Debate Emerges Over How to Shrink Fed’s $8 Trillion Bond Pile

Federal Reserve officials have begun debating how to approach shrinking a stockpile of more than $8 trillion of bonds.

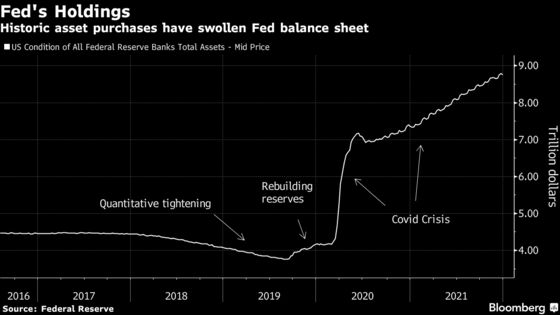

(Bloomberg) -- Federal Reserve officials have begun debating how to approach shrinking a stockpile of more than $8 trillion of bonds as a key element of a policy-normalization campaign in the wake of unprecedented moves to shore up the economy during the pandemic.

While there was a consensus that current conditions are notably different to the last time that the Fed embarked on scaling down its balance sheet, a diversity of views emerged at the Fed’s Dec. 14-15 meeting, minutes of that session showed on Wednesday.

The discussion last month began with a presentation by Fed staff members on the last policy-normalization campaign, which started with raising the key overnight interest-rate target and then two years later was complemented by shrinking the central bank’s bond portfolio.

That episode ended in controversy, with the Fed having been blamed by some market participants for taking too much liquidity out of the financial system, undermining confidence and roiling markets. Last month’s discussion alluded to issues with the 2017-19 experience, without detailing them.

“The previous experience highlighted the benefits of maintaining the flexibility to adjust the details of the approach to normalization in response to economic and financial developments,” the minutes said.

Participants in the meeting “generally emphasized” that boosting the key federal funds rate target would be the “primary means” for the Fed to tighten. Three reasons were cited:

- There’s less uncertainty about the impact of rate hikes than on shrinking bond holdings

- Rate increases are easier to communicate to the public

- It’s easier to tweak the rate-increase plan than the process of running down the bond portfolio

Even so, “some” policy makers made the point that relying more on balance-sheet contraction than on rate hikes could help to limit a flattening in the yield curve. That’s when short-term rates rise by more than longer-term ones. An inversion of the curve, when long-term yields are below short-term ones, is a recession signal.

In theory, by shrinking its bond holdings, the Fed could prop up longer-term yields. Relying less on rate hikes would meantime reduce the amount by which short-term rates rise.

“A few of these participants raised concerns that a relatively flat yield curve could adversely affect interest margins” for lenders, the minutes said, referring to a sub-group of those favoring greater reliance on balance-sheet measures. Such a yield curve “may raise financial stability risks,” according to these officials.

A study by economists at the Federal Reserve Bank of Kansas City released in October made a similar argument -- “we conclude that normalizing the balance sheet before raising the funds rate might forestall yield curve inversion and, in turn, support economic stability.”

Operating Loss?

Michael Feroli, chief U.S. economist at JPMorgan Chase & Co., separately this week raised another reason for the Fed to consider a more aggressive run-down in its balance sheet: the potential for operating losses. As it boosts short-term rates, the Fed has to pay out more interest on the reserves that commercial banks place on deposit with it. At some point, that cumulative bill could get bigger than what the Fed receives on its bond portfolio.

“This shouldn’t lead to technical problems but could prove to be politically embarrassing,” Feroli wrote in a note. “The reputational costs could be notable,” he wrote.

No such mention was made in the minutes of the December meeting.

Meantime, “several” meeting participants last month noted concerns about “vulnerabilities in the Treasury market” that could affect the appropriate pace of reducing bond holdings. Such vulnerabilities have emerged on a number of occasions in recent years, with a sudden dearth of buyers for Treasuries -- particularly those that aren’t the current benchmarks. A seize-up in the market in March 2020 forced the Fed into massive intervention.

The discussion showed that “several” officials underscored that the Fed now has a new tool that can help address strains in markets, however. It adopted the Standing Repo Facility last year, which can provide as much as $500 billion of cash overnight to the banking system.

In all, “many” participants judged that a faster pace of shrinking the bond portfolio will be warranted this time around.

Policy makers highlighted a number of differences from the last time the Fed mounted policy normalization:

- The economic outlook is stronger, with inflation faster and the labor market tighter

- The Fed’s balance sheet is bigger, both in dollar-amount terms and with regard its ratio to GDP

- The weighted average maturity of the Fed’s holdings is shorter. This means by simply allowing securities to mature without replacing them, it could shrink much faster without caps on the process

“It appears we should expect both an earlier start and more aggressive path for Fed balance sheet runoff,” JPMorgan strategists concluded Wednesday.

©2022 Bloomberg L.P.