(Bloomberg Opinion) -- It’s quite a statement to launch a US$2.82 billion foreign-currency perpetual bond (the riskiest type of debt) in the biggest Chinese deal of this type since 2017 — especially when the debt capital markets have hit their quietest period this year on coronavirus uncertainty.

Bank of China Ltd. achieved this feat on Wednesday, with one of the lowest coupons on record (3.6%) for any bank for this type of issue. These so-called additional tier 1 (AT1) regulatory capital bonds, known as CoCos, have tended to yield much higher in the past because because of their riskiness (the investor would bear the losses on the debt if the bank ever fails).

Though it was twice covered with an order book of nearly $6 billion, that’s actually relatively low for this type of bond sale — no doubt a reflection of its unusually vast size for an AT1. It has struggled too in the after-market as it will take some time to be digested properly.

Local buyers will have played a big part too in making sure this deal was a success. Nonetheless, it’s reassuring that bond buyers are still eager to take exposure to China’s oldest bank for its first dollar perpetual since 2014. Amid all the fears about the coronavirus and the effect on the country’s economy, this shows its biggest banks can raise money fairly easily. The bank issued a yuan-denominated perpetual bond last year but it has no outstanding dollar AT1 debt so a deal of this magnitude was due — it is the timing that’s impressive.

This benchmark deal will probably be followed by other Chinese banks because there’s a need for them to boost regulatory capital buffers, as several credit rating agencies have highlighted. Furthermore, there are more than $40 billion worth of outstanding AT1 deals with call dates this year that are expected to be redeemed. Bank of Communications Hong Kong Ltd. also issued a $500 million CoCo this week.

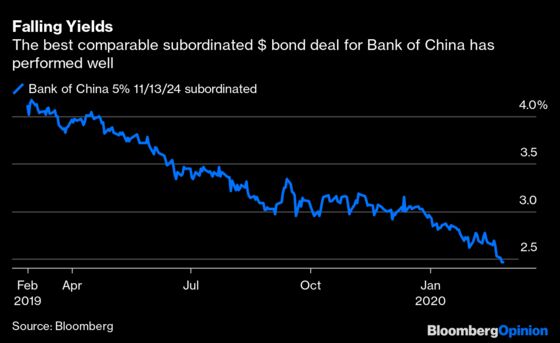

The People's Bank of China, the country’s central bank, relaxed its rules in January last year to allow perpetual bonds as eligible collateral, thereby increasing their attractiveness for use in liquidity funding. This shows how the Chinese authorities are trying to be as flexible as possible. Falling yields offer a chance for Chinese banks to get ahead of their funding needs so long as investor demand holds up. The experience of Bank of China should offer reassurance in difficult times.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.