Currency Traders Are Missing the Details in This Rout

(Bloomberg Opinion) -- Stereotypes are difficult to shake, especially in times of distress. As hard as central bankers and politicians try to change them, the old rules of investing still apply.

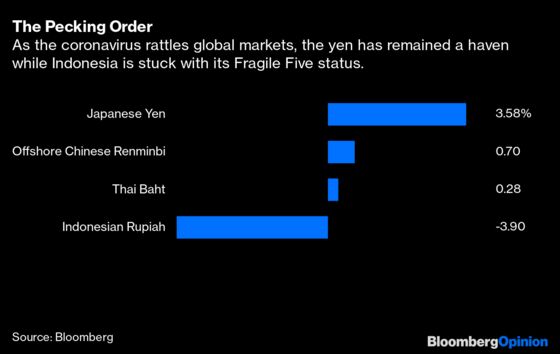

Just take a look at the currency market. As the outbreak spread to the U.S. — causing the worst weekly stock selloff in a decade — traders still abided by the old pecking order, bidding up the Japanese yen and selling down the Indonesian rupiah. Meanwhile, the yuan stayed eerily calm, even though the virus came from China and two-thirds of its smaller businesses are struggling to get their employees back to work, according to Beijing’s own briefing.

Japan's case is curious. Judging by Prime Minister Shinzo Abe’s crisis response, the country seems to be anything but a haven. The Diamond Princess cruise ship, which was quarantined for days off Yokohama, represented the largest concentration of coronavirus cases outside China. Despite ranking high on the Centers for Disease Control and Prevention's watch list, Tokyo isn’t conducting enough diagnostic tests. This foot-dragging may be partly driven by Abe’s reluctance to derail the Tokyo Olympics, the New York Times reported.

But currency traders aren’t looking at the details. Buying the yen is a well-worn theme, not an outcome of careful political-economy analysis. If you have a bearish stance toward the U.S. market during Asian trading hours, buy the yen. The correlation coefficient between the S&P 500 and the dollar-yen pair is a whopping 64% on a weekly basis, the highest among G-10 countries. The yen paused its advance Monday, dropping 0.4% in morning trading after the Bank of Japan injected liquidity into the market. The currency’s sharp rise last week is leaving hedge funds wrong-footed, exposing them to the risk of short covering.

Then consider Indonesia, which hasn’t recorded any cases, despite the fact that the nation of 264 million features prominently on China’s Belt and Road Initiative. While questions remain about testing accuracy, the country still has plenty for investors to like. President Joko Widodo has made Indonesia a better investment destination in recent years, slashing red tape and improving the country’s onerous land acquisition and labor laws. The new capital, estimated to cost $34 billion, may have first-tier investors ranging from SoftBank Group Corp. to Abu Dhabi’s sovereign funds.

Yet Indonesia’s Achilles heel isn’t the paucity of direct investment so much as foreigners’ sovereign debt holdings, at almost 40% of the total. When markets get jittery, that money flees.

In China, meanwhile, the yuan remains resilient, falling only 1.7% since Jan. 20, when the coronavirus first started gaining global attention.

One rationale is that a nationwide curfew is keeping restless Chinese tourists from going abroad. As a result, there’s little need to buy as much as $14 billion a month worth of foreign currency — or sell yuan of the equivalent amount — estimates HSBC Holdings Plc. This is certainly bullish for the yuan, as China edges toward a current account deficit.

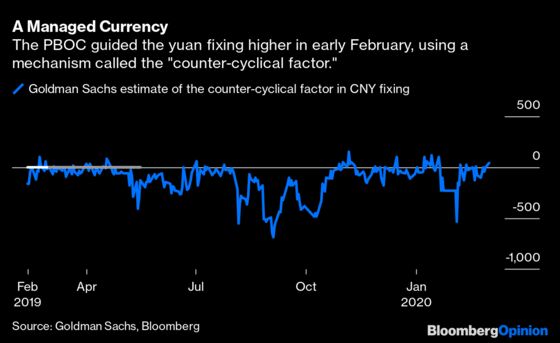

The truth is, the yuan remains a heavily managed currency. In early February, the People’s Bank of China guided its daily fixing higher, using a mechanism called the “counter-cyclical factor.” This tool has become a catch-all that allows officials to ignore true market dynamics and adjust the currency's path to its liking. As for yuan bears in Hong Kong — who aren’t beholden to the 2% daily trading limit of their onshore counterparts — the central bank has already found clever ways of killing them.

Thanks to a bull stock market — also engineered by Beijing — offshore demand for the yuan has been quite strong. With President Xi Jinping repeatedly vowing to keep China’s growth target, investors are now expecting helicopter money. That doesn't seem so far-fetched given the economy's contraction in the first quarter, which could be as much as 6% on an annualized basis.

It’s at this moment of distress that we realize Asian countries aren’t transforming themselves fast enough. Japan's yen is too strong for an economy in perpetual deflation; Indonesia can't shake the Fragile Five label; and market reforms are nowhere seen in China. Optimists may say the region has learned the lesson from past financial crises. The coronavirus only proves otherwise.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2020 Bloomberg L.P.