Here Comes DBS’s Muddle-Through Year

(Bloomberg Opinion) -- Singapore’s largest bank had only the briefest of honeymoons with an improving global economy.

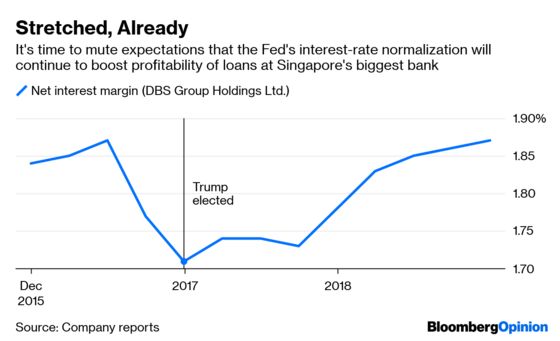

Rising global interest rates, amplified by U.S. president Donald Trump’s late-cycle fiscal expansion, boosted DBS Group Holdings Ltd.’s loan profitability. But only up to a point.

In the past three months, the two to four rate increases CEO Piyush Gupta expected from the Federal Reserve in 2019 have begun to look all but impossible. Net interest margin did manage to expand by 1 basis point in the December quarter to 1.87 percent. Still, it’s hard to see how the 16-basis-point jump over the past two years can extend any further.

One reason is Trump’s tariff war with China. Trade financing, which accounts for a tenth of the lender’s assets, shrank 5 percent by value over the previous quarter. A sudden deterioration in the global economic outlook and heightened volatility in asset prices are also taking a toll. With income from wealth-management fees falling to a two-year low and trading income dropping by 35 percent during the quarter, DBS’s net income missed the consensus estimate.

Deposit competition in Hong Kong is another reason to be pessimistic about margins. Hong Kong dollar deposits, which provide more than 9 percent of DBS’s total customer funding, fell 3 percent. Within that, current and savings accounts – sources of practically free money – slid 13 percent in the December quarter. Virtual-only banks could further spice up competition for cheap funding in the city.

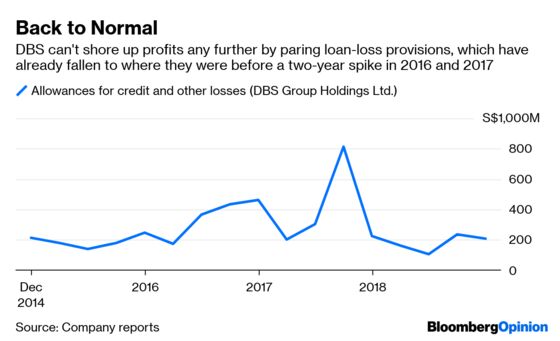

Last year, DBS shored up profits by more than halving the elevated loan-loss provisions taken in 2016 and 2017, when a meltdown in global energy prices dinged Singapore's offshore-and-marine industry. There's little scope to cut credit losses any further. Neither will last year’s 7.9 percent gain in Singapore’s residential-property market be repeated anytime soon; home prices fell last quarter after the government clamped down on speculation in July.

A cost-to-income ratio of 46 percent-plus saw DBS’s return on assets slip below 1 percent in the December quarter – the first time that happened in 2018. To the extent higher costs are related to the bank’s technology push, the 1-percentage-point drop in return on equity to 11.3 percent should be temporary.

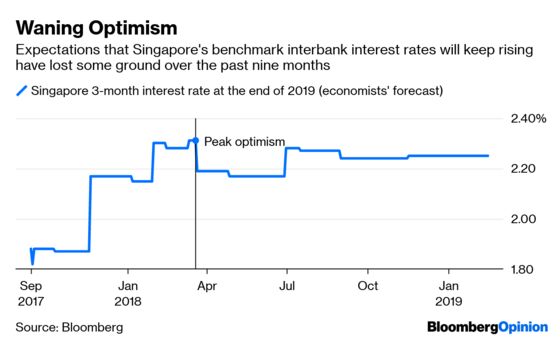

Even if loan profitability doesn’t improve much this year, it’s unlikely to fall off a cliff: Surveys predict Singapore’s benchmark three-month interbank rate will still rise to 2.25 percent from 1.95 percent by the end of 2019. However, with the Fed putting interest rates on hold and hinting a pause to its balance balance sheet contraction, the best for DBS may already be in the rearview mirror.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.