Traders Look to Profit in China Bond Market That Won’t Move

China Traders Look to Profit in Bond Market That Doesn’t Move

(Bloomberg) -- Making money in a market that moves so little has become a key challenge for China’s sovereign-bond traders.

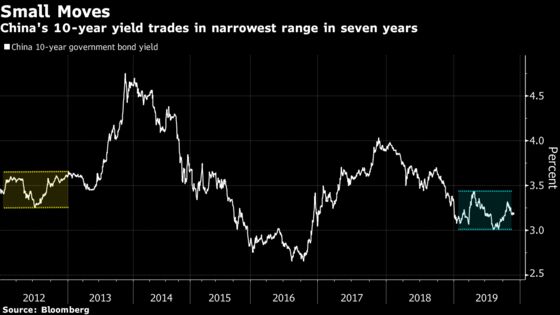

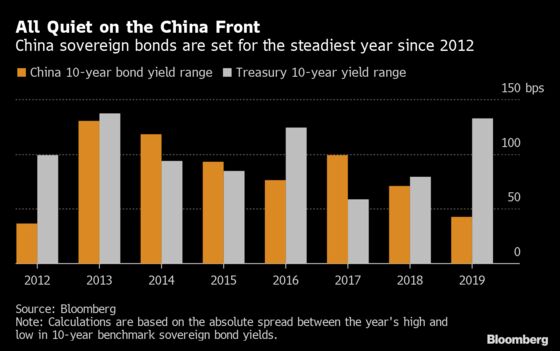

With 10-year notes trading in the narrowest range in seven years, investors are casting their nets far and wide to enhance returns. It’s policy bank bonds for JPMorgan Asset Management and PineBridge Investments Asia Ltd., dollar-denominated debt for Nissay Asset Management Corp. and convertible bonds for Morgan Stanley Huaxin Fund Management Co.

China’s 10-year yield has fallen just 11 basis points this year, missing out on a global rally that in August took the world’s stockpile of negative-yielding bonds to a record $17 trillion. The People’s Bank of China helped trigger a sell-off in October when it effectively withdrew liquidity from the financial system, but bonds have since stabilized following a series of unexpected policy-rate cuts and cash injections.

But that wasn’t enough to spur a rally: the central bank signaled this week it will continue to refrain from large-scale easing. A supply surge in local government notes is also concerning traders.

Here’s how some investors are navigating the market:

Policy bank bonds

China’s quasi-sovereign policy bank notes -- particularly in the three-year tenor -- are worth considering, says Jason Pang, a fixed-income portfolio manager at JPMorgan Asset Management. The bonds are in a “sweet spot” as they benefit from any liquidity injections and still provide a decent yield above 3% and greater roll-down returns, he said, referring to the strategy of selling a note as it approaches maturity. Arthur Lau, head of Asia excluding Japan fixed income at PineBridge Investments, also prefers policy bank bonds, as the notes have higher yields than sovereigns. He favors them in five- to seven-year tenors.

Dollar-denominated debt

Toshinobu Chiba, chief portfolio manager of fixed-income investment at Nissay Asset Management, took an overweight position in dollar-denominated China credit in October and sold Chinese government bonds after consumer prices rose by the fastest pace since 2013 in September. He’s looking to buy China dollar bonds, with a view that the central bank has little room to ease monetary policy if inflation remains high. He says dollar corporate debt will remain attractive in the coming six months, with rising demand for it signaled by a tightening credit spread.

Investment grade credit

While Pictet Asset Management Ltd.’s head of China debt Cary Yeung is still positive on Chinese sovereign bonds, he’s also a fan of onshore investment-grade credit for its “low volatility, decent carry and stable” fundamentals. He likes short-dated high-yield bonds issued by property companies, as the sector’s sales have been doing well and it might see more favorable policies in the future.

Derivatives and others

Li Yi, a fund manager at Morgan Stanley Huaxin, whose onshore China bond fund has outperformed 95% of peers over the past three years, says to “pay attention to convertible bonds, treasury bond futures and other derivatives to enhance returns.”

Better year

For Manu George, a fixed-income director at Schroder Investment, the current yield of Chinese sovereign debt is already attractive and he has taken a long position. China bonds are likely to see a better year in 2020, he says.

The yield on China’s 10-year sovereign bond was down 1 basis point at 3.2% as of 4:55 p.m. local time.

--With assistance from Tian Chen and Jing Zhao.

To contact Bloomberg News staff for this story: Livia Yap in Shanghai at lyap14@bloomberg.net;Claire Che in Beijing at yche16@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, David Watkins, Philip Glamann

©2019 Bloomberg L.P.

With assistance from Bloomberg