China Seeks to Defuse Its $4.5 Trillion Local Hidden Debt Bomb

China Seeks to Defuse Its $4.5 Trillion Local Hidden Debt Bomb

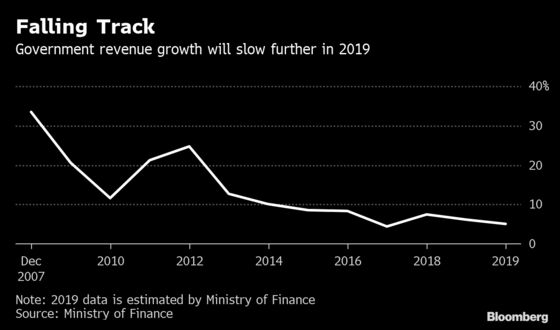

(Bloomberg) -- China’s multi-year campaign to contain financial risk is re-focusing on the so-called “hidden debt” owed by local governments, as officials seek to reduce repayment pressures amid falling tax revenues.

Provinces and cities from Jiangsu in the east to Qinghai in the west are looking for means to pay-off or restructure their implicit borrowings, a term which includes off-book funding via financing vehicles. Some authorities are seeking cheap refinancing from the nation’s largest policy lender, the China Development Bank, and others are selling off state-owned assets such as office buildings and housing.

| Hidden Debt Estimated By | Trillion Yuan |

|---|---|

| Southwest Securities Co | 30-35 |

| Lianxun Securities Co | about 37 |

| S&P Global Inc (as of Oct. 2018) | about 40 |

Efforts to address the chronic issue are gaining urgency as the government pledges to cut taxes by two trillion yuan ($297.5 billion) this year, further draining local coffers and adding to the possibility of missed repayments. The fact that there is no official estimate of the size of the implicit debt, which usually carries higher rates than on-book ones, makes the issue even trickier.

No Official Estimates

The motive is “just that the problem can’t be delayed anymore,” as in many places fiscal revenues and gross domestic product aren’t enough to cover the interest and principals, said Lu Ting, chief China economist at Nomura Holdings Inc.

Such probes are under way, and so far they’ve shown that hidden debt in some places exceeds the on-book borrowing, a lawmaker of the National People’s Congress Zhu Mingchun said over the weekend, without naming places directly.

Payments due for local-government financing vehicle debt, just part of the off-book borrowing, could reach 2.3 trillion yuan this year, according to estimates by Industrial Securities Co. Local authorities will have to carry that burden at a time of slowing revenue growth due to tax cuts and shrinking receipts from land sales, unless they can restructure.

In one case in December, the CDB led a group of commercial lenders in a swap of 260.7 billion yuan of implicit debt borrowed by Shanxi province to build highways. The debt was restructured with a tenor of up to 25 years, allowing the local authorities to save 3 billion yuan in interest payments every year, according to Shanxi Transportation Holdings Group.

Asset sales are also being used. For example, a district in the northeastern city of Shenyang is planning to sell more than 38,000 square meters of offices and government-built housing to repay maturing debt.

Read More: China’s Policy Bank Has New Job Resolving Hidden Government Debt

Policy makers are using “the healthier part of the balance sheet of the public sector to address some of the hidden issues,” but they have to make sure the risky loans won’t get out of control again in the future, because by that time the balance sheet would be less capable of absorbing them, said Grace Ng, a China economist at JPMorgan Chase & Co. in Hong Kong.

The efforts to address hidden debt have made notes sold by local government financing vehicles more attractive to investors on expectations of possible government bailouts.

A financing platform in the eastern province of Jiangsu, where the CDB is involved in some cases of debt restructuring, sold a 270-day bond last week with a coupon of 4.8 percent, 150 basis points lower than a similar note the company issued in January. On Monday, a financing and investment company owned by a city in Shanxi province was upgraded to AA+ from AA by China Chengxin International Credit Rating Co., which cited the better outlook for capital quality.

“The bigger worry is the moral hazard issue,” said Zhu Ning, a professor of finance at Tsinghua University and the author of “China’s Guaranteed Bubble.” “Implicit government guarantees still lie at the core of so many problems.”

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Ling Zeng in Shanghai at lzeng30@bloomberg.net;Tongjian Dong in Shanghai at tdong28@bloomberg.net;Heng Xie in Beijing at hxie34@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger, Karthikeyan Sundaram

©2019 Bloomberg L.P.

With assistance from Bloomberg