(Bloomberg Opinion) -- Relying too much on shoppers to tide over growth can be a risky business.

China and the U.S. have been leaning heavily on consumers to sustain their economic expansions. With the threat of hundreds of billions in tariffs looming over goods from bicycles to roof tiles, it seems only a matter of time before these noble buyers start to falter.

Over the past several years, the pace of China’s retail sales growth has outpaced other economic drivers, such as industrial production. In September, retail sales rose 7.8% from a year earlier, a touch higher than August. Consumption contributed 60.5% to gross-domestic product growth in the first nine months of the year, up from 55.3% in the first half. Those figures come against lackluster third-quarter growth of 6%, as a downdraft of Beijing’s crackdown on local debt crimps expansion and the trade war hits exports. That’s less than forecast and the lowest pace of growth in decades.

In the U.S., where consumer spending accounts for roughly 70% of GDP, we’re starting to see evidence that this economic muscle has gone wobbly. Earlier this week, retail sales unexpectedly posted the first decline in seven months, at a time when manufacturing and business investment are already faltering. Consumer spending had been propping up the economy in recent months, buoyed by rising incomes and rock-bottom unemployment. The trouble is, such data have has been a poor gauge of past recessions, as Komal Sri-Kumar wrote in a Bloomberg Opinion column in September.

While it’s nice to have a relatively robust domestic driver when global demand for your products starts to ebb (or they suddenly become more expensive thanks to tariffs), it’s cavalier to think that one pillar can power an entire economy indefinitely.

The recent slackening of the U.S. and Chinese economies, on which so much global prosperity has rested, shows just how intertwined commerce between the duo remains. There’s a lesson there: If you’re going to engage in a trade war, don’t expect it can stay limited to to the containers sitting around the wharves in Los Angeles or dockside in Tianjin. Ultimately everything is linked, making “synchronized slowdown,” a term deployed by the International Monetary Fund this week, depressingly apt.

It's possible that domestic consumption can tide activity over while monetary policy is loosened further and some fiscal support is provided, or at least considered. China can probably meet its annual growth forecast of between 6% and 6.5%, and still has plenty of levers to juice activity should it wish. Yet Beijing is wary of building up another stimulus-induced debt overhang.

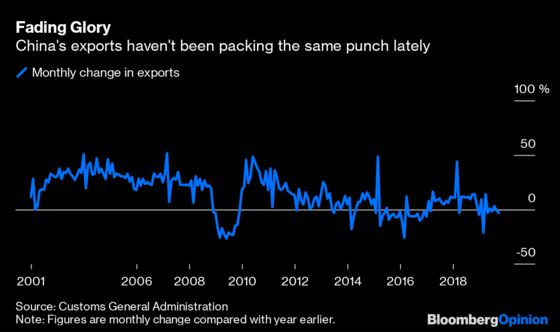

It’s no small irony that China’s growing dependence on the home front would be a recipe for slower growth just when the world needs its largess to buttress global expansion. For years officials from developed economies lectured China about the need to re-balance the economy away from manufacturing. The country’s exports fell more than anticipated last month, and imports slid as well. How many will still think this trend is a great idea in, say, a year’s time?

Many experts also urged China to kick its over-reliance on debt-fueled growth; yet it was that very model that lifted the global economy from its rut in past recessions. The world might welcome a dramatic opening of China's spigots. In some ways, that’s the last thing China needs.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.