markets is finding cautious support from some of the world’s largest investors.

From Jakarta to Wellington, policy makers are challenging taboos and creeping closer toward the monetization of government debt, breaking new ground after the U.S. and Europe took the lead in crisis management a decade ago.

Global bond funds say the bold action from the region’s central banks can’t come soon enough, even as they worry about the longer-term risks, particularly in emerging markets.

“We need to have an exit strategy sometime down the road, but right now we need aggressive policy reaction and most Asian policy makers have been delivering,” said Jean-Charles Sambor, head of emerging-markets fixed-income at BNP Paribas Asset Management in London. “The issuance pipeline is more manageable in Asia than in other regions.”

As the coronavirus has spread from China to its neighbors and around the world this year, bond markets have been thrown into turmoil. Indonesia’s 10-year bond yield skyrocketed to 8.31% while yields on similarly-dated India securities have been buffeted as the government sells bonds at a break-neck pace to fund stimulus. Yields in Australia and New Zealand have whipsawed as traders come to grips with quantitative easing.

“As an investor it’s fascinating to see how quickly things are changing,” said Neeraj Seth, head of Asian credit at BlackRock Inc. in Singapore. “You really have to readjust your overall investment paradigm to match with that.”

The Government’s Hand

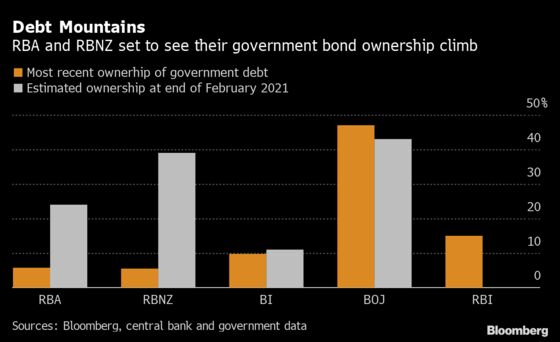

Bank Indonesia was expected to buy conventional bonds directly from the government on Tuesday after snapping up Islamic debt at an auction last week. International investors hold almost one-third of Indonesia’s sovereign debt and rely on India for its high yields. Their stakes are larger still in Australia and New Zealand, where they own about half of all government bonds.

Calculations by Bloomberg suggest that Bank Indonesia could end up holding 11% of the government’s debt, excluding bills, by the end of February next year, while the central banks of Australia and New Zealand are headed for 24% and 39%, respectively. The Reserve Bank of India looks poised to boost its ownership significantly from the present 15%.

Read More: Debt Monetization On the Menu Across Asia

The dangers lurking in these trends are already on display in Japan, where pioneering monetary policy makers have bought almost half the state’s colossal debt without reviving the nation’s economic fortunes. In the U.S. and Europe too, it’s getting increasingly difficult to distinguish between governments and central banks, with the latter buying trillions of dollars of assets.

They “are lining up the largest monetary and fiscal stimulus in history,” said Alberto Gallo, a London-based money manager at Algebris Investments. “This makes the investment environment a lot more difficult compared to the last 10 years.”

Indonesia

The country’s finance ministry on Tuesday received bids for 44.4 trillion rupiah ($2.9 billion) of bonds and bills, according to people familiar with the matter. It wasn’t immediately known how much the central bank may have bid for.

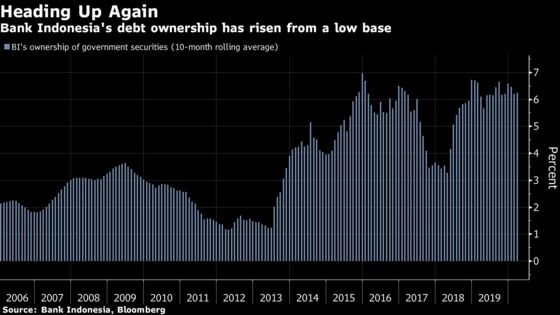

Bank Indonesia’s purchases should boost market stability in the near term, according to Thu Ha Chow, a portfolio manager at Loomis Sayles Investments Asia in Singapore, which trimmed its Indonesia bond holdings earlier this year.

Foreign investors hold about 32% of the nation’s sovereign bonds, making them vulnerable to sharp moves when sentiment sours.

Chow said her concern is that risk premiums become distorted and global investors get crowded out by the central bank.

“Indonesia is effectively beginning to monetize their fiscal debt,” said Edward Ng, a portfolio manager at Nikko Asset Management Asia Ltd. in Singapore. “If left unsterilized and depending on the magnitude, [this] could lead to currency weakening and inflationary pressure at some point.”

BlackRock’s Seth expects any debt monetization in emerging Asian markets to be “balanced” and for yield curves to remain steep. For rates in Indonesia, the short end of the curve looks more attractive, he said.

