G-20 Finance Chiefs Go on Alert With Global Growth at Risk

Climate Change, Global Tax Emerge as Snags for G-20 Communique

(Bloomberg) -- Finance chiefs and central bankers from the world’s largest economies say they see downside risks to global growth persisting as the coronavirus raises uncertainty and disrupts supply chains.

While delegates at the Group of 20 meeting in Riyadh, Saudi Arabia, spent much of their time talking about a response to the outbreak that originated in China, their final communique only mentioned the epidemic once, saying they’d enhance risk monitoring. And although it said the participants agreed on a “menu of policy options” to counter the emergency, the statement included few details on a coordinated response.

The coronavirus has so far killed more than 2,300 people and infected about 80,000. Countries such as Japan, and institutions including the OECD, have been pushing for nations with surpluses to spend more to help avert a deeper economic slump.

The G-20 countries “agreed to be ready to intervene with the necessary policies related to these risks,” Saudi Finance Minister Mohammad Al Jadaan said Sunday in remarks concluding the meetings at the Ritz Carlton Hotel in the Saudi capital. “Global economic growth is continuing but remains slow and downside risk persists, including those arising from geopolitical, remaining trade tensions, as well as policy uncertainty.”

China’s representatives were absent from the G-20 gathering as authorities there focus on countering the fallout. The world’s second-largest economy is likely to pick up quickly after the coronavirus is contained and stage a “V-shaped” recovery, according to Chen Yulu, a deputy governor at the People’s Bank of China.

International Monetary Fund Managing Director Kristalina Georgieva said Saturday the outbreak had led the lender to cut its forecast for Chinese growth to 5.6% from 6% and to trim 0.1 percentage points from its global growth forecast, but that it’s also looking at more “dire” scenarios.

“We do not know what will be the next steps, indeed if the epidemic will turn to pandemic or not,” French Finance Minister Bruno Le Maire told Bloomberg TV in Riyadh. “But we have to be prepared and that is exactly what we decided today among the G-20 members.”

Budget Appeals

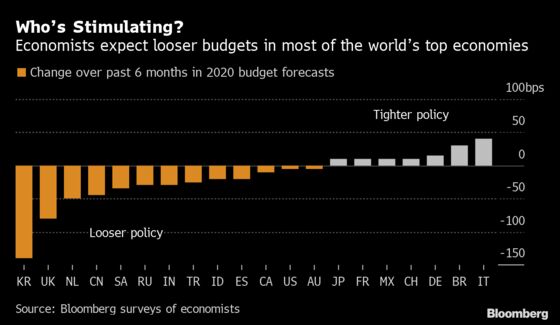

Germany was the primary target of the calls for more spending. So far, the export-driven country has showed little interest in significantly boosting expenditures, arguing fiscal stimulus can’t bolster foreign demand.

“Fiscal policy should be flexible and growth-friendly while ensuring debt as a share of GDP is on a sustainable path,” the communique said. “Monetary policy should continue to support economic activity and ensure price stability, consistent with central banks’ mandates.”

The delegates managed to extract a key concession from the U.S. by including a mention of climate change in the final communique for the first time since President Donald Trump took office in 2017. Jadaan called it a “very important issue” on the Saudi agenda.

The concession came after several days of heated debate, including France finance chief Bruno Le Maire cornering Treasury Secretary Steven Mnuchin late Saturday as the G-20 economic leaders dined, according to two people familiar with the matter. Mnuchin said he didn’t bow to European pressure on the issue, and the mention of “climate” in the communique was simply a statement of fact about what the financial stability board was doing.

Tax Debate

The final communique didn’t include any breakthroughs on efforts to introduce a global minimum tax or a tax system for multinational tech giants like Alphabet Inc.’s Google and Facebook Inc., according to the people.

Europeans have balked at a U.S. proposal that new global rules should be a “safe harbor” regime. If there’s no agreement, several European nations, who have called for an agreement by year-end, will go ahead with taxes on revenues of multinational digital firms. That could spark a transatlantic trade war as the U.S. says such measures are discriminatory and has already threatened France with tariffs.

In a press briefing after the meetings concluded, Mnuchin said there was a disproportionate focus on some elements of the digital tax discussion, and called on his counterparties to “step back” and focus on the global minimum tax, for which he said there was broad agreement. He declined to define what he meant by “safe harbor,” but said the U.S. has been consistent in stating that the digital services tax would be discriminatory to U.S. companies.

France and the U.S. have held tense discussions on the subject since France introduced a 3% levy last year on the digital revenue of companies that make their sales primarily online. The move was supposed to give impetus to international talks to redefine tax rules, and the government has pledged to abolish its national tax if there is agreement on such rules.

France and other countries have insisted that the digital tax and the global minimum tax, which is designed to prevent multi-national companies from shifting their profits to low-tax locales to avoid taxation, be implemented as part of the same package.

“We’re striving between now and July 2020 -- whether at the Berlin OECD conference or the meetings in Jeddah of the G-20 ministers -- to reach an agreement related to the tax,” Al Jadaan said.

--With assistance from Saleha Mohsin and Vivian Nereim.

To contact the reporters on this story: Toru Fujioka in Tokyo at tfujioka1@bloomberg.net;Jana Randow in Frankfurt at jrandow@bloomberg.net;William Horobin in Paris at whorobin@bloomberg.net

To contact the editors responsible for this story: Benjamin Harvey at bharvey11@bloomberg.net, Paul Abelsky

©2020 Bloomberg L.P.