China’s Banks Are Going to Suffer. But Not Equally

(Bloomberg Opinion) -- China’s bank stocks have sold off indiscriminately on concern the coronavirus epidemic will drive up bad loans and hurt earnings. The reality is more nuanced. The biggest state-owned banks are likely to be worst affected, as the government sticks them with the the bulk of the bill for shutting down two-thirds of the economy. The smallest, meanwhile, already have well-documented funding challenges. Midsize lenders look best placed to ride out the storm.

You wouldn’t think so to look at the stock market. Medium-size lenders China Everbright Bank Co., Shanghai Pudong Development Bank Co. and China CITIC Bank Corp. have all dropped more than 10% in Shanghai trading since mid-January, when the spread of the virus started to weigh more heavily on markets. By contrast, the so-called big four state-owned banks have lost between 4.6% and 6.6%, with the steepest fall suffered by Industrial & Commercial Bank of China Ltd., the biggest.

There are signs already that banks will be pressed again into what’s been called “national service” — sacrificing their commercial interests to support broader government policy objectives. On Jan. 26, the banking regulator issued guidance calling on lenders to give special consideration to borrowers amid the outbreak, such as offering a moratorium to individuals having trouble meeting mortgage, credit-card or loan payments. They were also told to extend extra support to companies that are essential in combating the virus, such as medical providers, as well as businesses operating in virus-hit areas.

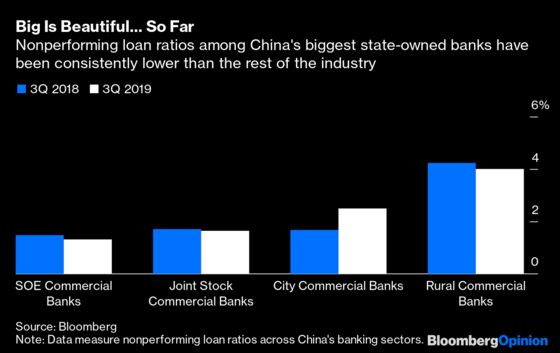

The cost of such support will inevitably fall most heavily on the biggest financial institutions. They are the best capitalized and have lower bad-loan ratios than the industry as a whole, even as China’s economy has slowed. For the third quarter, the six largest banks by assets reported a nonperforming loan ratio of 1.32%. That number looks sure to rise. A prolonged health emergency could lead to 5.6 trillion yuan ($800 billion) in fresh bad loans, causing the system-wide ratio to more than triple to about 6.3%, S&P Global Inc. estimates.

That’s likely to mean more difficulties for small lenders, adding to funding stresses that have persisted since the bailout last May of Baoshang Bank Co. The government may be tempted to turn to its largest institutions to stave off any further collapses, as it did in July when ICBC became the largest shareholder of Bank of Jinzhou Co.

Smaller lenders have also been hit hard in the market rout, with the mainland-traded shares of Bank of Nanjing Co., Bank of Hangzhou Co. and Bank of Xi’an Co. all dropping by more than 10% since mid-January. Shares of Bank of Jinzhou remain suspended in Hong Kong after tumbling 65% late last year.

Besides the threat of having to rescue their weaker brethren, the biggest banks have also increased their exposure to small private companies that are likely to be among the most vulnerable amid the virus-imposed shutdown. That’s a legacy of Beijing’s years-long deleveraging campaign, which squeezed the private sector’s access to loans. In response, the government exhorted banks to embrace “inclusive finance.” The big four — comprising ICBC, Agricultural Bank of China Ltd., Bank of China Ltd. and China Construction Bank Corp. — extended 6.1% of their gross advances to small and micro businesses in the third quarter, up from 5.2% in the first. That’s still below the 7.5% share for the banking sector as a whole.

Midsize lenders are less likely to be used as policy tools by Beijing. At the same time, the likes of China Merchants Bank Co., and Everbright Bank have a more secure deposit base and so aren’t as dependent on interbank funding as their smaller rivals. They tend to have strong fee income, insulating them to some extent from troubles in the private sector (to which they are big lenders) and making them less vulnerable to the rate cuts analysts expect, which typically undermine bank earnings. Merchants Bank, for instance, is strong in retail and private banking, while Everbright and CITIC have large credit-card businesses.

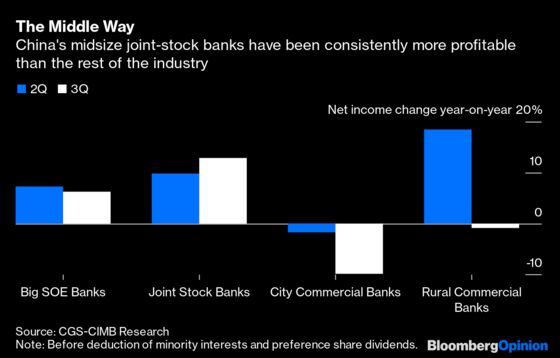

Their earnings are also growing faster. China’s 12 joint-stock commercial banks (which mostly fall into the medium-size category) posted a 12.8% increase in third-quarter profit from a year earlier. That compared with a 6.2% gain for the big state-owned lenders and a 9.9% decline for city commercial banks, according to CGS-CIMB Research. Their NPL ratio stood at 1.6%.

While there may be no escaping the damage that the coronavirus will inflict on China’s banking industry, the middle way offers the best hope of a refuge for investors.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2020 Bloomberg L.P.