India

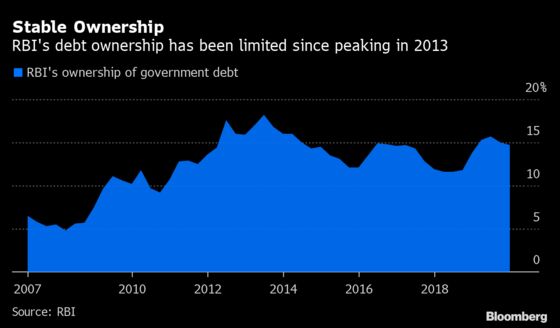

The Reserve Bank of India currently buys bonds in the secondary market through announced operations to manage banking liquidity, and occasionally via anonymous purchases.

While it is banned from buying straight from the government, legislation passed in 2018 has an “escape clause” that allows the RBI to participate directly in primary auctions if the fiscal deficit is expected to be 0.5 percentage points above the targeted shortfall for the year.

With the federal government slated to borrow a record 7.8 trillion rupees ($102.5 billion) in the 12 months through March, there are prospects of a deficit blowout, which is fueling calls for the central bank to step up.

Governor Shaktikanta Das hasn’t taken a view yet on monetization of the government deficit, nor has the central bank participated in the primary government auctions, Cogencis news reported on Monday.

Investors are deeply concerned about how the market will absorb the supply and it is no surprise they aren’t looking to increase their allocations to Indian bonds, said Abhishek Kumar, the London-based head for emerging markets at State Street Global Advisors.

“Governments will spend and the central banks will expand their balance sheets to fund that spending, that’s the global playbook we will witness in the coming months,” said Naveen Singh, head of fixed-income trading at ICICI Securities Primary Dealership in Mumbai. “There is no escape. The RBI will have to come out, sooner or later, with massive bond purchases to fight this unprecedented crisis at our doorstep.”

While India is trying to attract more overseas investors to help with its funding shortfall, this won’t come soon enough to cope with the strains caused by the coronavirus.

Uncertainties are so great that analysts are steering clear of estimating how much sovereign debt the RBI may take on.

New Zealand

Reserve Bank of New Zealand Governor Adrian Orr has said he’s open-minded about buying debt directly from the government.

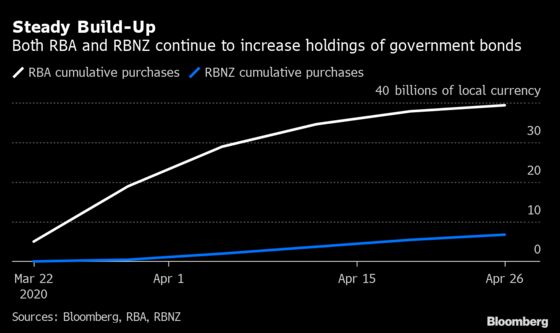

While the country’s finance minister has downplayed the likelihood of this, the RBNZ is already gearing up to purchase NZ$33 billion ($20 billion) over a year in secondary markets.

“There’s a certain comfort from these kinds of statements from credible central banks -- the quality of the institution, or government and legislation matters a lot when you’re entering debt monetization territory,” said Hamish Pepper, fixed-income and currency strategist at Harbour Asset Management Ltd. in Wellington.

Speculation is growing that Orr may raise his buying target at the May policy meeting, which would push the RBNZ’s ownership level even higher than current estimates.

What would come after this is an open question, but it is not so long ago that even quantitative easing seemed unthinkable in New Zealand and Australia.

Australia

The Reserve Bank of Australia has been at pains to emphasize that it is only buying bonds in the secondary market, even as the government rolls out a historic A$130 billion rescue package to save jobs and businesses.

This hasn’t stopped it snapping up A$39.3 billion ($25 billion) of bonds since it embarked on QE last month, or about 7% of outstanding government debt.

None of this dissuades Julio Callegari, lead portfolio manager for local rates and FX in Asia at JPMorgan Asset Management, from buying Australian bonds.

“The fiscal damage of this is quite large across the board, but in places like Australia their starting point is quite good,” Hong Kong-based Callegari said.

Australia’s record A$13 billion bond sale this month gave a clue to the nation’s ongoing appeal among debt investors. Funds tabled A$25.8 billion of bids to the Australian Office of Financial Management for the November 2024 security.

This leaves it in a relatively good position, like its neighbors, but with a delicate balancing act to perform in the months ahead.

“The key challenge for this kind experiment is the risk that people go ‘whoa, it’s too much, it’s too far in terms of debt monetization’. But truth is we’re in a place now where we’re still discussing how deep the recession is going to be” -- Callegari

* Note: Bloomberg’s projected sovereign debt-holdings by each central bank is based on their stated purchase plans, expected issuance and bond redemption over the period to February. For Indonesia, the forecast is based on the assumption that BI would buy a quarter of government bonds sold at auctions, the cap that was mentioned this month by its governor. The analysis excludes bills.

©2020 Bloomberg L.P.